.jpg)

Weekly Newsletter

Freedom Calls: 29/12/25, 2026 Predictions, defence and how AI will blow our minds in 2026

by

The team at Freedom Asset Management

December 29, 2025

12 Minutes

Freedom Calls: 29/12/25, “2026 Predictions, defence and how AI will blow our minds in 2026”

From the team at Freedom Asset Management

I hope your Christmas break was a bit warmer than mine, as I unexpectedly (and not entirely voluntarily) retrained as a heating engineer. It seems that at this time of year my own heating engineer prefers Barbados to the wintery chills of Guernsey - and quite right too, I may join him next year! Armed only with a collection of non-English language Youtube videos, internet pages and some (at best) curious (and often competing) logic, I managed to restart the highly sophisticated nuclear power station in our garage, which masquerades as the heating and hot water supply. It then took a full 24 hours to bring it all back on line to have a cosy, warm house.

And all because… two AA batteries in one of the thermostats had died…. It is a beautiful example for business of how we are only as good as the weakest link in our chain.

Reflecting on 2025

With 3 trading days left in the year and many people in the Western world sizing up the most imaginative way to work with turkey leftovers, it is customary to reflect on 2025.

At Freedom, 2025 was a busy year, organisationally:

Our Abu Dhabi (ADGM) business became a stand-alone FSRA licensed entity, as we closed down the ADGM branch of our Guernsey business that had been in place since 2019;

ADGM has now become Freedom's biggest office and we continue to expand from ADGM

We launched 2 new funds in Abu Dhabi - our US Technology VIP fund and our Managed Income fund - each fund supported by Mubadala Capital’s Abu Dhabi Catalyst Partners

Our new Hong Kong SFC regulated business launched its first domestic (OFC) fund using our Qualified Foreign Institutional Investor (QFII) license to access hedge fund managers in China. As we go to press, we are putting the finishing touches to our second fund, which is due to launch in February/March 2026 and there is a strong institutional pipeline for that business.

Investment markets certainly kept us busy in 2025

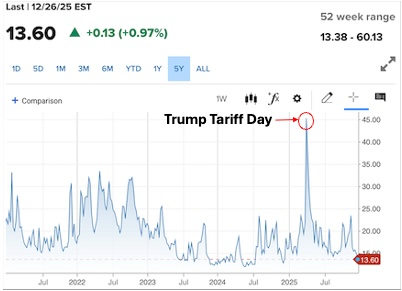

As we munch on our mince pies, it is easy to forget that in April we saw the largest spike in volatility for 5 years, when Trump announced his initial tariff plans (see chart below). Large spikes in volatility, affectionately known as “vol” in the trade, almost always come with massive drawdowns at little, or no notice.

It now seems a distant memory, but this level of vol was higher than the outbreak of the war in Ukraine (February 2022) and right up there with Covid (March 2020). Many panicked…. journalists told us that world as we knew it was about to end, and private banks made margin calls on their clients. We sat tight and played this out. When you don’t have leverage, you can afford to play the long game.

Source: CNBC, 26/12/25, CBOE Volatility Index (.VIX)

As we look at how the year is ending for our funds, across the piece, that was undoubtedly the right decision...

(See performance disclaimers at the foot of this email)

So what does 2026 hold?

In the world of predictable financial market outcomes, there are really only two data points that matter for 2026:

Will the Federal Reserve cut interest rates again and when?

Will the US enter a recession in 2026?, and

(The Bonus Question) Who will Trump nominate as Fed Chair?

So this year, I thought I would try something different. Polymarket is the go to prediction website for all manner of questions, from politics, economics to sport and a lot more beyond. In some countries you may require a VPN to access the site.

For people like us, who like to keep track of data points, it is a real time check on what the “market" is thinking, because you can watch how the percentage outcomes change by the hour. The people who make the percentages real are those who are placing money on those particular outcomes. Polymarket has a remarkably good track record at predicting the right outcomes, certainly better than government departments.

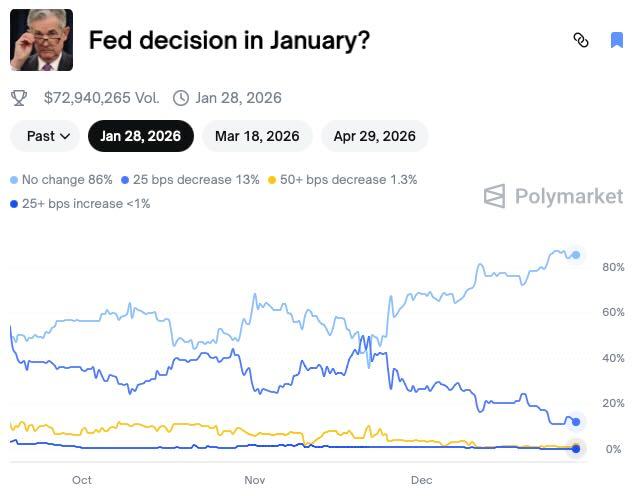

So we looked at Polymarket to see what it is thinking about our key economic questions:

You can see from the above chart that there is an 86% chance of "no change" in interest rates at the January Fed meeting. Bloomberg cannot poll analysts as quickly or as convincingly as this. The equivalent chart for March says 64% no change, and then for April 62% for no change. So we will probably have to wait until April/May before we see the next rate cut.

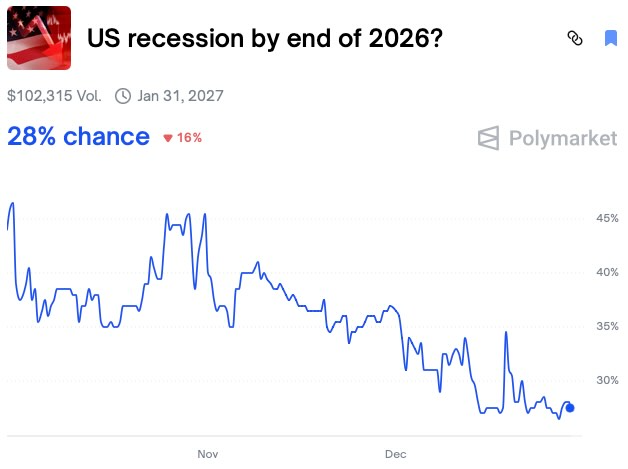

So here, in the last two months the risk of a recession in the US in 2026 has dropped from 45% to 28%. This suggests we have a fairly confident route ahead for investors in US stock markets in 2026.

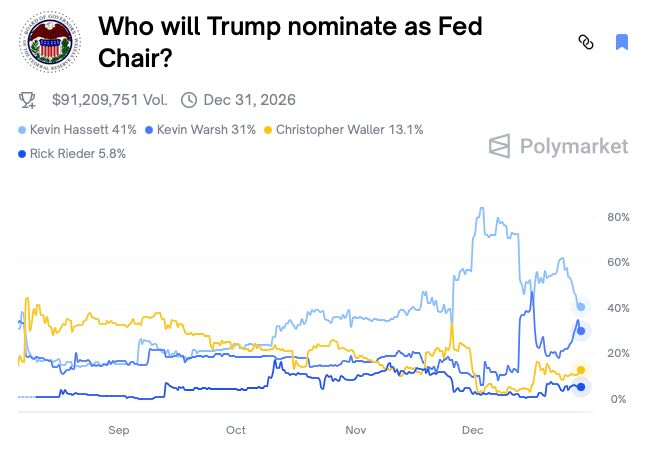

Moving to our bonus question, "who will Trump nominate as the Fed Chair?”, I think we can be fairly certain he is going to be called Kevin(!) The next Fed Chair takes up the role in May 2026, so is expected to have a big influence on how the rest of the year plays out for interest rates.

Kevin Hassett (on 41%) is seen as a Trump loyalist, who will seek to lower rates perhaps more aggressively than the rest of the board. Kevin Warsh (on 31%), who has previously served as a Fed governor (so has more experience), comes from a more “hawkish” background, i.e. he has historically favoured tightening monetary policy with higher interest rates. However, Trump is on record as saying that they would both like to lower interest rates.

In reality, they are both going to be in favour of cutting rates, the only question is when and how much.

When it comes to geopolitical positioning, Polymarket is less useful.

Geopolitics

I would say these are some of the main geopolitical thoughts for 2026:

1// We are in a US and China world - not much else matters

One of the most depressing realities when you spend a lot of time in Asia is that Europe simply does not matter. It used to, but it really doesn’t now. President Xi only cares about the US. Russia is a slightly embarrassing ally and moderately useful trade partner to China, but nothing matters more than the US. President Trump has worked this out.

2// Sorting out Ukraine - does Putin really want peace and what is the peace dividend?

We talk to lots of people on this all of the time. There has been much movement (and talk) towards peace, but the considered view at the moment is that Putin is playing for time. He believes if he stays in the fight for longer, Ukraine will run out of men and resources and he will prevail. Given the changing nature of battlefield warfare (i.e. the extensive use of drones), the statistics are not looking good for Putin’s chances of achieving the outcome he seeks.

The counter narrative on Russia is that it is spending massively and has dipped heavily into its domestic sovereign wealth fund to fund its war machine. At this rate, apparently, the tap runs dry in 18 months. Russia is already looking at increases on income taxes to help fix the gap.

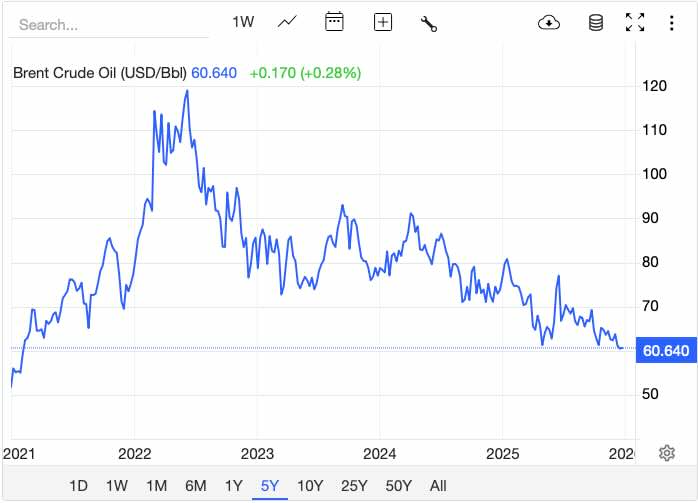

During WWII there was a secret effort by the Allies to prop up the price of commodities to make it harder for Hilter to stay in the war. You have to slightly ask yourself the question about whether the current oil glut (in the middle of Europe's and North America's winter) has been created to weaken Russia’s position. I can believe that Trump has done a deal with the Saudis (in return for military support) to make sure the pumps keep pumping - see the price of Brent crude below at the lowest point in 5 years. This serves Trump’s needs in Russia, but also keeps Venezuela and Iran in check. It is not great for the US oil industry however.

(Source: 5 year chart on Brent Oil price, Tradingeconomics.com 28/12/25)

As we go to press, there are talks at Mar-a-Largo with Trump and Zelensky. We sincerely hope these talks lead to a lasting peace.

We have been looking at how to play the Ukrainian rebuilding story when it happens. The Ukrainian stock market was an unhappy place long before the war. There are only 2 stocks that make up the MSCI Ukraine Index - one is a chicken producer (MHP - a GDR) and the other is a telecoms operator (VEON - an ADR).

So we expect the most likely beneficiaries will be Polish companies from their close geographic proximity - from the banks to the consumer stocks and the builders. The Polish stock exchange is a much broader and deeper market - so we will be researching this more.

3// What is happening in Venezuela - and does it matter?

When the Nobel organization awarded its 2025 Peace Prize to the (at least internationally) little known Venezuelan opposition politician María Corina Machado, (instead of the mighty Mr Trump), they probably thought that nobody would give a second thought by teatime.

But upon receiving the said award, the very same Venezuelan politician asked for Trump’s help against the current incumbent President Maduro. She and the Norwegians were probably not expecting 15,000 troops and the US Navy’s Fourth Fleet to be deployed off Venezuela’s coast.

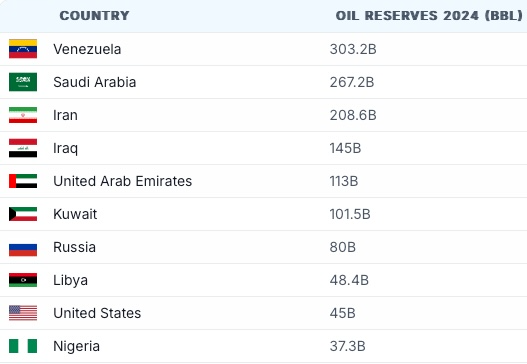

Although Venezuela has been heavily sanctioned by the US and is now only producing c.1m barrels of oil a day, it holds the world’s largest proven oil reserves at 303bn barrels - see chart below, so to the Western world, Venezuela does matter, especially if it is being run by the “wrong” people, with the “wrong" friends:

Source: www.worldpopulationreview.com

The working assumption on Trump is that he intends to depose Maduro and welcome in the opposition candidates. He would then like to see the return of US oil companies to Venezuela. It is all strategic, just not terribly peaceful.

4// China and Taiwan

We think this is not the year that China makes the long reach for Taiwan, but make no mistake President Xi would like to see this during his political lifetime. Just not this year. Read Charles’ article below for an update on readiness for that scenario.

Our articles this week:

Bryce Smith of 10,000 Days, Advisers to the US Technology VIP fund, write about how AI could blow our minds in 2026

Charles Harris, Investment Analyst in our Abu Dhabi office gives us an update on Global Defence positioning

This week I am in Guernsey and London. Wherever you are spending the New Year’s holiday, please let me wish you a wonderful week ahead! And top tip - stock up on some AA batteries!!

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

—————————

“Could AI blow our minds in 2026? Our answer is an emphatic “Yes,” Here’s why.", 29/12/25

By 10,000 Days’ Cody Willard and Bryce Smith, Adviser to the US Technology VIP Fund

We are slightly more than three years into The AI Revolution–starting with the ChatGPT moment–and we feel like sentiment toward the “AI trade” has shifted to something closer to apathy rather than exuberance.

I think a lot of people on Wall Street are simply tired of talking about AI and the endless debate and volatility surrounding AI is exhausting. This year has seen a lot of whipsaw action in tech resulting from debates around DeepSeek, circular financing, Oracle’s debt, depreciation schedules, Michael Burry, OpenAI drama, the list goes on.

Those volatility spikes were probably enough to wipe out many of the people riding the AI hype wave. The fact that AI is still accelerating ahead is a testament to AI’s legitimacy and durability. And in 2026, there is a real chance that AI will become so good that the debates we’ve seen this year about the fundamental technology and business models of the companies building AI become asinine.

First, we think that AI models trained on Nvidia’s latest Blackwell architecture will result in a step change in performance and capabilities. All of today’s AI models were trained on Nvidia’s last-gen hardware, and the AI companies are just now training models on Blackwell. These next-gen chips have 5x the raw throughput of Hopper (the last generation) with more than 2x the bandwidth capabilities. So that’s going to result in large language models (LLMs) and other AI models that have at least 10x the number of parameters (which are essentially a unit of knowledge, like a neuron in a brain) of prior models.

Moreover, these racks are being connected in data centers that are themselves an order of magnitude larger than the last generation. The first gigawatt-scale data centers are coming online in early 2026, and these will be 10-20x larger than the single largest data centers currently in operation.

So we are looking at the chips/racks themselves becoming 10x more powerful, and those chips are connected in data centers that are 10x-20x larger. While that’s absolutely incredible, AI follows a power law, meaning 100x more compute does not result in a model that is necessarily 100x "smarter." But the models will certainly get a lot smarter, and these hardware improvements will also unlock more-advanced reasoning—allowing models to think, plan, and self-correct during inference rather than just predicting the next word—and to process massive context windows of data.

In other words, the AI’s depth of capability will be orders of magnitude deeper and it will hold vastly more information in memory to solve complex, multi-step problems that today’s models cannot. In short, the AI of 2026 will make today’s AI look like child's play.

If AI capabilities improve to the degree we expect, we think it will put to rest most of the debates about the value of the tech itself and whether these AI companies are crazy for spending hundreds of billions on AI data centers. The AI of 2026 will be so good that its impact on revenue, earnings, and growth will be impossible to ignore.

Further, enterprises, governments, startups, and individuals are all figuring out how to implement AI in ways that drive further productivity/entertainment gains. There is always a lag between tech development and tech adoption, and there is a good chance that we see adoption of AI skyrocket in 2026. Especially as the models become orders of magnitude more capable, companies and governments will fall behind rapidly if they do not furiously focus on implementing AI across their organizations.

In sum, we think AI will become extremely more capable, extremely more useful, and incredibly more entertaining in 2026. As the current debates around AI start to fade into the rear-view mirror, new debates will certainly emerge. However, as long as the core technology keeps improving (as we expect) and the major AI companies continue to grow revenue and earnings (as we expect), the music will go on.

As we go into the new year, we know from past experiences that we must remain realistic about tech Revolutions like this. Which, come to think of it, is why we are so incredibly excited about the future and the wealth it’s going to create. I often say that the biggest mistake in my career has been not fully believing how big these Revolutions can get and how much wealth they can create. So let’s remain realistic about The AI Revolution in 2026!

Bryce Smith

——————————

"Defence Outlook Part 1: Geopolitics”, 29/12/25

By Charles Harris

Geopolitics, Advanced Tech, and Industrial Supply Chains form the triad underpinning the defence sector's trajectory in 2026. We will discuss Advanced Tech and Industrial Supply Chains in the coming weeks, but this week we discuss the how geopolitics factors will likely shape the defence industry in 2026.

We will discuss firstly some of the ways in which European states have reacted to the invasion of Ukraine and secondly touch on how tensions in the Indo-Pacific are shaping defence spending in south-east Asia.

Following the 2022 invasion of Ukraine, which ended years of underinvestment (aka ‘the peace dividend’), NATO allies massively boosted defence spending. By 2025, all allies are expected to meet the 2% GDP target, which was initially set over a decade ago and in a summit in June NATO members agreed to push this goal to 5% - of which 3.5% is earmarked specifically for core defence capabilities.

Heading into 2026, there are currently no signs of a slowdown in defence procurement or development, but with peace negotiations being held between Trump and Zelensky/Putin and truces between the Trump and Xi some question the long-term inevitability of the defence sector. Below are only a few of the key initiatives that will continue to unfold over the coming years.

European Reinvestment

In Europe, the focus has shifted from political pledges to that of deterrence.

1. The European Space Shield

The most significant milestone of 2026 is the formal launch of the European Space Shield in the second quarter. Distinct from the air-domain European Sky Shield Initiative (ESSI), this project is designed to protect critical EU space assets – e.g. the Galileo navigation system and Copernicus satellites - from kinetic destruction, jamming, and spoofing. This initiative marks the EU's transition from a regulatory power to a hard security actor in space, responding directly to the weaponization of orbit unfriendly states.

This offers a unique opportunity for European based space or space related companies as there is an immediate demand for hardware in a sector currently dominated by the US (majority SpaceX), China and Russia. European defence companies with space divisions will likely be the largest beneficiaries e.g. BAE Systems, Thales, Leonardo SpA and Avio SpA etc.

2. Brigade Litauen

Simultaneously, on NATO's eastern flank, Germany's newly established Brigade Litauen (45th Armoured Brigade) will be permanently stationed in Lithuania. By mid-2026, the brigade will reach a strength of approximately 2,000 troops, integrating the existing rotational Enhanced Forward Presence into a national command structure. This "tripwire" force fundamentally alters the calculus for aggression against the Baltic states.

This deployment should drive a surge in infrastructure and logistics contracts. Beyond construction, industry must establish forward-deployed MRO (Maintenance, Repair, and Overhaul) hubs to sustain Leopard 2 tanks and Puma IFVs on the frontier. Landsystem providers will likely be the largest beneficiaries e.g. Rheinmetall, KDNS, BAE Systems, Leonardo SpA etc.

The Indo-Pacific: Closing the "Davidson Window"

In Asia, 2026 is viewed as the final year of preparation before the onset of the "Davidson Window" (2027) - the period between 2021-2027 when the People’s Liberation Army (PLA) is assessed to be capable of seizing Taiwan, stemming from US Admiral Davidson’s warning to the senate in 2021.

1. Japan SHIELD

Japan’s defence budget for FY 2026 is set to reach a record Yen 9 trillion yen (approx. $58 billion), solidifying its shift from a strictly defensive posture. A centrepiece of this is the SHIELD (Synchronized, Hybrid, Integrated and Enhanced Littoral Defence) network.

Utilizing unmanned aerial, surface, and underwater vehicles, SHIELD aims to deny access to the First Island Chain which extend from the Kuril Islands, the Japanese archipelago, the Ryukyu Islands and then down to Taiwan (Formosa) before reaching the northern Philippines and Borneo.

Japan presents an urgent demand for expendable drones producible in the thousands. This opens the market to non-traditional tech companies and startups capable of delivering AI-enabled systems rapidly.

2. AUKUS Integration

The AUKUS partnership moves to high-tempo experimentation in 2026 with the "Maritime Big Play" exercises, integrating autonomous systems across the US, UK, and Australia. This precedes the 2027 rotational deployment of Virginia-class and Astute-class submarines from Western Australia.

The geopolitical necessity of AUKUS is breaking down historic barriers in technology transfer. The industry is seeing a push for interchangeable software architectures e.g. allowing a US sea drone to communicate with a British submarine. For the industrial base, the competitive advantage is shifting to "software-defined warfare," prioritizing AI integration and data processing speeds over traditional hull strength.

As we enter 2026, geopolitics has established itself as the primary architect of the global industrial landscape. The threats looming over Europe and the Indo-Pacific have shed their abstract nature, evolving into concrete operational challenges that demands immediate action.

This newfound urgency is reshaping the defence sector's mandate. The industry is no longer just delivering contracts; it is racing to accelerate production timelines and localize supply chains directly to the point of use, from the forests of Lithuania to the coastlines of Japan. In this new era, the priority is clear: deliver systems that offer immediate, scalable deterrence.

Charles Harris

————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 28/12/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 28/12/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.