.jpg)

Weekly Newsletter

Freedom Calls: 9/2/26, "Anti-Capexism challenged and Mr Warsh explained"

by

the team at Freedom Asset Management

February 9, 2026

5 Minutes

Freedom Calls: 9/2/26, "Anti-Capexism challenged and Mr Warsh explained"

From the team at Freedom Asset Management

++ This is coming out early because I am on the overnight flight to Abu Dhabi via Doha and don't fancy my chances with the airport WIFI in Doha early tomorrow morning ++

First up, a picture of the stunningly beautiful Swiss Alps from last week, where I think we came across our favourite "Sirius dog sled team" sneakily undergoing elite combat training in Verbier, whilst Mr Trump takes his eye of Greenland for a while(!). The dogs are in good company - the British Army often sends its people to train on the slopes of Verbier.

A couple of surprise economic take-aways from the slopes: a lack of inflation - a hot chocolate on the slopes is still "only" CHF5 - some 8 years after I was last in these parts, and house prices in Verbier are down 5% on the year - a place where previously house prices only ever went up. It seems even Switzerland is not immune to real estate pressures in Europe.

Our articles this week

Away from the slopes, it was obviously quite a busy week. We have two excellent articles this week picking up on the two key market themes of last week:

10,000 Days Cody Willard and Bryce Smith (USVIP) share their thoughts on last week's tech sell-off, which disproportionately affected software firms in their piece entitled: "SaaSpocalypse, Anti-Capexism, And A Crypto winter"

Canaccord's Justin Oliver (OGG) talks about Kevin Warsh, the new proposed Fed Chair, who partly spooked the markets with his desire to reduce the size of the Fed balance sheet, whilst at the same time supporting lower short-term interest rates. Mr Warsh is also up for looking at the economy very much in the style of Alan Greenspan and will be willing to run it "hot", which should be good for the US and global equity markets.

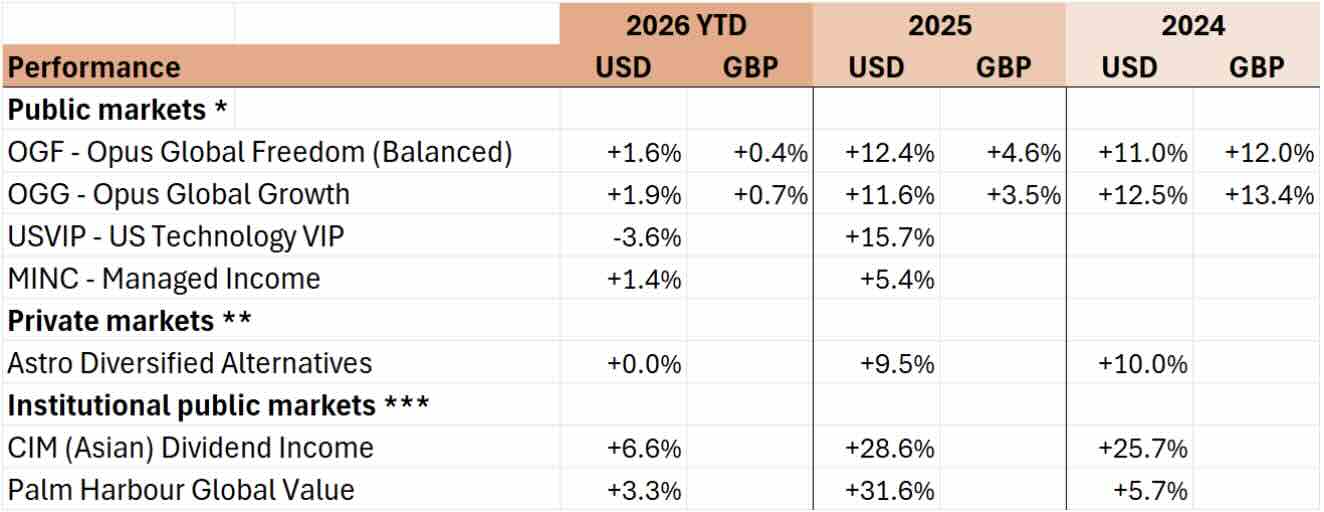

Performance - a rough week in tech presents a helpful buying opportunity

One of the great things about temporary market weakness is that it can present more helpful buying opportunities - none more so than in technology right now. We look forward to welcoming investors old and new into our US Technology VIP strategy whilst market prices are giving us a little discount. Please reach out to your usual Freedom counterpart or simply reply to this email and we will be in touch.

The remaining funds OGF, OGG and MINC continued to perform solidly despite the big market gyrations of last week.

(Please see performance disclaimers at the foot of this email.)

No news in Iran

We have still not seen Trump show his hand on Iran - so that geopolitical event is still very much out there, and the protesters in London were very much out in the streets of Whitehall today (like last weekend, and the weekend before) chanting for regime change in Iran. It seems difficult to believe that the solution will not involve some military intervention from the US and Israel, but this is more complicated than Venezuela, so those strikes will need to be very precise and not impact the oil price (a sentiment echoed by a source at a large US investment bank over the weekend). As we said last week, a world where Iran does not have a nuclear capability is a safer world and that is good for markets…. even if there are some wobbles on the day.

I will keep this week's note short, except to say I am looking forward to be in Abu Dhabi and Dubai this week - and then Guernsey for the week after. Wherever you are this week, please let me wish you a peaceful and prosperous week ahead,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

————————————————

"SaaSpocalypse, Anti-Capexism, And A Crypto winter", 9/2/26

By 10,000 Days' Cody Willard and Bryce Smith - Advisers to US Technology VIP Fund

Today we find ourselves in a tech bear market that in many ways rivals the post-COVID 2022 crash in severity. While the indices aren’t too far off all time highs (ATH), beneath the surface you can find absolute carnage. Three phenomena are converging to cause the sudden collapse in many tech stocks.

First, we have the alleged death of software, a.k.a. the SaaSpocalypse. New tools like Claude Code, OpenAI’s Codex, and the open-source “Clawdbot” present existential threats to the software industry. The iShares software index (IGV) is down about 25% YTD (and we’re just six weeks into the year) and about 33% from its all-time high set back in September 2025.

Stocks like Applovin, Duolingo, Salesforce, ServiceNow, Zscaler, Crowdstrike, Snowflake, are down 50% or more from their highs. Even former darlings like Microsoft and Palantir are down 25%+. Software valuations have always been notoriously high, so it’s not unreasonable to see a big drawdown when uncertainty around the sector is this high.

Second, the market has developed a prejudice against AI capex, what we call “capexism”.

The hyperscalers’ 2026 capex guidance came in way above Wall Street expectations (32% higher) and is up significantly (about 63%) from last year. The hyperscalers are saying they will spend $625 billion between the four of them, and when you include other major players like Oracle, Tesla, and CoreWeave, we’re looking at $725 billion in capex in 2026.

That’s more spending in one year than the American Recovery Act and the Inflation Reduction Act spent on physical infrastructure, combined (not to mention that government spending took place over several years).

Source: 10,000 Days

Despite beating on the top and bottom lines and issuing guidance that exceeded expectations, the stocks of all of the companies above are down significantly because of capexism. People are concerned that these companies will not generate a high enough return on these massive investments, and therefore the capexists think they are set to burn unprecedented levels of capital.

Third, we are now in the freezing cold depths of another crypto winter. Bitcoin is down about 50% from its high in October, and crashed 16% in the last five days. The infamous Microstrategy (MSTR), a stock we’ve warned people about for the last two years, is down 76% from its ATH set last summer and traded at a discount to its NAV for the first time since 2022. Crypto-related stocks like Coinbase, Robinhood, and Circle are down 65%, 53%, and 81% from their ATHs, respectively.

This storm of bearishness leaves tech stocks in quite a dismal state of affairs. A lot of stocks still aren’t “cheap” by traditional metrics and we suppose it looks like there could be more room to fall. People have been calling for a crash in tech for some time now. And that’s what they now have.

With all that said — here’s why we’re buying: the market’s perception of reality is not aligned with reality itself. Tech is facing a test and it’s one that we are confident it will pass.

First, the fears around software are overblown. AI is highly disruptive, but software companies are not sitting still, and in fact they are the ones adopting AI faster than anyone. Every software CEO has known that AI represented an existential threat to their business, and they’ve spent the last two years integrating AI into their legacy products as fast as possible. Google said that their largest SaaS customers increased their AI spending commitments by 16x last quarter, because the products these software companies built on Google’s AI saw revenue grow 300% y/y.

The SaaS industry will transition from seat-based pricing to consumption-based pricing, and there will probably be some pain in the short term for some companies (we might even see revenue decline for some software companies over the next year), but we think there are a lot of SaaS companies that are positioned to grow rapidly as they increase the value they deliver to their customers with AI. Business models will change, but software as a category of technology is not dead.

Second, capexism rests on the faulty premise that companies are not generating ROI with this spending. This is such a tired argument at this point that I’m a little shocked it has surfaced again. We spent the whole of 2025 debating AI capex ROI, all whilst the hyperscalers demonstrated growing revenue and profits quarter after quarter. You’d think the fact that the hyperscalers uniformly raised capex to the tune of 30% more than Wall Street estimates would put to bed any arguments about whether these companies are seeing a return on their massive spending.

Do the anti-capexers really think the leaders of the largest tech companies in the world are so stupid as to risk destroying their incredibly profitable, dominant monopolies on a technology that isn’t working after three years of usage?

Every piece of compute they turn on gets monetized immediately because the demand from customers is so high. Four independent, ruthlessly profit-maximizing monopolies don’t accidentally coordinate to destroy shareholder value at the exact same time.

GPUs and AI are not just a better way of doing computing, they are an entirely new way of doing business, and doing life for that matter.

Enterprises, governments, startups, and consumers alike are all adopting AI at a rapid clip because it delivers so much value and meaningfully improves their operations/lives. The revenue and earnings of the hyperscalers are accelerating off of larger bases than ever before precisely because these companies are integrating AI. Meta – which spent $69 billion on AI last year and is spending $125 billion in 2026 – uses all of its compute internally, and the company expects its revenue to grow 31% in the first quarter of 2026, faster than any quarter in the last five years! Meta is trading at 19x forward P/E for the value guys reading this.

We're not calling a bottom at this very moment, but these are some exciting pitches.

We don’t think we’ve seen a time when the entire market was this disconnected from the fundamentals. During COVID or the 2022 crash or the April Tariff crash, there were plenty of real reasons to be worried. But right now, the fundamentals of the economy, and especially fundamentals in The AI Revolution are, simply put, very strong.

The market seems to be trying to predict what might happen with AI and software somewhere down the line, but what the market is expecting is, at least for now, 100% opposite from what we are seeing on the ground.

Even legacy software businesses like Atlassian (TEAM) are reporting record numbers, growing backlogs, and increasing earnings even as they are supposedly being eliminated by AI. And the valuations, in many cases, are completely undemanding: TEAM is trading at 17x forward earnings growing 20% per year; The Trade Desk (TTD) is at 13x forward P/E growing 18% per year; Salesforce (CRM) is at 14x forward P/E growing 10% per year; just to name a few.

With respect to crypto (which is not the same as crypto stocks, obviously), we have to remain more cautious around crypto assets because there are no earnings or other fundamentals supporting the price of cryptos like there are with stocks. With respect to the crypto-adjacent companies that we own – Robinhood and Circle – those companies have real earnings, remain quite Revolutionary in their own rights, and are building platforms that real people and businesses (and in Circle’s case, real government agencies) use.

This week, we coined our motto for 10,000 Days Capital. The motto is “Vision, Discipline, and Patience (VDP).” We also decided we should periodically measure our VDP ratio, which is sort of a proxy for our conviction level. Right now, our VDP ratio is perhaps at its most attractive level ever with respect to our holdings.

Markets in panic lose their VDP. Our job is to keep ours when others abandon theirs.

Cody Willard and Bryce Smith

————————————

"Inside the thinking of Kevin Warsh - Trump's proposed new Fed Chair”, 9/2/26By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

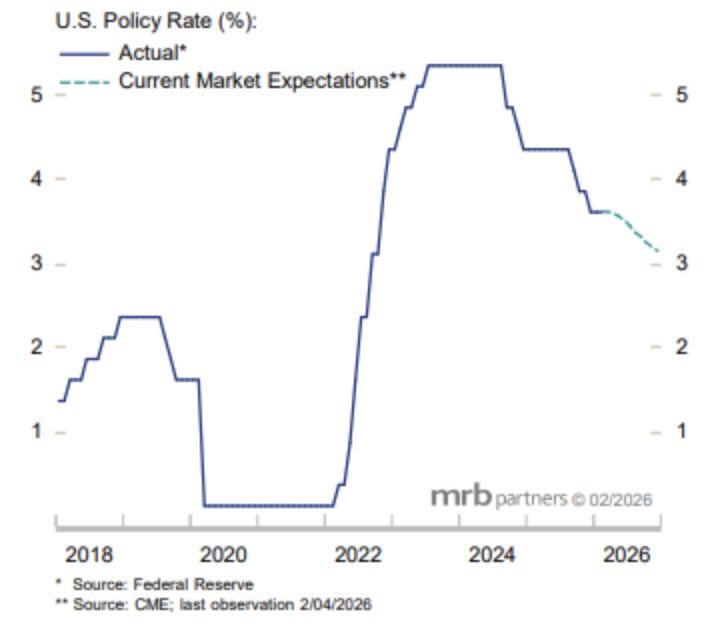

The Trump Administration has made its views on Federal Reserve policy unambiguous: interest rates are seen as too high, and the Fed should be cutting rates irrespective of prevailing economic conditions. Against this backdrop, the nomination of Kevin Warsh as the next Fed Chair initially appears counter-intuitive.

During his tenure as a Federal Reserve Board governor between 2006 and 2011, Warsh developed a distinctly hawkish reputation, criticising the expansion of the Fed’s balance sheet and warning of its inflationary consequences. As recently as 2024, he argued that rate cuts were inappropriate while inflation remained elevated.

Since emerging as a serious candidate for the chairmanship, however, Warsh’s tone has shifted. He has criticised the Fed for being overly cautious in easing policy and now attributes much of the inflation problem to what he describes as a “bloated” balance sheet. Warsh argues that a meaningful reduction in the size of the balance sheet would allow the Fed to lower interest rates. He has also proposed altering its composition, favouring Treasury bills over longer-dated Treasuries and other securities.

Warsh wants to shrink the Fed's balance sheet

If implemented, these proposals would represent a significant regime change in the conduct of monetary policy, with potentially material implications for bond markets, including a steeper yield curve. That said, Fed policy is determined by committee consensus rather than by the Chair alone. In our view, Warsh will struggle to secure sufficient support within the Federal Open Market Committee for some of his more ambitious ideas.

Most FOMC participants estimate the neutral policy rate to be around 3%. As a result, there may be scope to lower rates toward that level, particularly given political pressure and a leadership shift. This path is already reflected in market pricing. However, the macroeconomic backdrop would still need to justify such moves. Recent FOMC commentary suggests that either a clear deterioration in the labour market or sustained evidence of easing inflation risks would be required to secure majority support for rate cuts later this year. At present, neither condition appears imminent.

Investors expect rate cuts under the new Fed Chair

The FOMC comprises seven Federal Reserve Board governors, the president of the Federal Reserve Bank of New York as a permanent voter, and four rotating regional bank presidents. This year’s regional voters have generally signalled limited appetite for further easing unless inflation moderates meaningfully. On the Board itself, Warsh will fill a seat that was until recently temporarily occupied. If Chair Jerome Powell steps down from his role as governor after his term ends in May, the Administration would gain another appointment, potentially creating a narrow pro-easing majority. If Powell remains, that camp would be in the minority.

In either scenario, Warsh is highly unlikely to command enough votes to push through rate cuts that are not supported by incoming economic data. An “ideological” easing of policy remains improbable.

Support for shrinking the Fed’s balance sheet also appears limited. First, the argument that the balance sheet is excessively large is inconsistent with the Fed’s current operating framework. Balance sheet reduction was halted last November amid concerns that reserves could become too scarce, risking renewed volatility in short-term funding markets, as seen in 2019. To accommodate growing demand for reserves and currency, the Fed has since resumed monthly purchases of Treasury bills to maintain ample reserve levels.

Second, the FOMC has explicitly committed to operating in an ample-reserves regime. Within this framework, the size of the balance sheet has little bearing on inflation or economic activity, provided reserves remain sufficient. Monetary policy is instead transmitted through the interest rate paid on reserves, which anchors broader funding rates and influences credit conditions.

Third, a return to the pre-2008 scarce-reserves regime would be operationally complex and economically redundant. It would not lower the optimal policy rate, contrary to Warsh’s claims, and would reintroduce the need for constant reserve fine-tuning—an unnecessary complication given the current system.

Moreover, a substantial reduction of the balance sheet to pre-GFC levels would likely require disruptive asset sales, effectively a renewed phase of quantitative tightening. Such a move would place upward pressure on interest rates, directly conflicting with the Administration’s objectives. As a result, the probability of a significant balance sheet contraction appears low.

Where Warsh may find some traction is in adjusting the composition of the balance sheet toward shorter-dated Treasury bills. This would likely require coordination with the Treasury, potentially involving swaps of long-dated securities for bills and a shift in future issuance patterns. Such changes could better align the Fed’s assets with its short-duration liabilities, reduce portfolio income volatility, and shorten duration without increasing bond supply to the private market.

Warsh has also criticised the Fed’s forward guidance, including the dot plot, and expressed scepticism about the absence of a formal policy rule. While this may lead to incremental changes in communication, any adjustments are likely to be cautious to avoid unsettling markets.

In summary, while political pressure to ease policy will intensify under Warsh’s leadership, rate cuts will remain conditional on economic evidence. Meaningful balance sheet reduction is unlikely, though a gradual shift toward a more conventional composition may be achievable.

Justin Oliver

————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 7/2/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 estimate takes the MCAS December 2025 estimate and deducts the estimated charges of the Astro feeder fund. *** Morningstar as at 7/2/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2026 Freedom Asset Management Limited.