.jpg)

Weekly Newsletter

Freedom Calls: 2/2/26, "Hey Meta…. what happened to Silver last week?…. And the Tesla financial model for robotaxis explained"

by

The team at Freedom Asset Management

February 2, 2026

12 minutes

Freedom Calls: 2/2/26, "Hey Meta…. what happened to Silver last week?…. And the Tesla financial model for robotaxis explained"

From the team at Freedom Asset Management

We had Cody Willard in London and briefly Guernsey last week on his way back from Abu Dhabi. Without doubt the "best supporting actor role" of the trip went to a pair of Ray-Ban Meta Display glasses (pictured below). Still not yet available in the UK and Europe, the latest generation of these glasses have a very cool display inside the glasses only visible to the wearer. You can ask the glasses a question by starting all prompts with "Hey Meta…".

You need to have installed the Meta AI app on your iPhone to make it all work and be in close proximity to your phone, whilst it seeks out the answers to your questions - anything from "what am I looking at?" to "what is the weather today?". It takes photos and videos with a simple audio prompt and connects to your Spotify playlist with excellent audio. The sound is carried through small speakers in the arms near the ears, which therefore allows the user to be completely aware of their surroundings. Unless you were in a very quiet room you would not know that the Meta glasses wearer was listening to anything.

What is particularly clever about these glasses is that they weigh only a little more than a set of reading glasses, have a 5-hour battery life, and recharge in the case (see above) which itself carries a 30-hour battery life.

It is not every day that we see a new technology which will change human behaviour, but this one will!

A new Fed Chair announced

Well so much for Polymarket telling us that BlackRock's Rick Rieder was going to be the next Fed chair…. it was a Kevin after all! So what does it mean for markets? Kevin Warsh is styled as somewhat of a hawk, i.e. he favours a smaller balance sheet for the Fed, but he has indicated that he favours some interest rate cuts. He has previously been on the Fed board of governors, so he should not be too much of a contentious choice.

Potentially unwinding the Fed balance sheet could point to higher long-term interest rates. At one stage the Fed owned $9tr of US government debt, which had the effect, as we now know, of distorting pretty much all asset prices. So, a Central Bank that goes back to being a Central Bank is probably no bad thing in the long term even if there is some adjustment in the meantime.

So what happened to Silver last week?

The 1-month daily closing price chart on Silver below shows how it peaked at $115.50 last week before plummeting c.32% to $78.53. I was always taught that Silver is a speculators asset, whereas Gold has an investment case. And despite the new narrative about Silver being a key component in the solar energy industry (which it is) and in electronic and technology (which it is), that has not stopped Silver being used to highly speculative effect. Whilst Silver is still up on the month, an asset that can deviate so wildly from its fundamentals over a 2-week period is not something we are likely to want to own as a single portfolio line item - and in consequence we didn't.

Silver price - last month

Source: CNBC, 1/2/26 Silver COMEX (Mar 26), using closing prices

In contrast, Gold whilst also having a roller coaster month, is only down c.12% from its peak (and still up on the month). The case for Gold is much more investment based - i.e. the weakening dollar trade, and the "tricky Central Bank stockpiling trade". The Central Banks of China, Iran and Russia are known to be accumulating significant quantities of physical Gold in place of US Treasuries, and seem to be price insensitive, because of geopolitical reasons. So, as investors know, we do hold Gold exposure in our funds and have benefited so far this month.

Gold price - last month

Source: CNBC, 1/2/26 Gold COMEX (Feb 26), using closing prices

Performance

There was a bit of repricing in technology stocks last week, erasing almost all the gains for January, but that is obviously quite helpful for those considering an investment or top-up in our US Technology VIP fund (USVIP). If you are coming from Sterling even better as cable still wants to trade close to $1.37.

The rest of the funds are all printing solid year to date numbers. It is early days, but we always like to see a positive start to the year.

(Please see performance disclaimers at the foot of this email.)

Our articles this week:

10,000 Days' Cody Willard and Bryce Smith (USVIP) model out the case for Tesla with robotaxis in "Tesla enters a new era"

Canaccord's Justin Oliver (OGG) reports on India reaching an important economic milestone, in "India is about to overtake Japan as Asia's No. 2 economy”

Iran is the arena to watch this week

We are conscious that the US is building up its warship presence in the Gulf and we have heard sources suggesting that Trump will make his move on Iran this week. Whatever that move, if it happens, is likely to be swift and hit at the regime's military and nuclear capability. We should expect the move to be supported by Israeli military assets.

If an attack does happen, it is unlikely to match the move on Maduro in Venezuela - you cannot simply remove one person from the Iranian regime and take effective "control" of the country. Maduro was, simplistically, a corrupt man running a corrupt system - and you can always put a new (less corrupt and more aligned) person in his place. The Iranian problem is intertwined with religion and religious fundamentalism - and the last thing Trump will want to do is lend any credibility to setting off a new series of religious wars against the US and its allies in the region.

Another possibility is that Trump uses the warships in the Gulf to block access for Iranian crude in the Strait of Hormuz (see below). A naval blockade was how things started in Venezuela. This would effectively put a stranglehold on the Iranian economy, but it will take longer to achieve the desired result. At its narrowest point there is only a 6 mile wide navigable route for large tankers, so not difficult to implement a naval blockade.

Source: Wikipedia

Whatever the chosen method, we should be prepared for some volatility in the immediate aftermath. But as we have said in previous notes, anything that Trump does to make the world fundamentally a safer and more predictable place will quickly become good for the investments we hold in the funds.

I will be spending this week in the Swiss Alps, but staying very much in touch with developments and the team; I look forward to being back in Abu Dhabi from 9th February.

Let me wish you a wonderful and peaceful week ahead.

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

——————————————

"Tesla enters a new era", 2/2/26

By 10,000 Days' Cody Willard and Bryce Smith - Advisers to US Technology VIP Fund

2026 is shaping up to be the year when AI comes to the “real world.” We are speaking mostly of Tesla, and we think the company has laid the groundwork to shock the world in 2026. If I could sum up the Tesla quarter in two words, they would be “game on.”

We were more excited listening to this Tesla quarter than maybe any other quarter in the last four years or so. It’s clear that all of the things that Tesla has been working on for years are coming together and 2026 is the year they start to scale several incredible new businesses.

Among other exciting updates, Tesla disclosed the total number of full self-driving (FSD) subscriptions at 1.1 million, growing 38% y/y. Moreover, the company is discontinuing the Models S and X to replace those factory lines with Optimus production lines capable of producing 1 million robots per year. They are also doubling their AI compute capacity, scaling cybercabs, scaling semi, and more.

And in just four short months with a tiny fleet of robotaxis (about 500 as of the end of the year) in two cities, the company reported 650,000 cumulative paid robotaxi miles, and the curve is growing exponentially. Tesla plans to expand the robotaxi service to seven more cities in the first half of 2026.

However, almost nobody on Wall Street has modeled what Tesla’s financials will look like if they scale robotaxis in 2026 as they are currently planning. So we did the math, and the math shows that Elon was no dummy for putting all of his eggs in the "autonomy" basket for so long:

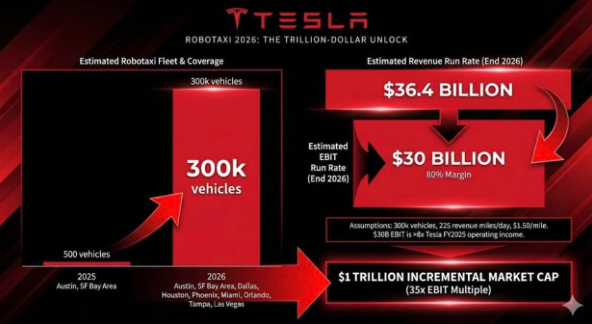

In sum, we think robotaxi is, in and of itself, a $1 trillion unlock for Tesla in 2026 alone, even at a small scale compared to its ultimate potential. According to our numbers, the robotaxi business could be at a $36 billion revenue run rate by the end of the year (which would amount to 38% of Tesla’s 2025 revenue) and produce $30 billion in earnings before interest and taxes (EBIT), or more than 8x Tesla’s entire operating income in 2025. If we put a 35 multiple on those earnings, that’s $1 trillion in incremental market cap for Tesla (for context, Tesla currently trades at about 300x its TTM EBIT).

Our model assumes that Tesla has about 300k robotaxis in nine cities in operation by the end of the year. That may sound like a tall order, but it’s actually quite reasonable. The nine cities Tesla is focusing on at present have about ~300k rideshare drivers currently, and all nine of them have existing robotaxi operations or test programs (mostly Waymo), so regulation shouldn’t be too much of a hurdle.

So you might ask, how can Tesla possibly replace every Uber, Lyft, and Waymo in these cities? It’s pretty simple: cost. Tesla robotaxi can undercut its competition by 50% or more and still generate 80% EBIT margins for the company according to our model. Rideshare is basically a pure commodity, and Tesla will be cheaper than any other option on the road. Moreover, Tesla is fundamentally safer than human drivers (the data shows they are already about 10x safer than a human), and there is no risk of assault or theft from the driver, and no chance you hop in a stinky cab with a guy harassing you about politics.

Moreover, 300k robotaxis wouldn’t be much for Tesla in terms of its existing supply chain as they already produce about 2 million vehicles per year, and their documents indicate that they have capacity to produce 2.35 million vehicles. The company is also building dedicated cybercab production lines in Austin, Texas, and those are expected to enter production in the first half of the year.

Now, let’s talk about unit economics (which are amazing).

We estimate that an individual robotaxi will generate about 225 revenue miles per day (that’s conservatively estimated as 11.25 revenue miles for 20 hours per day (we’re assuming 4 hours per day of charging, cleaning, etc.)). At $1.5 revenue per mile (half price of most Ubers), that car will generate about $121,500 in revenue per year. Cash operating costs (electricity, tires, insurance (Tesla will self-insure)) amount to roughly $0.20 per mile, which equates to $16,200 per year. If the car costs Tesla $35,000 to make (I think it will be lower than that at scale), and lasts five years, that’s $7,000 per year in depreciation. This model indicates that the robotaxis will generate a return on invested capital (ROIC) of 280%, or a 4 month payback period. I like those kinds of numbers.

The reason this is so exciting right now is because the path ahead is clear, and the groundwork has been laid for this to actually happen this year. Elon has his pay package, which is specifically tied to robotaxi production (1 million in service), the company is testing and preparing to scale cybercabs, there are no more safety monitors in Austin, and the cities they are targeting all have existing autonomous vehicle operations and regulatory frameworks, significantly lowering the barriers to scaling.

And don’t forget, robotaxi is just one of Tesla’s exciting business lines. The company will also be scaling semis, batteries, solar panels, and most importantly, Optimus Robots this year. Moreover, the $1 trillion unlock for robotaxis is just for 2026, and assumes operations in just a few American cities. This will be a business that the market will value in the tens of trillions of dollars once it scales across the US and the rest of the world. Just think of the latent demand Tesla will unlock when the cost of transportation is 50-60% lower than current prices?

Of course, there are risks, and we don’t want to make it sound like scaling this business will be easy. These vehicles must continue to operate safely, and Tesla will need to expand its physical footprint to support hundreds of thousands of cars hauling people from place to place in nine major cities. It won’t be a walk in the park, but the payoff will be enormous if they pull it off.

In conclusion, it really feels like Tesla is entering a new era, and the company is 100% on the autonomy, AI, and robotics paths. It’s now or never. Tesla sunsetting their original Model S and X vehicles to make room for Optimus production lines at their Freemont, CA factory is symbolic of where the company is at in its lifecycle. If there was ever a question of whether Tesla was an EV company or an AI company, that is a question no more. What we are witnessing is the formal transition from EVs to a platform for physical AI, and it is extremely exciting. Rock on!

Cody Willard and Bryce Smith

———————————

"India is about to overtake Japan as Asia's No. 2 economy”, 2/2/26

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

As investors fret about US tariffs, Chinese deflation, Japanese yen volatility, and geopolitical upheaval, India continues to shine. Its 8.4% year-on-year (y/y) growth rate and relatively calm economic backdrop offer a contrast to many of today’s concerns.

Indeed, India is on the verge of passing a tantalizing milestone: surpassing Japan in GDP terms to become Asia’s No. 2 economy. Prime Minister Narendra Modi’s government claims that India had $4.18 trillion of output in 2025. That exceeds the World Bank’s calculation of Japan’s GDP, at $4.03 trillion, and is nearly as high as the International Monetary Fund’s $4.2 trillion calculation. Next target: Germany within three years.

Impressively, India is holding its ground in the face of 50% US tariffs. Clinching the “mother of all deals” with the European Union last week should help to build on what Modi’s Bharatiya Janata Party calls a “Goldilocks moment,” with rapid growth and moderate inflation. India projects 7.4% GDP growth over the next fiscal year. And inflation rose just 1.3% y/y in December, roughly half the rates that confront the central banks in the US and Japan. The EU trade deal, 20 years in the making, will eliminate or reduce tariffs on 99.5% of goods from India over seven years.

President Donald Trump’s inner circle probably never expected Modi’s party to regard 2025 as a “defining year for India’s growth” despite the US tariffs. Nor did they expect the tariffs to be the catalyst, jumpstarting Modi’s long-stalled efforts to increase government efficiency and move the economy upmarket. Reforms fast-tracked to help India weather the trade war include: overhauling labour codes, cutting consumption taxes, opening insurance companies to full foreign ownership, pulling forward capital spending on infrastructure, giving private companies access to the nuclear industry, unifying India’s securities laws into one single code, and pivoting to new markets.

Trump’s trade war is also catalysing a detente between India and China. Clashes over a 2020 border skirmish in the Himalayas are becoming an afterthought as New Delhi and Beijing lower their economic guards. By year-end 2025, Indian shipments to China were almost 70% higher than a year earlier. One particularly wise policy shift was a change to visa policies to allow in Chinese workers, needed to build Indian factories. It’s a recognition that, for all India’s success in luring Apple, Intel, Samsung, and Taiwan’s Powerchip Semiconductor Manufacturing Corp., achieving Modi’s “Semiconductor Mission” requires Chinese machinery and expertise.

That said, it’s not all plain sailing. The cumulative effects of Trump’s 50% import tax could erode GDP growth in the months ahead. As South Korea found out this week, Trump isn’t done hitting Asia with tariffs. The White House says it will raise its Korean imports levy to 25% from 15%. Could Modi’s EU trade pact draw fresh US retaliation? Other possible headwinds for India include prospects for a further economic slowdown in China, supply-chain chaos, deeper disinflation, and Modi’s falling short of key pledges he has yet to fulfil. These include the “Make in India” plan to morph the nation into a top manufacturing power to address high youth unemployment.

Though India can boast of isolated successes in manufacturing - including wooing Airbus, Amazon, Microsoft, and Nissan - manufacturing’s share of GDP is now 17% at best, a long way from the 25% envisioned back in 2014. Modi has a penchant for announcing high-profile foreign investments, then pivoting back to national security pursuits. He’s been slow to cut red tape, increase transparency, level playing fields, strengthen human capital, and raise productivity. This explains India’s multi-speed economy 140 months into the Modi era.

Other demerits, including a chronic trade deficit, explain why the rupee is Asia’s worst-performing currency. It lost 5% loss versus the dollar in 2025 and is down 2.1% so far this year (see below). Efforts to support the exchange rate have India selling US Treasuries. Its holdings are now at a five-year low of $174 billion, a 26% drop from the 2023 peak. India also saw $19 billion of foreign capital outflows in 2025. They are continuing, as evidenced by the Sensex stock index’s decline since the beginning of the year

Pictured: USD vs INR Source: Bloomberg

The ultimate conclusion is that Modi isn’t actively harming his own economy, as governments in the US and China (political purges and a property crisis) arguably are. But he faces a daunting to-do list to ensure that the benefits of GDP growth in the 7.0%-8.0% stratosphere reach a critical mass of India’s 1.47 billion people.

Justin Oliver

—————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 31/1/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 YTD estimate takes the MCAS November 2025 YTD estimate and deducts the estimated charges of the Astro feeder fund. *** Morningstar as at 31/1/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2026 Freedom Asset Management Limited.