.jpg)

Weekly Newsletter

Freedom Calls: 8/12/25, The desert is good for the soul… and get ready for the next 25 years of mind-blowing tech!

by

The team at Freedom Asset Management

December 8, 2025

7 Minutes

Freedom Calls: 8/12/25, "The desert is good for the soul… and get ready for the next 25 years of mind-blowing tech!"

From the team at Freedom Asset Management

The desert is good for the soul…

We sneaked a couple of days off for the occasion of the UAE’s 54th National Day. A 2.5 hours' drive out from central Abu Dhabi is the desert resort of "Qasr Al Sarab", which is best described as “the middle of the desert meets The White Lotus”. If you haven't seen "The White Lotus" (on AppleTV), think: Asian rich kids, Instagram-city, honeymooners, octogenarian German billionaire family brings out the multitude of grandchildren on holiday to impart the meaning of life etc etc…

Pictured: Early morning desert walk at Qasr Al Sarab, Dec 2025

Anyway, you do get plenty of time to wander through the endless, seductively beautiful desert - and that makes you think about a lot of things – mainly because there is absolutely nothing else going on at all. For me, it was thinking through asset allocation and "what have we missed out on this year?"

We certainly haven't missed out on revolutionary technology (thank you Cody and Bryce - and more from Cody on this further down), or Defence (thank you Charles), or some of the best performing Asian, Japanese and EM funds (thank you Ramon, Florian and James), but what about next year? And are we missing something in Europe?

So this got me thinking about real estate, because in some respects real estate is the very expression of economic growth and prosperity.

Is Europe "over"?

There was a time in the UK when you got yourself on the property ladder as soon as you could, leveraged yourself to the max, and just kept on climbing that ladder with more leverage until you got to the “top”. The top was defined here as the “full nest” family home, which because of all that market growth and all that leverage meant that you were sitting on a lovely pool of equity. Then when the "empty nest" came, we were supposed to downsize, release all that equity and turn that into a pension pot (or buy another smaller unit to rent out for pension income). That model's not working now.

So two things that make me think "Europe is over", for now:

This weekend, I glanced the pages of www.PrimeLocation.com, which lists amongst other things smart residential real estate in London. It was shocking for me to see that an apartment today in the best part of Kensington trades pretty much where it was in 2012. And that is the asking price - not the sale price, which can be up to 25% lower in this market. What happened to the last 13 years? And speaking to a UK institutional real estate asset manager over the weekend, he thinks there is more uncertainty to come;

Last week, we sat in on a call with German real estate developers on a fund that our institutional business bought into 5+ years ago. Most of those assets are in Berlin. The mood on the call was pretty grim - the banks are not lending to real estate developers, and therefore development land is just not moving. This asset manager believes they need to extend the fund for another 5 years to see the market return to some sense of normality - forget about growth right now. Apparently, the only bid to pick up secondary LP positions in this fund is at c. 50c/$1. Ouch.

In contrast, our adopted home in Abu Dhabi is bristling with activity - real estate developments are flying off the shelves and new communities of wealth are being built for the next 25 years.

I am not saying Europe is over forever - it's just that its not where the game is going on right now.

And whilst the value investor will always find opportunity (e.g. I am sure there are some absolute gems you can pick up for a great price), it does mean that some of those values we were taught about wealth creation and preservation (through real estate) are no longer holding true.

This is especially the case when you think that acquiring property comes with significant costs of carry: taxes, upkeep, more taxes, annoying tenants that keep breaking things, a boiler that needs replacing etc… It has always surprised me that every home we have ever owned always seems to end up costing about $20,000 a year on "non-value-creating-stuff" (all those things listed above). So your real cost of carrying property (excluding financing costs and management fees) over 10 years can be $200k - on a $1m apartment that is 20%. (Now the "closet socialist" in me can also see how this is could be good news for property affordability for the younger generations, but we will keep that socialist firmly in the closet for now!)

So compared to real estate, the cost of carrying stock market investments, especially through managed funds is very low indeed; there are no random cheques to write and the upstairs' apartment's bathroom does not leak into your living room, there are no well meaning groups of Romanian builders to manage from afar. And in public markets, you can sell your investments quickly if you need your money for other things (typically in a week with Freedom).

So when we are thinking about building wealth for the next 10 years, it is not unreasonable to put more money to work in global stock market funds than we might have done previously.

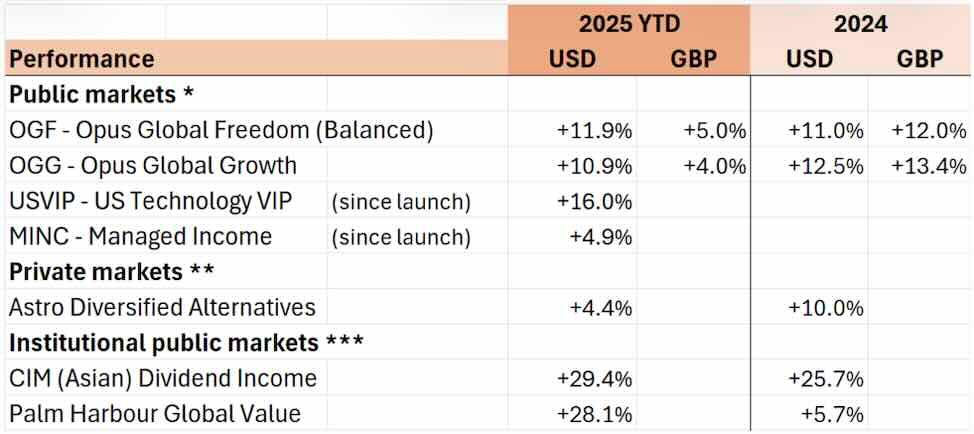

Performance - a good week all round

(See performance disclaimers below)

A good week all round also meant a strong week for USVIP. And much to validate Cody's article below, it means that every investor in USVIP is making money; it does not matter if you bought on the "worst" day before the April tariff crash, last week, or the wobble of a 3 weeks ago - everyone is up. It is never too early, or too late, to invest in the technology that will radically change humanity over the next 25 years.

It is also pleasing to see our balanced and growth strategies putting in another year of double digit returns. Hopefully, we will not see any more wobbles before the year end so we can "bank" those returns. It is worth remembering that interest rates are close to 3.75% now - and headed on a downward trajectory next year, so our balanced and growth strategies look like sensible choices against that context.

Our articles this week:

Cody Willard from 10,000 Days, advisers to US Technology VIP (USVIP), tell us how "Humanity's next 25 years will dwarf all history"

Justin Oliver from Canaccord, adviser to Opus Global Growth (OGG), also a believer in the impact of AI, takes a look inside OpenAI's balance sheet and looks at the current "bear" case for AI stocks - and concludes that while risks around funding, depreciation and competitive shifts are real, the broader story remains one of expanding productivity and a still-bright outlook for the AI-driven economy. He writes for us on "what does OpenAI's balance sheet tells us about the AI economy".

Please scroll down to read the articles.

This week I start with Abu Dhabi Finance Week and will spend the rest of the week in Hong Kong.

On Thursday we will be hosting a webinar with Cody on the US Technology VIP Fund.

Please use the link (or cut and paste the link) below to register:

Wherever you are let me wish you a wonderful and prosperous week ahead - and I hope to see you on the webinar Thursday!

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

———————————

“Humanity's next 25 years will dwarf all history”, 8/12/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

While I was traveling in London a couple weeks ago, I had this epiphany about just how much value creation has been done in the last 25 years and just how much we should probably expect to see over the next 25 years …and I haven’t been able to stop thinking about it since. What you’re about to read will blow your mind. Frankly, it’s probably the most succinct, accurate and important analysis that I’ve ever produced and it’s relevant for any and all investors out there because it underscores how Tech Revolutions are what drive most of the prosperity, wealth and gains in the economy and markets over time.

I want you to do some deep thinking. Let’s think of every fortune in the last 6,000 years (since the beginning of human civilization), including The House of Orleans, Mansa Musa, John D. Rockefeller, Cornelius Vanderbilt, Jeff Bezos and Elon Musk. Think of all the miraculous achievements that humankind built in that amount of time, from the Roman aqueducts to the entire electrical grid, the Internet, every software program, every video game, every professional sport league, all modern industry, smartphones, satellites… every economic transaction, every purchase, every building, every highway, etc etc etc. Think of the cumulative effort of the roughly 117 billion people that have lived on this Earth.

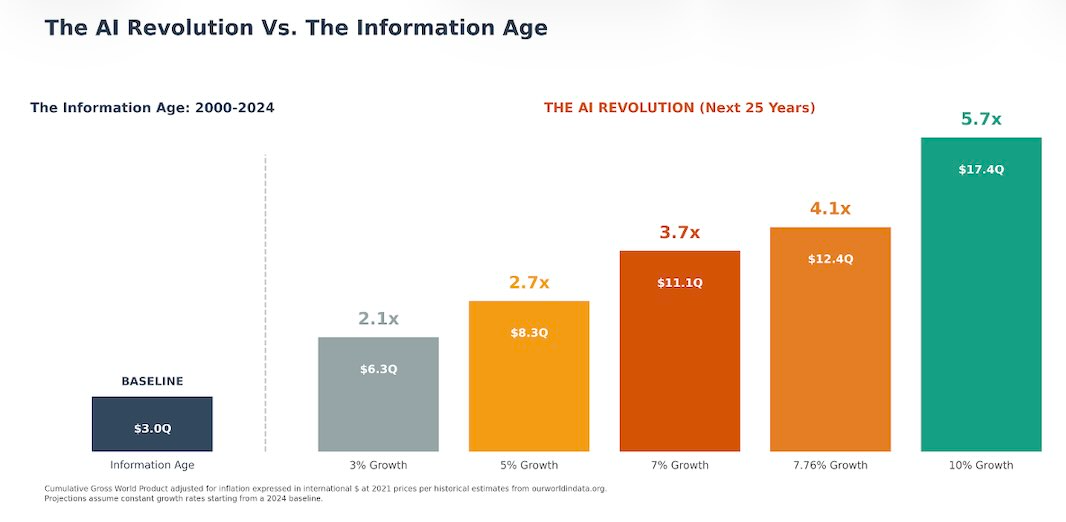

Half of the world's total wealth was created in the last 25 years

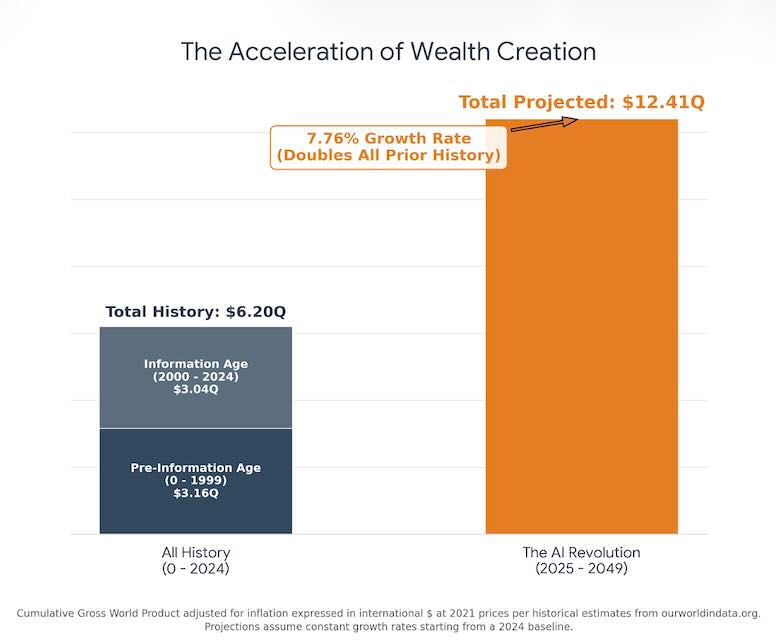

Now realize that half of all that wealth, prosperity, value, services, applications, buildings and products were built over just the last 25 years, during the “Information Age.” You read that right. More importantly, over the next 25 years, we will produce more than 2x all of the wealth, prosperity, value, services, applications, buildings and other products produced during the last 25 years.

And even MORE importantly, at just 3% annualized growth, the economy will produce about the same amount of wealth in the next 25 years as it did in all of human history combined!

Moreover, there’s a better than 0% chance (and probably better than 50% chance) that we double or triple the entire sum of historical Gross World Product (GWP) in the next 25 years. At a 7.76% real growth rate, we would produce 2x the amount of wealth in the next 25 years compared to the last 6,025 years combined.

This is possible because:

The AI Revolution is about to revolutionize all white collar jobs and make supply chains, customer resource management and other facets of business incredibly more efficient, which will enable all white collar workers to be 2-10x more productive, and

The Robotics Revolution is about to revolutionize all blue collar and all health care and other physical jobs, making them incredibly more efficient and 2-10x more productive, and

The Space Revolution is about to take our earthly GWP to a galactic GWP over the next 25 years

Furthermore, earnings/profits/operating margins were stagnant for most of the 1700s to the 1900s, but with the advent of computers, internet, mobile devices, apps, software, etc, earnings/profits/operating margins secularly expanded dramatically over the last 25 years. AI and Robotics will obviously help that trend of expanding earnings/profits and margins over the next 25 years too (perhaps even at an accelerating pace).

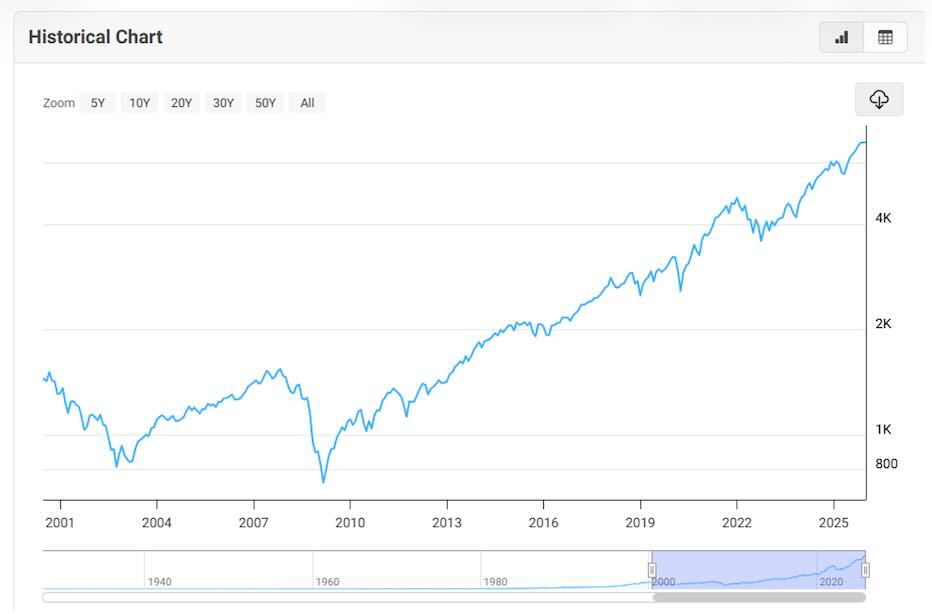

The amazing growth, higher margins, and wealth creation we witnessed over the last quarter century obviously showed up in the stock market.

Pictured: S&P500 returns: 1/1/2000 to date

You might think that these kind of returns were unique to the last 25 years, but just consider what the charts looked like coming into the millennium:

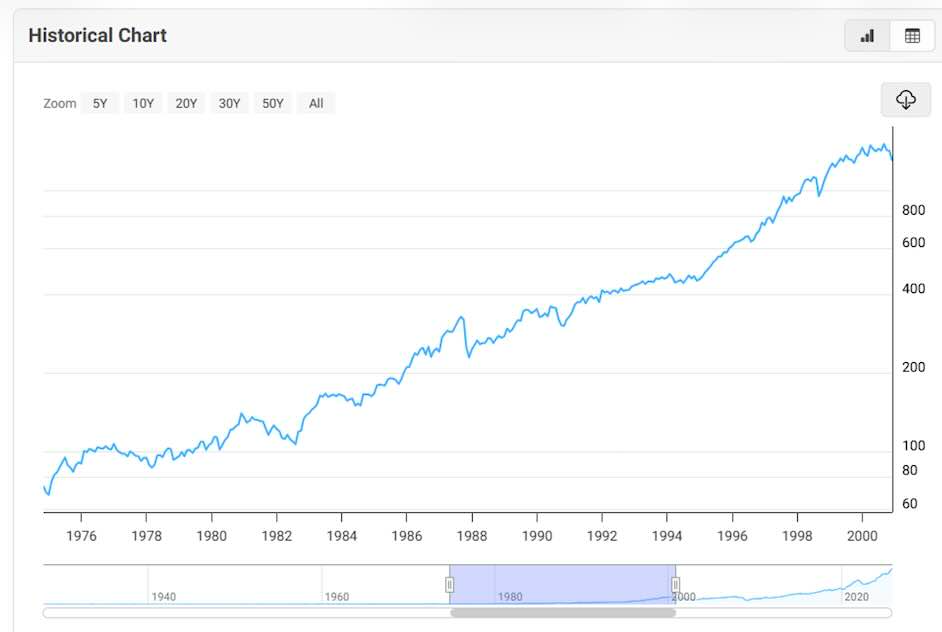

Pictured: S&P500 returns: 1975-2000

Pretty much the same "up and to the right" dynamic. So even if you bought in the highs of the 2000 bubble, you still saw fantastic returns over the next quarter century because of the amazing wealth creation (the economic doubling of the prior 2000 years) we saw in the 25 tech-empowered years that followed. And what about the 25 years before that (1950-1975)?

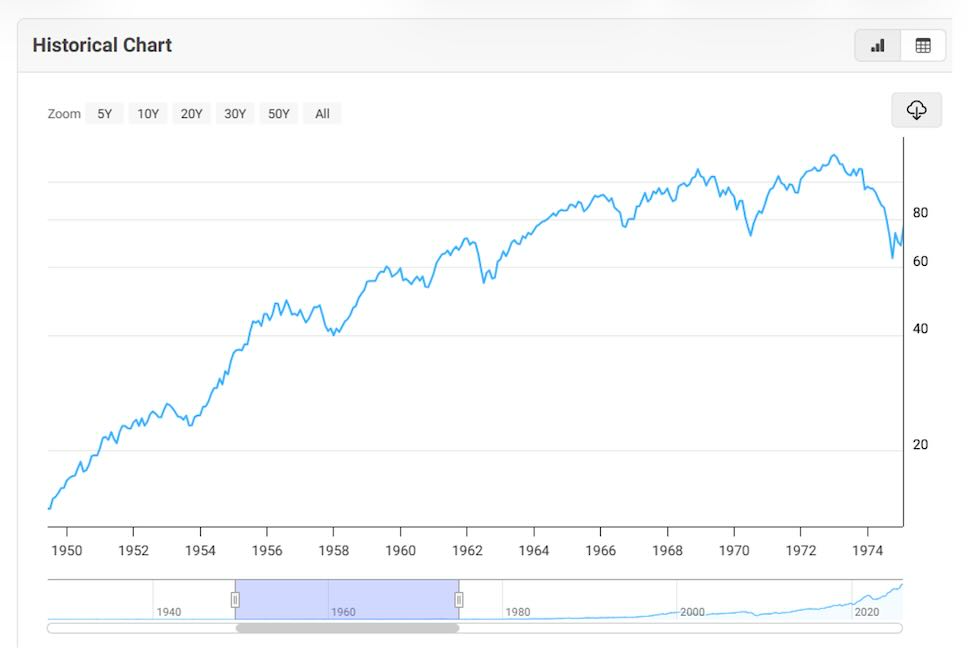

Pictured: S&P returns 1950-1975

Remarkably, pretty much up and to the right. Obviously, there are hiccups and downright crashes along the way (as there will continue to be), but we can see that in almost any 25-year period of the markets within the last 75 years – since tech (chips, computers, internet, smartphones, etc.) – really took off, buying even at the short/medium-term tops still yielded fantastic results over a 25-year investment period.

And to be clear, tech was the primary wealth creator of the last 50 years, and it notably accelerated in the last 25 years (The Information Age). In the years before 2000, a good chunk of the growth in Gross World Product (GWP) was driven by population growth.

From 1975 to 2000, the population grew from ~4 billion to 6.2 billion, a 1.77% CAGR. However, in the most recent quarter century, population growth slowed to 1.12% per year. Meanwhile, the rate of real GWP growth expanded to 3.35% from 2.9% annually.

Despite the fears of most economists, the GWP growth rate is most likely going to continue to accelerate as tech Revolutions drive even more productivity gains. With The AI, Robotics, and Space Revolutions coming down the pike, human productivity is about to explode, leading to even higher wealth creation per capita compared to the prior quarter century, which was in and of itself greater than the 6000 years that preceded it.

However, the wealth created over the last 25 years was not evenly distributed.

While just betting on the markets themselves was great, picking the winners of the tech Revolutions yielded truly fantastic results. The tech companies which drove the radical improvement in human productivity obviously captured most of the value, and that’s reflected in their outperformance of the market over the last 25 years.

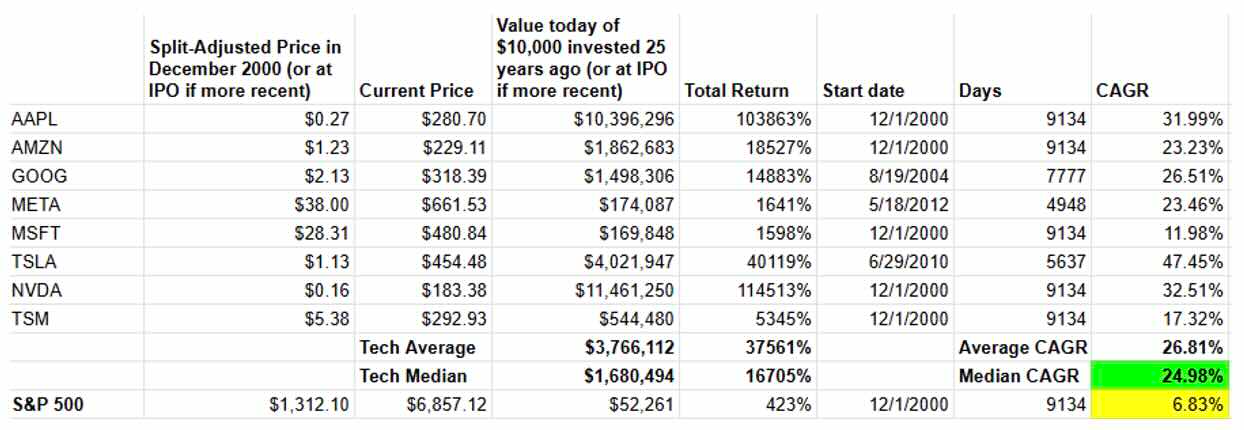

If we look back, the median compounded annual growth rate (CAGR) of the largest 8 tech companies was about 25% per year (25 years, 25% per year? Seems sort of mystical). That dramatically outperformed the S&P 500, which only returned about 7% per year.

Isn’t it wild that we’ve famously owned seven of these eight companies (no MSFT) for years/decades? And while 25% per year may not sound absolutely crazy, a $10,000 investment in just one of these companies yielded a median ending value of $1.7 million, compared to an ending value of just $52,261 if you invested in the S&P 500.

Other sectors that are not tech-based will also do very well over the next 25 years as these Tech Revolutions drive the economy and markets higher. But the vast majority of the hundreds of trillions of dollars of new wealth created over the next 25 years will be done by Revolutionary Tech companies, just as it was over the last 25 years and even over the last few hundred years.

Now let’s hit on inflation, as that is always a big concern for economists and is supposedly "bad" for tech. The economic returns we’re discussing over the next quarter century are real returns, i.e. the real increase in wealth and purchasing power (our 3% model is only slightly higher than the consensus 2% growth estimate). But interestingly enough, as long as inflation/deflation stays within reasonable bounds (say within -2% to +4%), the net effect of inflation is actually positive for stock ownership.

While inflation erodes purchasing power, it generally correlates with increased nominal financial asset prices over the long term. A distinction must be drawn between "real-world inflation" (the rising cost of goods like eggs) and "financial asset inflation" (the rising value of stocks). Over a multi-decade horizon, equities tend to act as a hedge against currency devaluation because financial assets are distinct from fiat currency; as the supply of dollars expands, the nominal value of finite assets—such as company equity—rises relative to that currency. Consequently, a moderate level of inflation can boost stock returns on paper, even if it does not reflect an increase in real economic output or prosperity.

Moreover, as the population has grown exponentially wealthier over the last 50 years, and especially the last 25 years, we allocate a much higher percentage of our income to asset ownership, rather than spending. Especially post COVID, we have observed a phenomenon where liquidity flows disproportionately into financial assets rather than consumer goods.

This is accelerated by the structural shift in how society allocates capital, with a growing percentage of income being funneled into markets and assets rather than consumption (the "financialization" or "RobinHoodization" of the economy).

The huge rise in stock ownership by individuals, the explosion of crypto/sports betting/prediction markets, are all the result of relatively wealthier people allocating a relatively higher percentage of their income to asset ownership. That results in stock prices generally trending upward with inflation (unfortunately it also invites a lot of grifting, fraud, and mindless speculation).

Of course, if inflation blows way past the long-term norms (like when it shot to 9% post COVID), that shocks the whole system and can be bad for asset prices in the short term (i.e. 2022). But outside of that, mild inflation actually isn’t too big of a problem for people investing in tech Revolutions, like us.

All of this doesn’t mean we won’t have market downturns, crashes, bubbles and economic cycles over the next 25 years.

After all, we did have three serious economic recessions and three market crashes over the last 25 years even as we doubled all the prior economic activity of history. But over the last 25 years, as long as the investor was able to survive those market crashes, you made a ton of money in the long term.

And over the next 25 years, if we’re right that the global economy can grow by at least 3% (or much more than that) and if margins stay here or (much more likely, actually expand) we will, by definition, see the stock markets go up by tens of trillions or even hundreds of trillions of dollars.

We have to remember that technological innovation (and Revolution) happens at an ever accelerating pace, as I’ve explained many times over the years. There will be as many or more medical breakthroughs, architectural achievements, communications applications, software step changes, etc over the next 25 years as there were in all of history too.

Therefore, the most important takeaway is as follows:

Invest in Revolutionary Technology. I mean, most of those many trillions of dollars of market cap that will be created over the next 25 years will, of course, be created by technology companies, specifically those companies driving The AI, Robotics and Space Revolutions. We only have to find a few of those 25%+ CAGR compounders to achieve fantastic results.

In conclusion, there’s literally never been a better time to be a Revolution Investor than right here, right now as there’s never been another time in history where tens or hundreds of trillions of dollars of revenue, earnings, profits – and most importantly – market cap are about to be created in the span of less than 10,000 days. Said another way – it will take less than 10,000 days to create as much GWP, earnings and market capitalization value as was created over the last 2,190,000 days.

Cody Willard

—————————————————

“What OpenAI's balance sheet tells us about the AI economy”, 8/12/25

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Normally I’d leave any comments on technology to the far better positioned, informed and educated Cody Willard and Bryce Smith, advisers to the US Technology VIP Fund! However, with two recent analyses having somewhat shaken investors’ faith that the AI boom will bring the kinds of returns they’d previously assumed, I thought it might be helpful to look at this through the lens of a humble multi-asset fund manager; and someone who has managed money through many cycles…

Looking inside OpenAI's balance sheet

The analysis published by HSBC last week, which dissects OpenAI’s extraordinary cloud-computing commitments, has rightly drawn considerable interest. It landed alongside renewed commentary from investor Michael Burry, who has been cautioning for months that the current enthusiasm for AI resembles a classic valuation overshoot. His concern is that aggressive depreciation assumptions are inflating reported earnings and that investors are placing too much faith in optimistic long-term revenue stories.

Despite those warnings, we do not view the re-rating of AI-linked equities as evidence of a speculative bubble.

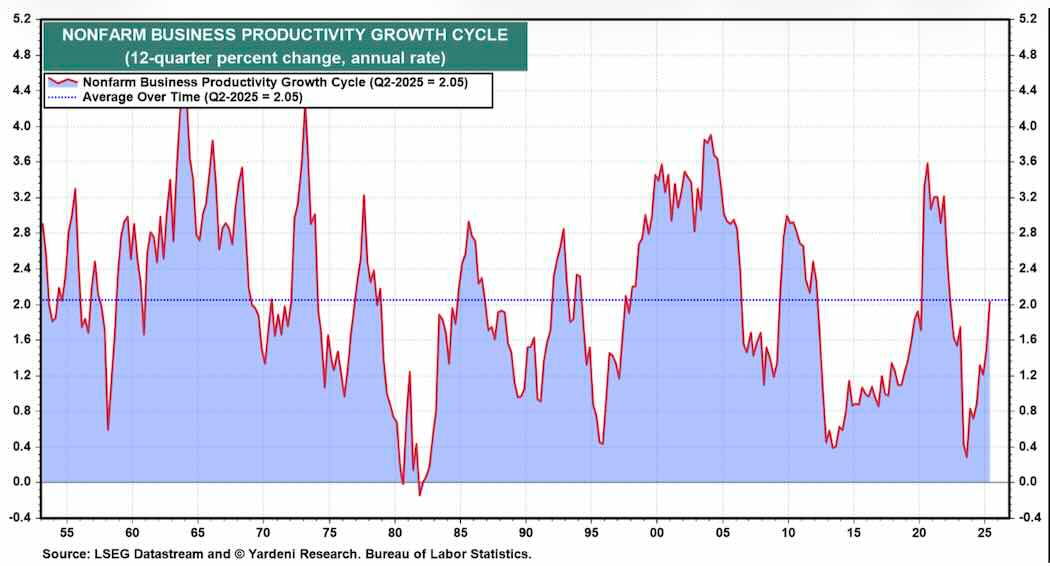

Rather, we interpret the surge in spending as part of an investment cycle marked by familiar early-phase overcapacity; something that has historically underpinned long stretches of technological productivity growth. Recent data already shows a meaningful lift in productivity, reinforcing the view that another sustained upswing may be underway.

Questions around funding models and accounting choices will persist, but the rapid acceleration in high-tech capital expenditure is laying the groundwork for what some have started to call the BRAIN revolution - biotech, robotics, AI and nanotech - advancing in tandem.

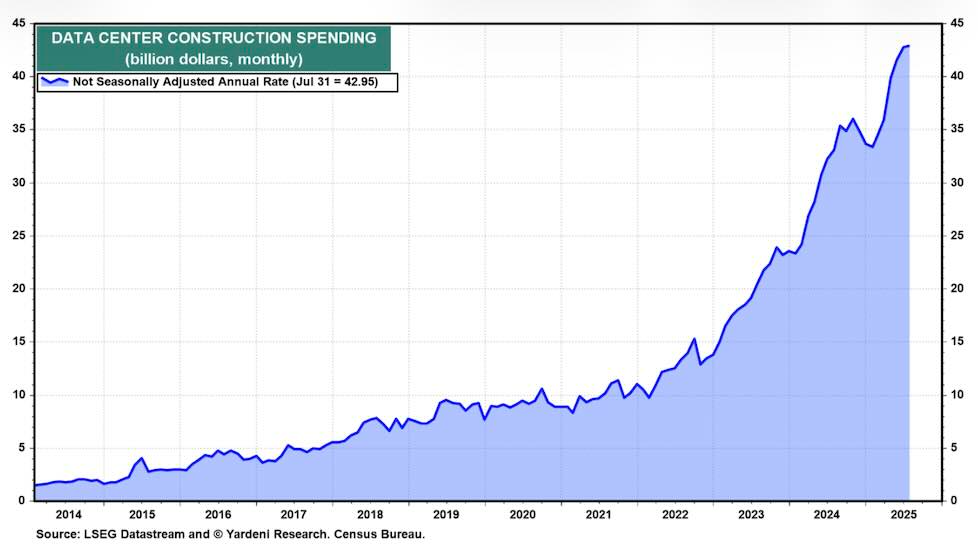

Major technological shifts have never been inexpensive, and generative AI exemplifies that reality: chip demand and data-centre construction have soared, highlighting the immense upfront physical build-out required to support large-scale AI. Should monetisation fall short, the gap between enormous fixed-cost infrastructure and modest realised revenue could become problematic.

HSBC models this risk explicitly, projecting that OpenAI could face a liquidity shortfall by 2030 even after assuming substantial cash inflows. Their base case incorporates roughly $282 billion in free cash flow through 2030, yet still arrives at a $207 billion funding gap once expected data-centre and compute-rental obligations are included. The modelling also assumes very bullish adoption: around 3 billion users, with 10% paying, and about $129 billion in consumer-facing AI revenue, mostly derived from search and advertising. These figures exclude enterprise revenues.

Although the Financial Times suggests HSBC may be overly conservative, the risks specific to OpenAI’s balance-sheet structure remain difficult to dismiss.

Burry’s depreciation critique sits alongside this. His argument is that hyperscalers are extending useful-life assumptions for AI hardware to five or six years, even though the realistic economic lifespan may be closer to two or three. (We note that this "realistic economic lifespan" point has been disputed in a recent note by Cody and Bryce - i.e. "old" the chips will continue to be used long after new chips have arrived, because there is insatiable demand for compute and the old chips will continue to run on the same improved software, so more chips = more compute).

That practice lifts current earnings but simply defers costs into the future. He estimates that under-depreciation across the sector could be overstating aggregate profits by as much as $176 billion.

Even so, while Burry highlights hidden strains and HSBC sketches a significant funding gap, the macro picture still points to several years of strengthening productivity and rising profitability. That underlies our constructive view for the remainder of the decade. Some firms will inevitably struggle under the weight of their own capital intensity, but capital tends to migrate toward viable operators, and productivity cycles rarely hinge on the fate of individual companies. Moreover, longer depreciation horizons have some merit: older GPUs can still be redeployed for internal or lower-intensity tasks. Growing pressure on power supply and compute capacity reflects demand rather than systemic fragility. Electricity prices are rising partly because data-centre consumption continues to grow. Meanwhile, S&P 500 operating earnings have repeatedly recovered through downturns and, in our view, retain room to trend higher.

One element missing from most coverage of the HSBC note is its overarching conclusion: AI is likely to permeate “every production process and every vertical,” creating widespread productivity gains.

That supports the view that the US could see several years of stronger GDP growth. Even incremental improvements matter in a $23.8 trillion economy. Just a few basis points of additional annual output can exceed the entire post-2020 surge in technology investment. In other words, modest gains on a very large base can overshadow even the largest cap-ex cycles.

Short-term setbacks remain possible. Early-cycle excess could weigh on semiconductor or construction names, and any spillover could temporarily pressure the broader cyclical complex. Yet the underlying productivity impulse should prove more durable and more consequential than any such correction.

As for Nvidia, competitive pressures are finally becoming more visible. GPUs remain the dominant tool for training AI models, given their flexibility and entrenched developer ecosystem. TPUs, by contrast, are specialised accelerators designed for efficient matrix operations and have been gaining share in model execution, where integration and efficiency matter more than general-purpose capability. Reports of Meta discussing TPU purchases with Google briefly unnerved investors, though markets ultimately stabilised. Google’s TPU performance, highlighted recently by Barron’s, underscores that alternatives are maturing. If hyperscalers divert even a portion of their demand toward TPUs, Nvidia’s pricing power could face pressure. It is unlikely to collapse, but competition has now arrived in earnest. Even with those competitive dynamics, the semiconductor sector as a whole remains on a healthy trajectory in terms of earnings, investment, and long-term growth.

In short: risks around funding, depreciation and competitive shifts are real, but the broader story remains one of expanding productivity and a still-bright outlook for the AI-driven economy.

Justin Oliver

————————————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 7/12/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 7/12/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.