.jpg)

Weekly Newsletter

Freedom Calls: 5/1/26, “The Venezuela issue …. And Happy New Year!"

by

The team at Freedom Asset Management

January 5, 2026

7 Minutes

Freedom Calls: 5/1/26, “The Venezuela issue …. And Happy New Year!"

From the team at Freedom Asset Management

First up, a Happy New Year to all our investors and friends of the firm! For all London’s problems - and there are many - it does nonetheless put on a great show for the New Year, with a spectacular (and not very ESG, or sustainable) fireworks display at midnight, and then a big parade through town on 1st January.

Pictured: London welcomes in the New Year, taken from the rooftop, Jan 2026

The Venezuela issue a.k.a "What does a guy have to do around here to win a Nobel Peace Prize?"

It was a very different kind of fireworks going off in Caracas over the weekend. I am beginning to think that Mr Trump may be on our circulation list. If you made it as far as the geopolitics section (No 3) in last week’s letter, you will remember we said:

“… Venezuela does matter, especially if it is being run by the “wrong” people, with the “wrong” friends… The working assumption on Trump is that he intends to depose Maduro and welcome in the opposition candidates. He would then like to see the return of US oil companies to Venezuela. It is all strategic, just not terribly peaceful."

What else does Trump achieve by forcing regime change in Venezuela (apart from said elusive Nobel prize)? Well, he sends a very powerful message to the rest of Central and South America, Moscow, Beijing and Tehran (in case they needed another one), that when he is negotiating, he is prepared to pull the trigger. It is difficult to say this was a fair fight - it seems the Venezuelans were completely overwhelmed. The skill now - a different one - is winning the aftermath and putting in place a legitimate government, but he has certainly made his point.

The Monroe Doctrine

Last week, I listened to a podcast on the (then) current situation in Venzuela and it was interesting that the Munroe Doctrine was being referred to. For those not familiar, the Monroe Doctrine, named after US President James Monroe in 1823 establishes the Western Hemisphere as a "US sphere of influence”. The Doctrine was aimed at curbing the ambitions of European colonisers; in it, the US also pledged “non-interference in European affairs” which, Putin may observe, hasn’t exactly played out as intended. The Roosevelt Corollary of 1904 subsequently re-interepreted Munroe to allow the US to intervene to restore internal stability in the Western hemisphere.

So, at least on Capital Hill, this is part of the authority for intervention in Venezuela. Interestingly, also in the same podcast, the point was being made that the “opposition" in Venezuela was doing the political rounds in Washington to convince US politicians that it was capable of governing the country after Maduro’s departure. So that all stacks up.

So what do we think happens now?

I did some calling around our sources at the weekend to get a picture of Venezuela. First of all, nobody liked Maduro. He kept the army loyal by paying them vast amounts of money and giving them power. This kind of loyalty can, in theory, be bought by the new incumbent. And clearly enough of his protectors took enough "facilitation payments" from the Americans to allow the US to come in pick him up and fly him out remarkably efficiently.

Of course we all imagined Mr Trump had a plan. From the available evidence it is not entirely clear that Mr Trump does indeed have a plan. He has already questioned the viability of the official opposition (the Norwegians won't be happy). But this could also just be bluster to get the opposition on message for the transition.

Make no mistake, right now, it is the army, the local gangs, and the Columbian gangs that are really in charge in Venezuela. And it seems difficult to believe that any of these groups are totally up for taking orders from Mr Trump or his friends, unless they come with bags of cash.

So there are fears a power vacuum appears quickly, and before we know where we are, this is Libya all over again. Let's hope not. One difference between Libya and Venezuela is that 8 million people have already left an economy where the GDP is down 70% over the last 10 years - so we are are already starting from a bad place, which is the main reason why we are here now. And there is a huge amount of support for the US from Venezuelans in exile. I think a key question is what support those networks have on the ground.

It might work, but there are a lot of people who will want to see it fail.

The Cuba angle

Cuba was responsible for stopping the brief coup attempt against Chavez in 2002. Chavez put the Cubans in the secret police and other senior positions; the Cubans are everywhere. Venezuela pays for this loyalty with oil. First up the Cubans will be worried about what has happened here. Cuba will fear that Trump may look at Cuba next - for a start, it is much easier to pull off than Venezuela, but there is no oil and not really much worth fighting over. But the Cubans will try every possible method on the ground in Venezuela to ensure that the US is not successful - as will most likely Lula in Brazil.

The Russia angle

This is a major blow to Putin. Although Russia has significant investments in the Venezuelan oil industry, even they were struggling to get their oil out, so most of those investments are effectively written off. But Putin will almost certainly be on the phone to his friends in Cuba and South America offering whatever help they need to scupper US plans.

The Venezuelan oil industry

Trump's angle that this will all be sorted with oil revenues does not easily compute. Yes, on paper Venezuela does have the world's largest proven oil reserves, but they is expensive to extract.

Venezuela is producing about 1m barrels per day (bpd) of oil (as a comparison the US produces about 13m b/d). Much of this is bought by China. The oil is heavy and the oil infrastructure is poor, after years of sanctions, corruption and under investment. To bring Venezuela up to about 3m bpd is possible, but it is a 5 year investment programme. All the oil fields are 60% owned by the state, so effectively the state has control over everything, albeit that it does not have the money to invest in the infrastructure.

The kind of money you would need to find to get Venezuela up to 3m bpd is something like $20bn for every additional 400k bpd - so you are looking at $100bn. This is less than the US has sunk into Ukraine, but it is still a very large number.

One of the biggest problems facing the Venezuelan oil industry has got nothing to do with the US - it is the current price of oil. At the current WTI level of low $50's/barrel, it is just not economic to develop those heavy oil fields. Capex alone will soak up about $25-35/barrel. So to get the oil industry investing again, we understand that break-even rates are around $70/barrel, and that is before we start pricing in political risk. Once the oil is flowing again, it is pretty straightforward to refine - the heavy oil is send up to the US to existing refineries. Chevron is already doing this with the appropriate sanctions approvals.

So although the US oil majors could come up with that investment, unless the US government guarantees those loans or investments, the oil industry is unlikely to be doing much on its own. And it will probably take 3 years to see the first fruits of that investment; Trump only has 3 years left in the top job.

What does it all mean for our portfolios?

Let’s be fair, Maduro’s Venezuela was unlikely to make it into our portfolios before Sunday, so no surprise that there is no direct impact. Also, we have no explicit Latin American exposure in our public markets portfolios, but we would expect it to be beneficial to the defence exposure we have in OGF, as the world again deals with the fact that defence spending is not a luxury item, it is a necessity. And I would expect to see the US oil majors perk up a bit, (notwithstanding the above economics etc), which is a theme we had already been looking at, but have not yet allocated to.

Generally, anything that makes the world a safer and more predictable place is good for our portfolios. The futures this morning are up, so we press onwards and upwards.

Upcoming trips and events:

Abu Dhabi/Dubai w/c 19th January, and

UK/Guernsey w/c 26th January

January is always a busy month, and we like to be out in front of our investors.

Our centrepiece event is in Abu Dhabi on Monday, 19th January. It is early evening event where we will bring together all our lead portfolio managers and investment committee members to present on the outlook for 2026. I am pleased to say we will be joined by Ramon Eyck (Opus Global Freedom and Managed Income), Cody Willard (US Technology VIP), and Justin Oliver (Opus Global Growth).

Invitations will be going out early this week. If you cannot make the event, don't worry, the team are in the UAE all week - and there will be plenty of opportunities for individual meetings.

We also have Cody Willard in London, Liverpool, Manchester and Guernsey in the week of 26th January as we introduce the strategy to our UK institutional client base. We are building the schedule as we speak, but we are planning a private client/family office lunch in London on Tuesday 27th and meetings and events in Guernsey around 29th/30th January. We will be reaching out shortly on these dates.

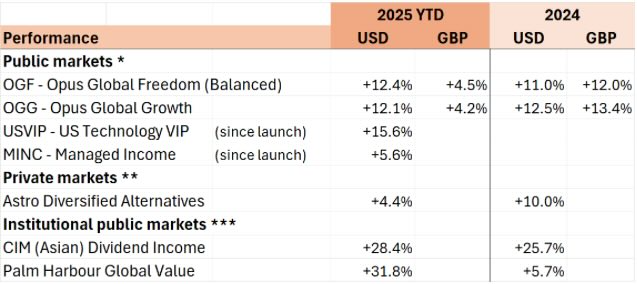

Performance

There was a little bit of horse trading in the last few days of the year. Tech and defence were a little bit off, and we saw a welcome late rally into the close for OGG.

Year-end performance is looking like this (remembering that the 4Q’25 Astro numbers are not expected in for another couple of months):

(See performance disclaimers at the foot this email).

We are happy with these numbers and we hope you are too. 2026 will doubtless be full of more surprises, but we start the year in a strong place, economically and geopolitically - and, at Freedom, a team of talented and passionate money managers eager for further success.

We thank you for your continued support and look forward to making you more money in 2026.

This week’s articles:

Derek Akkiprik on our investment team in Abu Dhabi reviews the opportunities in fixed income in 2026

- Cody Willard and the team at 10,000 Days have given us their “Tech Top 10 Predictions in 2026"

This week I am in the UK and Hong Kong. Wherever you are, let me wish you a wonderful and peaceful week ahead!

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

——————————

"Opportunities in Fixed Income in 2026”, 5/1/26

By Derek Akkiprik, Junior Investment Analyst

Rates for 2026: getting paid up front, staying careful on the long end

Fixed income heads into 2026 with something that was missing for years: meaningful income without taking heroic bets. The cleanest setup is still in U.S. Treasuries, especially in the front end (0–3 years) and the “belly” (3–7 years), where returns can come from simply holding bonds and collecting coupons.

Why this matters now

The Federal Reserve has already moved the policy rate down to 3.50%–3.75% and continues to stress that future moves depend on incoming data. Markets have tended to price a bit more easing than officials signal, which creates a reasonable base case: earn income first and treat any price rally as a bonus rather than the whole plan.

The curve

A bond’s total return can come from:

Income (coupon/interest)

Price moves (yields down → prices up)

“Roll-down”: as time passes, a bond “slides” toward shorter maturity, and if shorter yields are lower, the bond can naturally rise in price even if overall rates don’t move much

That’s why the front end and belly look attractive: they combine high starting yields with more reliable roll-down.

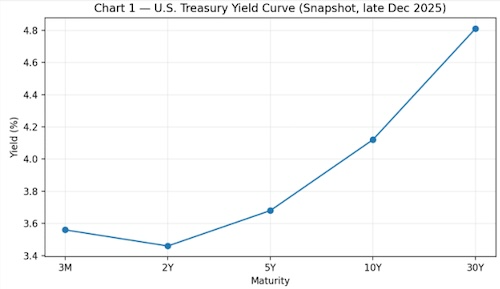

Where yields are starting (late Dec 2025):

3-month Treasury: ~3.64%

2-year Treasury: ~3.46%

That shape, short yields below the long end, supports the idea that intermediate maturities can “work” even without a big rate rally.

Why long duration needs a higher bar

Long bonds can still protect portfolios when growth collapses and investors rush to safety. But they also carry a different kind of risk going into 2026: (1) term premium and (2) fiscal concerns.

In simple terms, if investors demand more compensation for holding very long government debt (because of supply, deficits, or uncertainty), long yields can rise even in a world where the Fed is cutting. That means long duration is less of a “park it and forget it” trade and more of a tactical tool.

Inflation: TIPS as insurance, not a religion

Inflation is the swing factor that can ruin an otherwise clean “income-first” year. Market pricing looks relatively calm: the 5-year breakeven inflation rate is around ~2.25%. That’s not panic pricing—so TIPS are best framed as targeted insurance rather than a full portfolio pivot.

The key takeaway for 2026 is to build the core around front-end carry + belly roll-down, keep long duration selective, and use TIPS as a hedge when inflation risks start to reprice.

Derek Akkiprik

———————————

“Tech Top 10 Predictions in 2026”, 5/1/25

By 10,000 Days’ Cody Willard, Bryce Smith, Craig Delaune and Teguh Maulim

The team from 10,000 Days gave us each their Top 10 or Top 5 predictions - so in the interests of Brazilian rainforests I have edited this down to an overall "Tech Top 10”!

Perhaps the most important point to make in this article today is that none of these predictions, right or wrong, probably matter very much long-term, at least not in the context of Revolution Investing.

That is to say that if we're right about The AI, Robotics and Space Revolutions creating more wealth in the next 25 years than was created in all of humankind existence then it won't matter in ten years whether or not 10-year Treasury interest rates end 2026 at 2% or 4.5%, or whether or not Republicans or Democrats win the next election or even whether or not Nvidia is under-owned right now. If we're right, the global and galactic economies will create tens of trillions of dollars of new wealth for Revolution Investors over the next decade at an ever-accelerating pace.

Top 10 Tech Predictions

1// (Cody) The biggest, most valuable tech companies on the planet become even bigger and more valuable in 2026, increasing their share of the economy and their share of the stock market. We've basically got a dozen or so near monopolistic tech companies that are positioned to become near monopolistic AI and Robotics companies in the years ahead. The fundamental growth at these companies will continue to outpace most of the other 488 companies in the S&P 500 and pundits will complain even louder about what a big percentage of the stock market these companies account for.

2// (Bryce) We see the first 100,000 humanoid robots enter commercial use. Most will be in factories (probably the vast majority of the 100k are Tesla Optimi working in Tesla factories).

Sub-predictions:

The first humanoid robotics pure-play company comes public (most likely Unitree in China or Figure.AI in the US) at a $50+ billion valuation

We see the first robot-only bar or restaurant (still humans in the loop, but most of the customer-facing roles will be held by humanoids)

3// (Bryce) Augmented Reality/Virtual Reality (AR/VR) stages a massive comeback as AI integrations make personal devices like AI Glasses incredibly more useful and consumer-friendly.

Sub-predictions:

Meta crosses 15 million cumulative pairs of AI glasses shipped, and launches two new versions of its Display AR glasses. Meta also launches the Meta App Store for AI glasses.

A new AR/VR video game or social media app goes viral late in the year and hits 10 million monthly active users before Christmas.

Qualcomm hits $250 per share as the company raises 2027 guidance on the back of extremely strong demand for AR/VR devices (bonus prediction: Apple and Qualcomm announce a 2-year extension of their partnership (currently set to expire in 2027).

4// (Craig) 2026 is where OpenAI finally puts the revenue argument to bed, and it does that through OpenAI giving the people the chat bot they want. Next year, the AI companion will be redefined with ChatGPT 6.0, resulting in an ever-present assistant with improved speech recognition, more nuanced conversational abilities, and memory that persists across time and modalities. The lines between human and AI interaction will begin to blur as we grow more comfortable with its presence in our day to day lives. As that comfort grows, I think we see a push toward advertising in ChatGPT - akin to letting off the clutch and pressing on the gas. With the goal of going public, OpenAI will project advertising revenue, which will be met with a collective sigh of relief from bulls, followed by an extremely high stock price that further reinforces its already extraordinary valuation.

5// (Craig) Demand for compute doesn't ease up, in part because of The Robotics Revolution. Spacial AI will be all the rage next year as robotics companies compete to be the first to have a commercially viable, fully AI driven humanoid out by early 2027. Spacial AI won't just be used to train the robots, but their "brains" will be able to predict consequences of movement by running thousands of mini simulations before taking any action. For example, think of a kid in Minnesota hesitating before skating on a frozen lake in March after hearing the ice crack beneath his feet. A robot will do something similar, visually assessing the ice, factoring in temperature and thickness, and simulating what happens if it steps forward. This is the robotic equivalent of how humans feel risk before jumping a ditch or climbing a tree. The Robotics Revolution will drive an unprecedented volume of computation, sustaining demand for compute through the end of the decade and accelerating innovation in the data center space.

6// (Teguh) Policy, Ethics, and Regulatory Focus Intensifies. As AI becomes more pervasive, governments and organizations will increasingly address copyright, misinformation, deepfakes, and other ethical concerns. Policy discussions and regulatory frameworks will play a critical role in shaping how AI is deployed responsibly across industries.

7// (Cody) Optical networking becomes the most hyped part of The AI Revolution. Fiber optic connections between memory and inference chips are more economically and energy efficient than trying to jam endlessly more high end memory chips on each AI chip. Nvidia and Google (GOOG) and others will benefit from this trend over time and we are hard at work finding pureplays set to benefit from this new trend.

8// (Cody) The dollar has a strong year in 2026 on the back of US GDP growth and productivity gains which helps feed into the stablecoin virtuous cycle for the US dollar and the USDC. This is one of the reasons we own Circle (CRCL).

9// (Cody) Space stocks peak a month before the SpaceX IPO and spend the next two years in a bear market. SpaceX will be fine.

10// (Bryce) Starlink voice service (direct-to-cell (DTC)) becomes generally available to U.S. customers, putting pressure on the Big 3 U.S. telecom providers (note that texting is already available via the SpaceX/T-Mobile partnership).

Sub-predictions:

The Big 3 (AT&T, Verizon, and T-Mobile) subsidize the Starlink DTC service to prevent subscribers from leaving their network

SpaceX has at least 10 million DTC subscribers by the end of the year

And there we have it, the Tech Top 10 predictions from our very able Revolutionary Tech team at 10,000 Days.

Cody Willard, Bryce Smith

——————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 31/12/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 31/12/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2026 Freedom Asset Management Limited.