.jpg)

Weekly Newsletter

Freedom Calls: 9/3/26, God bless the UAE…. and the headless cockroach meets its match

by

From the Team at Freedom Asset Management

March 9, 2026

15 Minutes

Freedom Calls: 9/3/26, "God bless the UAE…. and the headless cockroach meets its match"

From the team at Freedom Asset Management

It has been a nervous week for anyone with teams, clients, friends and business partners in the Middle East, especially the UAE. But it has also been a week of great warmth shown by so many people around the world towards the people of the region unjustly targeted by Iranian missile and drone attacks.

The largest part of that practical support, without doubt, has come from the exemplary UAE military who have done a spectacular job of taking down so many of these projectiles (see below) - indeed the greatest risk of personal injury has come from falling missile debris, not the missiles themselves. We are grateful to the UAE military for keeping our people safe.

Daily recorded missile and drone attacks in the UAE

On behalf of everyone at Freedom, we are also grateful for the kind words of support we have received from clients and partners; our team has worked from home and has not missed a beat whilst the missiles and drones have threatened overhead, and the team have got used to the French Rafale fighter jets patrolling the skies above Abu Dhabi.

And although it is not over yet, where do we go from here?

The Iranian leadership - the headless cockroach meets its match

It is said that if you chop the head off a cockroach, it can look unpleasant and wander around for another 2 weeks before it dies. And that is how I characterise the Iranian regime position right now.

There can be no doubt that the US/Israelis will win this war. They have taken out the Supreme Council leadership and the military leadership at so many levels that it is improbable to believe a sustained and systematic defence and offence from Iran can be maintained for much longer.

I simply don't believe the line that the Iranians are saving their best missiles until after "they have used up the old ones to deplete the interceptors", as some claim. When you are being pounded by Israeli and US bomber command, for every hour you don't fire your best missiles, the less likely it is that you will be able to deploy them. Israeli intelligence has shown an incredible mastery of the Iranian military force's command and control capabilities, and also its missile launcher and storage locations.

And whilst we cannot rule out the possibility of something significant slipping through the net causing upset, fear or worse, the reality is that the Iranian regime, a sponsor of global terror and war, is being crushed and will never look the same again.

What next in terms of Iranian leadership?

It is interesting that the President of Iran, Masoud Pezeshkian, has not (yet) been taken out by the American/Israeli alliance. And whilst he spoke to apologise to his Gulf neighbours for the recent attacks on Saturday and said they would stop, the fact that they continue shows that it is the Army in charge in Iran right now - not him, or the clerics (which is what we said last week). I suspect that this morning's announcement that Ali Khamenei's son, Mojtaba, has been selected as the new Supreme Leader will change little.

At the Munich security conference 3 weeks ago, the son of the former Shah (King) of Iran, Reza Pahlavi, was doing the rounds with a proposal where he would come in as a transition candidate with a view to some kind of democratic elections some time afterwards. That proposal according to (former) General Petraeus was being given serious consideration.

The Americans have learned from Iraq, and this time they do not plan to completely remove the institutional apparatus of the civil service (as they did in Iraq) - the working assumption is that they just plan to control the top to ensure the country does not descend into even more economic chaos than it was in two weeks ago. That feels like a smarter solution. Let's see, but that does look rather like a version of the Venezuelan model, which for now seems to have "worked" in that Venezuela has not descended into internal chaos, although opinions do vary widely on this subject.

The Americans are not fond of kings, but in the Middle East as a model it does work, and mercifully in the UK we still have the Royal family albeit in a largely symbolic role, because otherwise we would only be left with oscillating administrations of competing clowns with little understanding of basic economics. So Trump should not discard the royal family option.

What does the world look like after this is over?

I have always considered Trump to be a fairly easy person to read - and if you were cynical, you might suggest from the US perspective that this is really all about US control over global oil and gas supplies - and support therefore for the US petrodollar system, which ensures the US dollar's dominant reserve currency status - ergo, a cheap source of finance for the US government for many years to come.

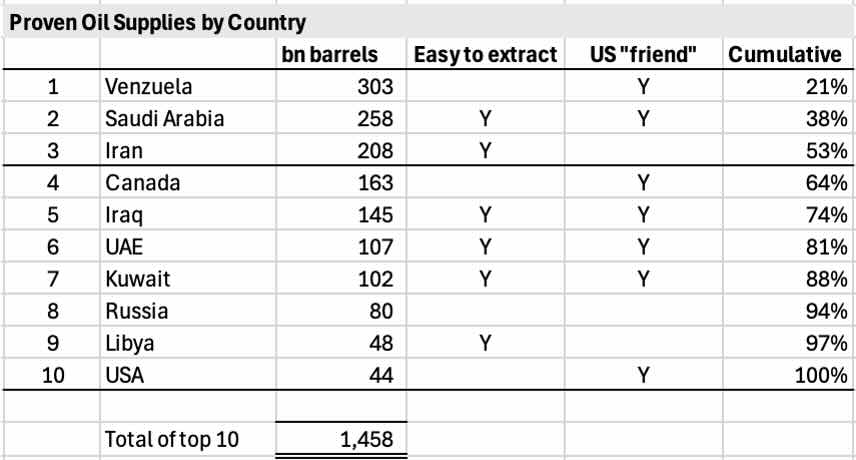

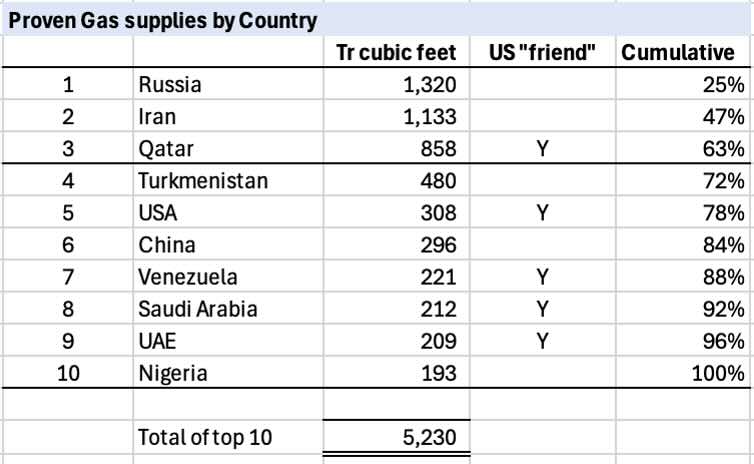

A simple look at proven oil and gas reserves (see below) shows that 3 countries control over 50% of the world's proven oil and gas reserves. I have overlaid (again very simplisitically), US friends or foes and how easy it is to extract the oil.

Source: Wikipedia, 2024, using lowest level in the range

Source: Energy Institute, 2025, using lowest level in the range

And strangely enough, Iran makes the top 3 in both lists. If you then consider that extraction of Iranian oil is relatively easy compared to what they make in Venezuela, the US oil companies will be given first pick of the spoils of war and a more secure and cheaper source of oil will flow on to global markets. The opex per barrel to get Iranian crude out of the ground is $5-8/bbl compared to $25 in Venezuela. The main issue, however, will be how much damage is done to the infrastructure during the Israeli/US bombings.

All this is bad news for China, because they were the main purchaser of Venezuelan and Iranian oil and gas - and as such it weakens China's energy independence.

Who are the other losers in this war?

So China as we have already discussed is a loser, but not a big loser. It was counting on Iran as part of its Belt and Road Initiative (BRI). China will now be increasing its dependence on Russian oil and gas. And some speculate that it will diminish China's ability to stomach a near term confrontation with Taiwan.

Europe always skilfully plays a losing hand. Europe had been counting on the supply of Qatari LPG after its spectacular failure at relying on cheap Russian gas, and then deciding to pivot away from unreliable US sources after Trump's recent aggressive move on Greenland. So that hasn't worked out for them.

Japan and certain Asian markets are at risk of higher short term oil prices. Speaking to our sources this morning, whereas 2 weeks ago, medium term crude prices were projected to be $60-65, that has now shifted up to $70-75 to reflect the time required to get Iranian crude back on track.

Even Trump in the short term is a loser as the US tries to focus in on the November Mid-term elections. Higher prices at the gas pumps mean higher inflation and that is bad news for Trump as we approach an election. So he is going to want to get the oil flowing quickly and cheaply again.

So what is the end game?

The war should be over soon - think weeks, not months - and maybe days

The world will be a safer place after this, with higher GDP prospects and lower energy price inflation - once Iranian crude is back on track

Risk assets should therefore perform

Cheaper energy should mean more AI adoption

And the US petrodollar retains its global dominance and therefore remains the world's undisputed reserve currency, meaning the US has a cheap source of finance for growth for years to come

And if I were a conspiracy theorist…. does Russia get a better deal in Ukraine for not helping Iran here … and does it all get done before the mid-terms?

The point is that even though this period is very nervous to watch from afar, and unpleasant to experience on the ground, we will get through this and the other side is a brighter day - especially for the Gulf countries.

So, this week we have a lot of articles for you:

Canaccord's Justin Oliver, Adviser to the Opus Global Growth Fund asks, "What do rising government debt levels mean for the resilience of the global economy?",

Sandrine Reynaud reports back on the recent trip to Tokyo, and tells us that "Japan is not so much a story of growth, but more of re-rating"

10,000 Days' Cody Willard and Bryce Smith, Advisers to the US Technology VIP fund remind us that "Technology accelerates through the fog of war"

Performance

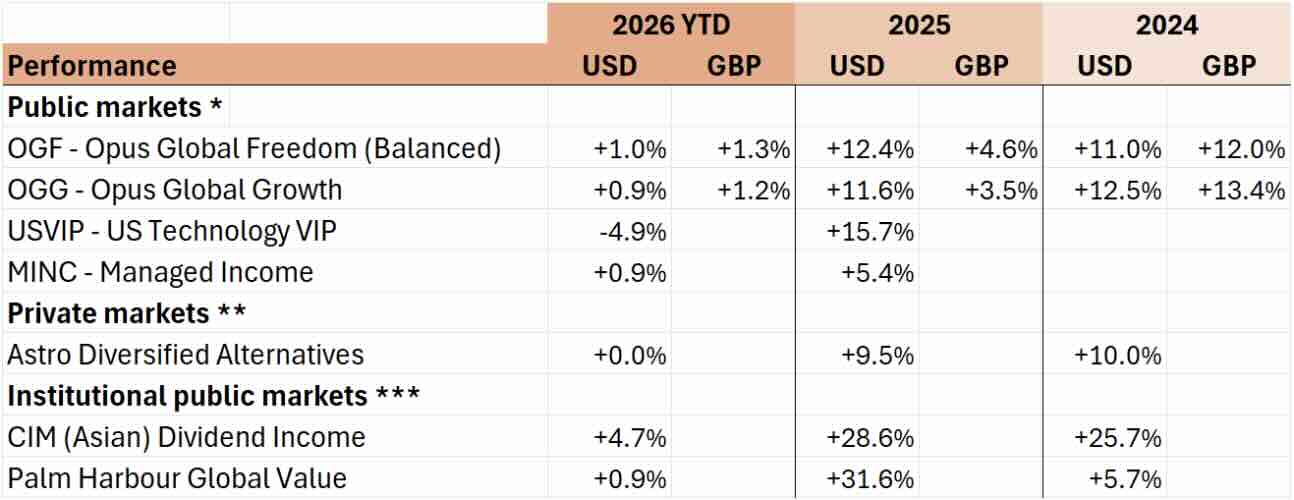

Naturally, last week was not a great week for most asset classes, but it wasn't a terrible week either. Below you can see that the risk off trade we did on OGF immediately prior to the conflict has helped significantly in relative terms. The biggest losers were Asian and emerging markets, because of the direction of oil prices, but we expect this market action to be short lived.

Sterling can be relied upon to sink when global risk appetite weakens and so for the first time this year, our Sterling numbers are ahead of our US dollar numbers. To all those commentators who predicted the long term demise of the US dollar, it might be (another) disappointing year.

Historically times of conflict have offered excellent entry points for fresh capital - so please do not hesitate to reach out if we can help. My guess is that we have another week or two of bumpy markets.

(For performance disclaimer please see foot of this email.)

This week I plan to be in London and Guernsey. Wherever you are, please make it a safe one again this week, and if you want to chat about anything, just message or call your usual contact at Freedom.

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

——————————————

"What do rising government debt levels mean for the resilience of the global economy?", 9/3/26By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Global debt levels were already at historic highs before the latest escalation in the Middle East, raising questions about the ability of governments to respond should global financial conditions deteriorate. According to the Institute of International Finance (IIF), total global debt rose by nearly $29 trillion in 2025, bringing the worldwide total to a record $348 trillion. The increase alone is roughly equivalent to almost six times the size of Germany’s economy, highlighting the scale of the expansion. While the rise has been driven primarily by the US, China and Europe, the trend is broad-based, with around two-thirds of the increase coming from advanced economies as fiscal deficits continue to expand.

Several structural factors have contributed to the sharp increase in borrowing. Governments have largely chosen to expand fiscal spending rather than pursue structural reforms, while accommodative monetary and funding conditions have helped support borrowing. In addition, rising investment related to artificial intelligence, alongside a renewed global push for defence spending, has increased capital requirements across both the public and private sectors. The shift towards higher defence spending has also been reflected in equity markets, with companies such as Lockheed Martin, Northrop Grumman and RTX Corporation benefiting from the trend. Even prior to recent geopolitical developments, Japan, under the stewardship of Prime Minister Sanae Takaichi, raised its defence budget to a record $72.1 billion for the current fiscal year. In Europe, defence commitments were already expected to increase the region’s government debt-to-GDP ratio by more than 18 percentage points by 2035.

Despite concerns about rising fiscal deficits, demand for US assets remains robust. According to the IIF, global financial conditions remain sufficiently supportive to help mobilise capital for key national priorities, including defence spending.

Importantly, the perceived decline of the US dollar has yet to materialise. Strong international demand for US financial assets, including Treasuries, equities and corporate bonds, continues to reinforce the dollar’s role in global markets. By the end of 2025, foreign investors held a record $9.3 trillion in US Treasury securities, underscoring the continued safe-haven appeal of US government debt.

Market commentary also suggests that structural factors such as relative economic growth and interest-rate differentials remain the primary drivers of currency movements. Expectations for US growth remain comparatively resilient, and interest-rate differentials have moved further in favour of the United States since the start of the year.

As a result, recent dollar weakness (excepting last week’s counter-trend move) appears largely sentiment-driven and could stabilise if the US economy maintains momentum.

While global growth has remained relatively resilient, the rapid expansion of government debt raises longer-term concerns. The combination of fiscal stimulus, accommodative monetary conditions and rising private-sector borrowing linked to capital expenditure may increase the risk of periodic overheating or asset-price distortions in some markets.

According to the International Monetary Fund Managing Director Kristalina Georgieva, the global economy is expected to grow by around 3.3% this year, which she described as “positive, but insufficient” given the growing debt burden. Global public debt is approaching 100% of GDP, which she warned could become a significant constraint over time. Estimates from the Organisation for Economic Co-operation and Development place the average debt-to-GDP ratio for advanced economies above 110%, levels not seen outside of the pandemic period since the era of the Napoleonic Wars.

In this context, the latest geopolitical tensions may be more concerning than they otherwise would be. While global growth remains stable and interest rates manageable, elevated debt levels mean that many governments now have less fiscal capacity to respond to future economic or geopolitical shocks.

Justin Oliver

———————————————

"Japan is not so much a story of growth, but more of re-rating", 9/3/26

By Sandrine Reynaud, Co-Founder of Freedom Asset Management

Early spring is a beautiful time in Japan, when the cherry trees blossom. Adrian and I visited took the opportunity to visit the Japan equities’ managers to which OGG and OGF are allocated. They provided some interesting insights on a bourgeoning economy, but not the expected excitement of full bloom.

Pictured: early cherry blossom in the Imperial Palace gardens set against the CBD in Tokyo, February 2026

Everyone has been talking about the Japan trade. Japan's economy in early 2026 shows a mixed picture; with modest recovery and steady (but slow) growth, transitioning away from decades of stagnation and ultra-loose monetary policy, it is facing ongoing challenges of fragile domestic demand due to the aging demography, and as everyone, feeling the geopolitical pressures.

For the full year 2025, growth came in around 1.1%, a recovery from contraction in 2024, but momentum remains soft due to cost-of-living pressures and trade headwinds inc. U.S. tariffs under Trump impacting exports.

Internally, the economy is seen as resilient, with low unemployment, and a structural shift toward a "labour shortage economy" helping sustain wage momentum but the forecasts point to steady but modest growth of around 0.8-1.0% real GDP for 2026 (e.g., Goldman Sachs at 0.8%, BOJ and IMF-aligned views around 1%).

This modest growth is led by domestic demand — private consumption (supported by recent wage growth as mentioned above, government measures, and real wage improvements as inflation eases) and capital expenditure (capex). The managers mentioned that with an increasingly aging population and c. 100% employment, younger employees can now “name their price” helping to improve consumption and pushing companies to rethink the operation efficiency and invest rightly in automation, software, and R&D. The latter is also improving the profitability of companies faster than the wage increase; however the top line growth is still slow.

To fill the labour shortage gap, Japan has incentivised women employment participation and interestingly employment of elderly which can be felt in Tokyo when you jump in a taxi or observe the number of people minding the roads. Whilst Tokyo may have some of the skyline and building blocks of NYC, it does not have the same buzz.

The stock market Nikkei index did not breach its all time high for 30 years (since 1989), over that time the S&P500 grew 19.6x and Dax 13.7x; companies are also much cheaper on a price to book ratio and companies in Japan have one of the lowest valuations - cash rich with little debt (with the exception of Softbank). Valuations have also been improving with reforms pushing for better governance, willingness of returning cash to shareholders via dividends or buy-backs.

While to foreigners including their Chinese counterparts, Japan may feel cheap because of the yen depreciation; the cost of living, healthcare and real estate are still high for the Japanese who have seen little wage inflation for 30 years. It is worth noting that wages are still lower than compared to South Korea, Europe/US and close to the average annual salary in Shanghai or Beijing.

Japan is navigating a delicate reawakening: moving from super-deflationary stagnation to mild inflation and normalization under Prime Minister Sanae Takaichi's administration, which emphasizes proactive fiscal policy (e.g., investment pushes, household support) while managing high public debt/GDP of 263%, which nobody seems to be worried about in Japan!

Domestic fundamentals look solid (firm consumption, higher corporate profits, wage gains), but the recovery is fragile — small shoots, but definitely good value.

For the value investor right now Japan ticks a lot of boxes.

Sandrine Reynaud

—————————————————

“Technology advances through the fog of war", 9/3/26

By 10,000 Days' Cody Willard and Bryce Smith - Advisers to US Technology VIP Fund

First off, we hope all of our friends in the Middle East and elsewhere in the world are staying safe. War is ugly and it brings with it lots of uncertainty (i.e. the Fog of War) and that's not great for markets.

But on the other hand, one of the fundamental tenants of our Revolution Investing strategy is “trusting our analysis,” and right now, our analysis continues to tell us that the fundamentals of our holdings continue to improve.

The AI, Robotics, and Space Revolutions we focus on are only continuing to gain steam, and geopolitical and major macro events like the ones we are living through today actually tend to accelerate the adoption of these technologies, not set them back.

COVID, tariffs, the financial crisis, and nearly every other big macro event over the last 20 years presented amazing buying opportunities in the names like those we own in the USVIP portfolio. And importantly, those events in and of themselves actually led the world to adopt technology more rapidly than ever before.

You can even go as far back to WWII and see how that unprecedented conflict, as horrible as it was, actually dramatically increased the velocity of technological advancement. Here are just a few of the foundational technologies to come out of that war:

Electronic Digital Computing

The Cavity Magnetron (Microwave/Radar)

Synthetic Rubber and Petrochemicals

Liquid-Fueled Rocketry

Mass-Produced Antibiotics

Nuclear Fission

Pressurized Cabins and Jet Engines

In today's wars (including Ukraine as well), we've already seen how critically important such technologies as AI, drones, cyber security, and space-based communication have been in shaping the conflicts. Modern war fighting is more about technological and logistical coordination than it is maneuvering divisions of troops on battlefields.

But by its very nature, war brings uncertainty and that tends to hurt equity valuations in the short term. But war doesn't change the fundamental calculus for tech investing. And we've seen throughout history how it is times like these that actually present some of the greatest buying opportunities in history.

While the companies we own aren't pure “defense” plays, they actually produce some of the most critical tech infrastructure needed to fight the modern war. A few examples:

SpaceX (via SATS) Starshield provides ubiquitous communication coverage for all types of devices and personnel.

Google/Amazon cloud services are critical for military computing and analysis.

Meta/Anduril augmented reality head sets for special operations units.

Zscaler for cyber security defense against state actors.

Nvidia chips for every AI workload including critically important Anthropic and OpenAI models actively in use by the Department of War.

Regal Rexnord’s bearings and actuators in the F35 fighter plane.

In sum, war doesn't change the long term analysis for the stocks we own, and in fact, it often accelerates and drives the adoption of the most advanced cutting-edge technologies which are made by many of the companies in our portfolio. And we want to take advantage of the understandable fear in the market to increase our exposure to the most Revolutionary companies on the planet building the platforms upon which modern society, both civilian and military, grow ever more dependent.

Our thoughts and prayers to everyone affected by these conflicts and we look forward to seeing our friends in the Middle East soon.

Cody Willard and Bryce Smith

——————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 8/3/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 estimate takes the MCAS December 2025 estimate and deducts the estimated charges of the Astro feeder fund. *** Morningstar as at 8/3/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2026 Freedom Asset Management Limited.