.jpg)

Weekly Newsletter

Freedom Calls: 26/1/26, "Davos deciphered and gold continues to march forward"

by

The Team at Freedom Asset Management

January 26, 2026

6 Minutes

Freedom Calls: 26/1/26, "Davos deciphered and gold continues to march forward"

From the team at Freedom Asset Management

Our thanks to those of you who joined us for our Abu Dhabi client event at the Four Seasons in ADGM last week. We heard from Justin Oliver (OGG), Ramon Eyck (MINC and OGF) and Cody Willard (USVIP). Pictured below (L-R): Sandrine, Ramon and Cody. We have Cody Willard on the road in the UK and Guernsey this week.

Davos deciphered

It was a busy week, not just for Freedom, but also in the Swiss mountain retreat of Davos. I cannot remember a previous Davos that was so rich in geopolitical and market content. I have been dipping into the speeches and podcasts of the week and share some observations:

Mark Carney – Canada has a wake-up call

Whilst not calling out Trump by name, Carney made a powerful speech in favour of the “Middle Powers”. He opened with a helpful summary of his speech in French, which we have lifted below (Source: weforum.org, Davos, Jan 2026):

“Today I will talk about a rupture in the world order, the end of a pleasant fiction and the beginning of a harsh reality, where geopolitics, where the large, main power, geopolitics, is submitted to no limits, no constraints. On the other hand, I would like to tell you that the other countries, especially intermediate powers like Canada, are not powerless. They have the capacity to build a new order that encompasses our values, such as respect for human rights, sustainable development, solidarity, sovereignty and territorial integrity of the various states. The power of the ‘less power’ starts with honesty.”

It is well worth looking up the full speech, because I suspect it will be referenced for the next 20 years. It was brave, and it is the liberal rallying call – and we all love Canadians and Canada. His most potent line in the speech:

“… the middle powers must act together, because if we're not at the table, we're on the menu.”

Interestingly, the right might argue that Carney’s approach to dealing with the looming geopolitical challenge next door is to do things that it could have been done long ago. He went on to say:

“Since my government took office, we have cut taxes on incomes, on capital gains and business investment. We have removed all federal barriers to interprovincial trade. We are fast tracking a trillion dollars of investments in energy, AI, critical minerals, new trade corridors and beyond. We're doubling our defence spending by the end of this decade, and we're doing so in ways that build our domestic industries.”

So instead of getting drunk with the self-interested eco-sustainability festival groupies, Canada could have started all these actions many years ago and found itself in a much stronger position. But like the shepherd and the lost sheep, the key thing is we get there in the end. Needless to say, Trump was not impressed with any part of the speech!

This was no wake-up call for the Middle East

Whilst the last year may have been a wake-up call for Canada, in the Middle East, the UAE especially worked out that they could no longer solely rely on the US when Obama's team: (1) lost interest in the Middle East (the result of increased US domestic oil production), and (2) appeased the Iranians, with a nuclear deal that left them dangerously on the precipice of being able to develop a nuclear weapon.

Importantly, the mood also changed in January 2022 when the Yemeni Houthis sent missiles to the UAE and both London and Washington were initially silent. The cost of that silence came only one month later when Boris Johnson’s London and Joe Biden’s Washington expected the UAE to automatically fall into line and implement sanctions against Russia for the Ukraine war, and the UAE government said, “err…. hang on a minute”.

The UAE realized then that it needed to build a less dependent foreign policy – and let’s call it that “Houthi moment” fast tracked the UAE to build a modern Switzerland, which listens to all major voices and provides a safe and secure venue for global dialogue. As a result, (almost) everyone is welcome to come, live, visit and do business in the UAE, and the UAE is friends with, and respects, all the major global powers. The UAE has prospered strongly from this position.

Back to Davos: Scott Bessent – US Treasury Secretary

I listened to an interview with Bessent (Source: CNBC, Davos, 21/1/26). 3 quotes sum-up the US positioning and frustration vis-à-vis Europe:

“Since 1980, the US has spent $22tr more on defence than the rest of NATO – that is approximately 2/3rds of the US outstanding government debt. So while the Europeans were building schools, having healthcare, we have been defending the world, and I think the President believes they should be paying their fair share.”

“Having worked with the Europeans, my guess is their next move will be to form a working group…. the dreaded European working group[!].”

“Four years into the Ukraine war, [Europe] are still buying [Russian] energy and refined products from India made from Russian oil… so four years in, the Europeans are still financing the war against themselves.”

He was happier when talking about the US economy.

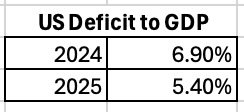

It is difficult to underplay the success of Trump’s US economy one year in. Trump’s three-legged stool for growth – tackling trade, taxes and de-regulation is working. Add to the mix: more controlled spending, tariff revenues, and the projected benefits of the AI revolution and the US made progress in 2025 and enters 2026 is a much stronger fiscal position that Trump inherited in 2024 (see table below).

Bessent believes that it is possible to bring the US deficit to GDP down to within 3% during this presidency. Think what that will do to all those projections of the US dollar’s downfall – at precisely the time when major European powers will be busting their budgets to meet new defence requirements. The US dollar may be a dirty shirt, but it is the cleanest one in the laundry pile.

He went on to talk about running the US economy hot, like under the Alan Greenspan years - this is probably worth another Monday letter. Bessent and Trump believe that you should not need to ramp up interest rates just because GDP grows strongly. There is an argument that AI will allow us to see GDP growth without the normal inflationary impacts. It is a relatively unorthodox economic view these days, but they might be right - and then what a difference that would make to deficit/GDP and debt/GDP ratios.

When you listen to Scott Bessent and then you listen to Rachel Reeves (UK Chancellor), you realise how lucky the Americans are!

Trump's pick for the new Fed Chair – (possibly) BlackRock's Rick Rieder

With Trump’s pick for the new Fed Chair to be announced potentially as early as this coming week, the prediction markets (e.g. Polymarket) have made a late last minute surge for a new candidate – Rick Rieder, the current CIO of global fixed income at BlackRock, the world’s largest asset manager, and one of the most senior figures at the firm since he joined in 2009.

As recently as 2 weeks ago, Polymarket reported that it was a racing certainty that the new Fed Chair would be one of two Kevins – Kevin Hassett (President of the National Economic Council) or Kevin Warsh (a former Fed Governor). But being Trump loyalists as both Kevins are, is not the right look right now.

Rieder would make a lot of sense, because at a time when Trump is often accused of trying to influence the Fed, Rieder – a previous Democrat donor like his boss Larry Fink – will sooth the US bond market, because there can be no doubt that he understands the bond markets. Rieder is well known to market participants through frequent TV appearances and also on record recently as saying that he believes that current interest rates do not support a vibrant housing market and favours a cut. A little known nugget about Fink: he was allegedly lined up to be the US Treasury Secretary under Hilary (had she won), so I would expect that Rieder would be well supported by the Democrats. And, as soon as he is in position, everyone will quickly forget the news flow with Jerome Powell.

So what does Davos mean for our portfolios and bank deposit rates?

If the Fed chair appointment goes as planned we will see rate cuts in the US this year - probably not as many as Trump would like, but certainly some cuts - this will directly impact deposit interest rates in the UAE and investors in MINC should see the benefits of broader market exposure and better liquidity than bank deposits will be able to offer.

There can be little doubt that defence companies will continue their upward march (benefiting OGF) and as Justin writes below precious metals (benefiting OGG). All of this is good for US equities and what is good for the US is usually good for Asia and emerging markets (OGG and OGF both benefit here on both counts).

Cody will tell us that none of the politics really matters for technology (USVIP) - the most revolutionary tech, the most efficient producer of tech will always win out in the end, and each of our governments whether they be socialist, republican or not democratic at all, need tech to be successful to deliver for their economies and communities. Both OGG and OGF have important allocations to tech.

I think the open point from Davos is whether Europe will get its mojo back and become an interesting place to invest (outside of defence companies). We will keep researching this space.

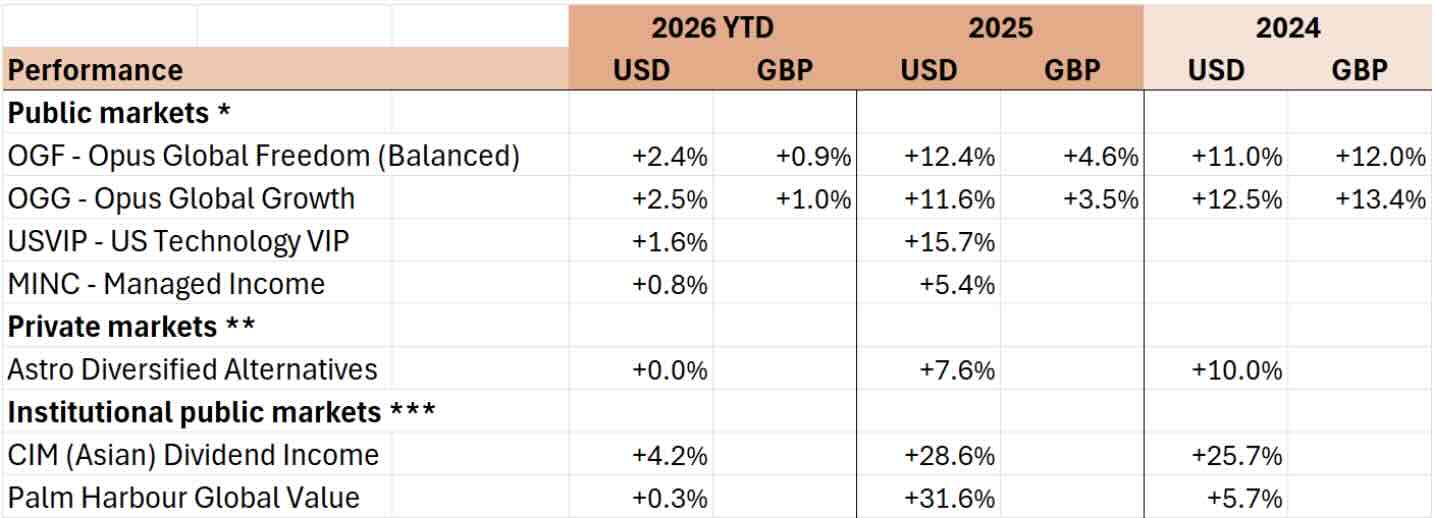

Performance

It was a little choppy mid-week as Trump flirted with tariffs on NATO allies, but by the weekend things had quietened down. Sterling strengthened, but like a rubber band, the more it moves away, the faster it will spring back - so at the risk of sounding like a broken record - a good time to deploy Sterling.

(For performance disclaimers, please see foot of email)

Our articles this week:

Canaccord's Justin Oliver, believes that precious metals have further to run

10,000 Days' Bryce Smith writes for us that "Revolution Investing requires both intuition and reason"

Please scroll down to read the articles.

I shall be in London and Guernsey this week, before taking a week off in the Swiss mountains. Wherever you are this week, please let me wish you a peaceful and prosperous week ahead.

Adrian

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

—————————————

"Precious metals have further to run”, 26/1/26

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Precious metals have started the year with strong momentum. The price of gold moved further into record-high territory last week, lifted by steady demand from investors seeking a safe haven, rising expectations of easier monetary policy, elevated geopolitical risks, and continued purchases by central banks, particularly in emerging markets, as they continue to diversify their reserves away from dollar-denominated assets. Other precious metals—including silver, platinum, and palladium—have appreciated recently, too, buoyed by demand from investors using them to hedge against a weaker dollar. The dollar fell about 10% last year.

Investors think the Federal Reserve is likely to either hold or ease interest rates further this year. Supporting these expectations are the weaker than expected December core CPI reading released last week. Even as inflation cools, the gold price is rising because real interest rates are expected to remain low, limiting the appeal of cash and bonds.

Further, elevated market and geopolitical risk across multiple fronts is pushing precious metals prices higher. At home, there are growing concerns over the Fed’s independence, following the Department of Justice’s criminal investigation of Fed chair Jerome Powell, and over President Trump’s threat to take over Greenland. Abroad, there are the ongoing tensions in the Middle East, with mounting risk of a US/Iran conflict; the war that persists in Eastern Europe as Ukraine continues to hold its line against Russia; and tensions that remain high in relations between Washington and Beijing even as both the US and China signal interest in keeping diplomatic channels open. All these developments have reinforced precious metals’ appeal as a store of value, in addition to raising global supply concerns.

Also, investors recognize that gold’s cousins, the “other” precious metals, have industrial-use cases suggesting growing future demand amid tight inventories. Semiconductors, for example, aren’t the main driver of appreciating precious metals prices, but they represent a demand narrative that certainly helps (i.e., the semiconductors needed to run AI programs contain precious metals including gold, silver, palladium, and platinum).

In terms of specific price movements:

(1) Gold. The move of gold’s spot price to fresh highs above $4,800 per ounce as of January 22 looks less like the result of speculative buying than a repricing of geopolitical risk and monetary policy uncertainty. We would not be surprised if Gold were approaching $6,000 by the end of this year.

(2) Silver. Silver’s spot price move above $90 an ounce, for the first time ever, on January 14, underscored the convergence of safe-haven demand, industrial usage, and constrained supply. As investors moved to hedge dollar weakness and geopolitical uncertainty, silver didn’t simply track gold higher but accelerated its climb, reflecting thinner liquidity and a tighter effective supply base. Unlike gold, silver is rarely mined on its own. Roughly 70% of global supply is produced as a byproduct of other metals, leaving supply slow to respond even when prices rise sharply. With inventories presently tight, the surge in the price of silver during early 2026 looks less like a supply shock and more like demand colliding with limited supply flexibility.

Because silver is used heavily in the manufacture of products connected to energy security and geopolitics (e.g., solar panels, electronics, automotives, and defence applications), its price is particularly sensitive to shifts in risk sentiment. Consistent with our expectations for rising gold prices by year-end and absent any change to these dynamics, spot silver could feasibly reach into the $100s and beyond, Reuters observed.

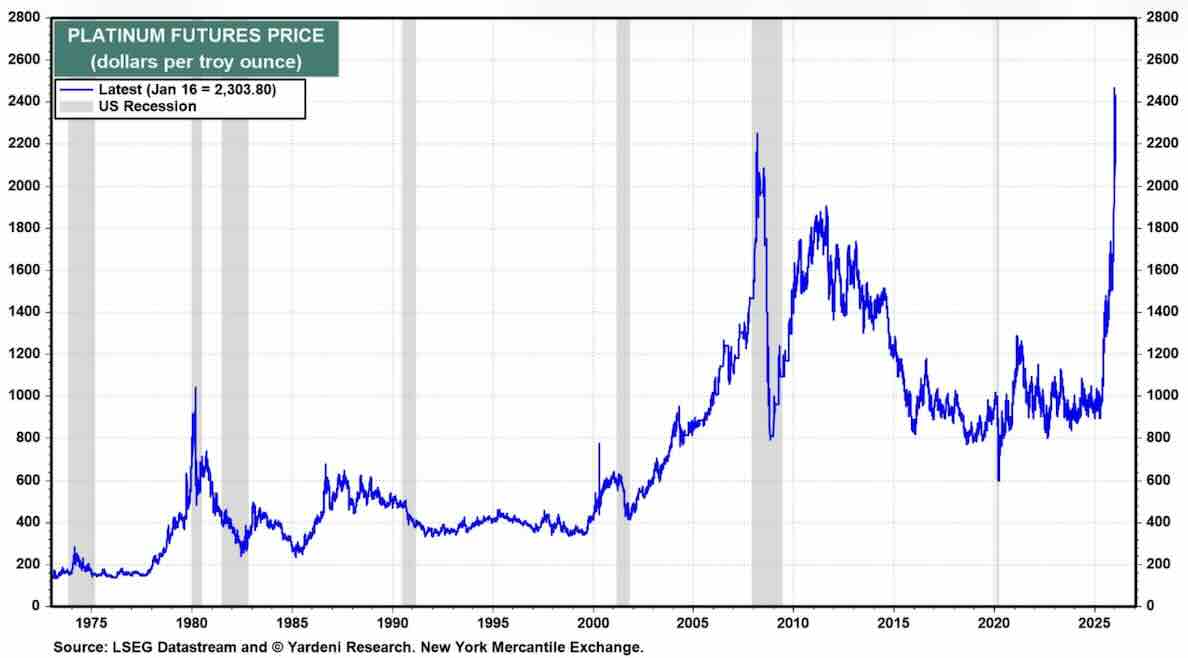

(3) Platinum & palladium. While gold anchors portfolios as a monetary hedge and silver straddles monetary and industrial demand, platinum and palladium remain fundamentally industrial metals, with usage tied closely to autos (especially electronic vehicles), energy, and specialized manufacturing. Both markets are highly supply constrained after years of underinvestment and geographic concentration, leaving prices sensitive to even modest imbalances.

Russia remains a critical supplier of platinum and palladium, keeping sanctions risk and export disruptions embedded in pricing. Platinum’s long period of price dormancy gave way to a record high near $2,480 per ounce in late December before the price eased back toward $2,300 in mid-January. The price of palladium has moved upward as well, but in a more measured fashion, reflecting earlier repricing tied to EV adoption.

In short, while precious metals have begun 2026 with a bang, there are valid reasons why this rally can persist.

Justin Oliver

——————————————

"Revolution Investing requires both intuition and reason", 26/1/26

By 10,000 Days' Cody Willard and Bryce Smith - Advisers to US Technology VIP Fund

Bryce here. I'm reading Walter Isaacson's biography of Steve Jobs and it's shocking how obsessed Jobs was with self-awareness and intuition. He studied Eastern religions extensively and said that while the West has done a great job with reason, it has lost intuition.

Whether you call it intuition, a gut feeling, a hunch, vibes, or something else, there is more to business and investing than strictly reason. We lack perfect information, and sometimes reason fools us into thinking we have it. We analyze numbers, build models, compare valuations, and create spreadsheets. And while all of that is fine, investing involves much more than just spreadsheets and 10-Ks.

That’s why we have to learn to listen to and leverage our intuition. Intuition is built through our life experiences. Through feelings and emotions; fear, pride, guilt, etc. Through our interactions with the ones we love and society at large. It’s the way we can “know” things without knowing them for sure.

Our appreciation of beauty and art comes from the same place as intuition, not reason. But it is impossible to measure, yet it is critically important in business and investing. Cody often encourages the team here at 10,000 Days Capital to go to museums and experience art and beauty firsthand for this very reason.

Much of our style of Revolution Investing relies on intuition, and we shouldn’t discount that or view it as a flaw. Intuition is what really gives us a glimpse into a company's future, and how the world might be different ten years from now, and how a product can become a platform, among other things. And these are the things that matter most when considering how to invest for the long term. You simply cannot see an unknown future with reason alone.

As our process uses both intuition and reasoning, and I wanted to jot down some of the principles that fall within each category:

Principles of Intuition:

- Platform Status/Potential

- Exponential Change

- Empowerment of the End User

- Network Effects

- Incentives

- Vision

- Scale

- Betting on Brilliance

- Beauty

- Empathy

Principles of Reason:

- Forward Price/Profits Ratio

- Growth Rates

- Gross Margins

- Switching Costs/Lock-In

- Monopoly Power

- Net Cash on the Balance Sheet

- Expense Discipline

- Management Alignment

Our merger of the Principles of Intuition and the Principles of Reason yields our style of Revolution Investing. And our merger of these principles is in and of itself an art form, not a science. The principles of intuition lead to inevitability: these things should happen, must happen, and will happen. The principles of reason ensure we don’t overpay for that ultimate inevitability, which is quite possible to do.

And we are not saying that our style of investing is the only way to invest (there are lots of ways to skin a cat), but it’s our style, and we have to own it if we are to be successful.

In conclusion, we should never discount our intuition. It’s as critical, and perhaps even more critical to investing than reason alone. Both are needed. Without reason, you can lose your grounding. But without intuition, you can never see a future which has not come. Steve Jobs was a master of intuition and self-awareness and still a brilliant operator. But I think it was his intuition, his gut, that told him how to design, how to build, how to hire, how to grow, and how to make bets. We must continue to do the same and focus on doing it even better.

Bryce Smith

—————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 25/1/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 YTD estimate takes the MCAS November 2025 YTD estimate and deducts the estimated charges of the Astro feeder fund. *** Morningstar as at 25/1/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2026 Freedom Asset Management Limited.