.jpg)

Weekly Newsletter

Freedom Calls: 23/2/26 Trump 0 - The Supreme Court 1… and it's hotting up in Iran

by

The team at Freedom Asset Management

February 23, 2026

10 Minutes

Freedom Calls: 23/2/26 “Trump 0 - The Supreme Court 1… and it's hotting up in Iran”

From the team at Freedom Asset Management

Pictured below the new crescent moon shining above Abu Dhabi’s serenely beautiful Louvre museum marking the start of Ramadan last week.

Picture credit: Sandrine

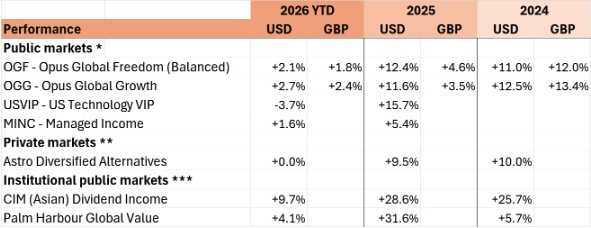

Let’s get the numbers out of the way, because they are pretty good in absolute terms (OGF, OGG and MINC) and relative terms (USVIP). And for a welcome change, they are even good in Sterling.

Performance

(For performance disclaimer please see foot of email)

Trump loses on tariffs, corporate America wins…. And consumers lose again

Tariffs were always going to be a difficult one to win in "the land of the free". And whilst I understood where Trump was coming from (in a way that seems to baffle most Nobel prize winning economists), the Supreme Court has now spoken. It is difficult say that Trump took it well. And effectively what has happened is that the Supreme Court has just given a $170bn bailout package to American retailers/importers…. and their corporate lawyers. Because whilst they will find it very easy to find the invoices that show the tariffs they (or someone in the chain) paid on imports, I am fairly certain they will claim it is impossible to pass on those savings to the American consumer, because no such simple invoice chain exists. The possible exception might be Amazon who certainly have the technology to work that out - I’m just not sure they will offer it up straight away.

To the skeptics out there, it proves that it really does not matter who is running the country, corporate America always wins! Et voilà …. the S&P500 was up about 0.7% on Friday.

It’s getting hot in Iran

We held an investment committee on Thursday from Guernsey for our Opus Global Freedom Fund (OGF or the Balanced Fund) - and we talked about Iran. We took the unusual step to dial back risk significantly for the short term. So, we went into this last weekend with and equity/risk weighting of 47% (down from 62%). We left our active positions unchanged in defence, technology, Asia and emerging markets, but sold 12% of S&P500 ETFs. We also initiated a new 3% position in a commodities fund which has a significant exposure to the very cheapest names in oil and gas.

You might ask “why have you cut risk - aren’t you positive about markets for this year?” And the answer is that yes we are positive for the year, but if we have an opportunity to lower our volatility over the next 4-6 weeks, that just feels like a good idea because we think there will be some military action against Iran over the coming weeks and possibly very soon. If that happens, markets will most likely fall quickly - and when they do, we plan to buy back all the risk we took off on Friday - hopefully at a lower price. If there is no military action, we will wait until the coast is clear and buy it back at hopefully a price not too far away from the current levels.

Our reasoning is thus:

The US Navy build-up in the Middle East is unprecedented - the very successful 12-day war on Iran last year was done remotely. The US now don’t need to use their airbases in the Middle East for a more sustained campaign, if they have this carrier set up in place. The Gulf countries have so far refused to allow the US to attack Iran from their local bases. And whilst I don't think regime change is remotely realistic in Iran, nor is a land invasion, after Venezuela, an emboldened Trump taking his cue from his Israeli supporters may want to inflict as much damage as possible on the Iranian regime to remove its nuclear threat for decades. If Trump were going to do it, it would be now.

There is a no-fly zone over Iraq at least if you are a US or British commercial airliner in the last c.3 weeks, because that is the route that Israeli missiles would take to reach Iran (see below). When I flew Doha to London last week, we didn’t fly up the Gulf and through Iraq, as normal, we instead turned left straight away, which adds a good 30 minutes to the flight time; nobody does that unless they have been told to do so. Interestingly, Etihad and Emirates are flying straight through Iran, but that’s another story for another time….

Pictured: BA122 routing Sunday 15/2/26

So we hope it won’t come to blows, and it may just be Trump doing his "maximum pressure act", but we do think the calculus has changed in the last couple of weeks, and it makes sense, at least in our balanced fund, to dial down the risk for now.

Meanwhile in Moscow…

I caught up with some sources in London last week. It seems Moscow has now been plunged back to the mid-90s with no mobile data service. The service has been dropped, because it was being used by the Ukrainian drones to seek their local targets. My source tells me… the strange thing is nobody seems to care any more... soon they will be pulling out their Nokia bricks from the back of the cupboard.

More importantly, on the peace deal, I asked how we might reach an understanding on a land transfer with Russia demanding Ukraine give up all of the Donbas region. The Ukranians do not want to give up the c.10% of Donbas that they still control because that is where their battle lines are - and they do not have fortifications on the official Donbas border to move back to.

So it seems a possible solution is two-fold: firstly, the Ukranians hold a referendum to agree to land being transferred - hence the referendum that has been called for mid May, but the second part is potentially more cute. In the Russian constitution, the Donbas region is not defined in terms of territorial limits. So the “clever" solution is to move the border to where the current Ukrainian defensive lines are. This would allow Putin to claim that he has captured “all” of (the newly defined) Donbas and the Ukrainians do not have to give up their hard fought battles lines. Let’s see how this plays out.

Our articles this week:

10,000 Days’ Cody Willard and Bryce Smith (Advisers to USVIP) bring us an in-depth look at the next groundbreaking AI feature from the Meta stable in “The Manus Moment: Meta’s path to become the OS of the enterprise”; we have asked Bryce and Charles to give us a training webinar on Manus - so look out of that in the next couple of weeks.

Canaccord’s Justin Oliver (Adviser to OGG) reports on the latest EU meeting to address the trade challenges coming from the US and China in his note: "Europe organises a committee …. to be decisive.”

This is a busy week of travel to London, Hong Kong and ending up in Tokyo for the rest of the week. The investment community is getting very excited about Japan and we will be sitting down with some of the managers we have allocations with to hear the story up close. I shall be based in Hong Kong the following week.

Please remember we are hosting a webinar with Cody Willard at 1500 London/1900UAE time today. Cody is always fascinating and entertaining. Please reach out to your usual Freedom client team member for details if you haven’t signed up, or just reply to this email.

Wherever you are please let me wish you a wonderful and peaceful week ahead!

All the best,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

——————————————

“The Manus Moment: Meta’s path to become the OS of the enterprise", 23/2/26

By 10,000 Days' Cody Willard and Bryce Smith - Advisers to US Technology VIP Fund

So agentic AI kills software, but who builds the agents?

That’s the question I set out to answer three weeks ago or so. These days it feels like industries (or at least stock prices) are collapsing left and right because of the threat of “agentic AI.” But I’ve never built an agent. And other than the vibe coding apps like Replit, I had never really used a true AI agent. I understood the premise of agents: AIs that can actually do things. But I’m looking at stock prices of logistics firms and real estate brokerages crashing because of what seemed like mystical, unseen, far-away agents.

So I went on a journey to find where these agents live, who’s building them, and find out how they work in practice. This path led me mostly down a road of confusion and frustration at first, but I eventually landed on what I think is one of the most Revolutionary platforms I’ve used in my life. I’m talking about Manus AI (which was recently acquired by one of our largest holdings, Meta Platforms (META)).

Above a screenshot of Manus’ user interface. At first glance, it looks just like ChatGPT or any other chatbot, but there is much more to Manus than meets the eye.

Manus is an AI that does real work. It is a multi-agent orchestration system that takes the users’ intent and turns it into outcomes. Unlike standard chatbots, there is no copying and pasting between apps to get work done. You just open the app, tell Manus what you want done, the agent goes to work (sometimes for 15 minutes, 30 minutes, or even an hour), and comes back with a result. Here are just a few things that I did on Manus this week that I have tried and failed to accomplish on other AI platforms multiple times in the last year:

Build and publish a working AI-powered fitness app for Android with the push of a button (no backend setup required)

Autonomously locate potential investors for our fund, research their backgrounds, draft and send custom emails to each lead

Read and respond to my most-pressing emails every hour

Build a fully functioning dashboard for our hedge fund with real-time price data, exposure analysis, and intraday P&L. Positions are updated daily by finding our broker statement in my email.

And More!

Critically, Manus is as easy to use as ChatGPT or Gemini. There is absolutely no coding involved, no API keys, no database setups, nothing that would require any sort of technical background. This was a remarkable differentiator from every other “agent” platform I tried to use.

Manus was a refreshing, nay, Revolutionary experience after two weeks of struggling to find an agent-building platform for an ordinary person like me. I tried everything I could get my hands on including Google’s Gemini Enterprise, Vertex AI, Replit, Anthropic’s Cowork, OpenClaw, LangChain, and Zapier. I couldn’t get access to Salesforce’s Agentforce without paying big fees up front, but I met with their team twice and reviewed several demos, and it was nothing like Manus.

The problem with legacy software’s approach to agents is that they are trying to create agents that go through the back door, and Manus (and a few other platforms we will discuss) are Revolutionary because they go through the same front door that humans use. You see, Microsoft, Salesforce, Workday, ServiceNow, and tons of other companies are trying to pivot their enterprise SaaS platforms to be agent platforms with things like APIs. These platforms were designed to interface with humans, and those humans are being replaced by agents, so they are trying to recreate them from the inside out to accommodate the agents.

But what I’m calling the front-door agents – things like Manus, Claude Cowork, and OpenClaw – are Revolutionary because they operate like humans do. They work by giving AIs a computer to use, and then they can do basically anything a human with a computer can do. As long as the AI has your login credentials, it can access and use any app, service, or website that you use.

Manus’ advantage over Cowork and Openclaw is that it operates entirely in the cloud, whereas these other programs are downloaded to your computer. Today, most work happens in the cloud (via a browser) and almost all enterprise data is in a data center (whether cloud or on-prem). Very little work is done nor data stored on the actual end devices these days. Moreover, Manus has huge advantages in terms of security and safety, because it is not living on your device like Cowork or Openclaw. Manus spins up its own virtual machine in the cloud every time you talk to it, so if it goes AWOL, it doesn’t screw up your device or compromise your safety.

I could talk about the Revolutionariness of Manus for days, but I’ll stop here and I encourage you all to try it for yourself (it’s $40/month and you can get a 7-day free trial.).

So what does this mean for Meta?

With Manus in its pocket, I think Meta is positioning itself to be the platform where businesses (and consumers) train, orchestrate, and monitor AI agents. If Meta pulls this off, it has the potential to be the OS-layer for businesses in the age of AI. Thereby dethroning titans like Microsoft and capturing a ton of the value formerly captured by the enterprise SaaS industry.

Meta is already integrating Manus into its Ads Manager. This allows advertisers to simply describe their goal and budget to the agent which can then build the content, target the market, purchase the ad, and repeat this process to optimize for the highest conversions.

And soon it will be integrated into WhatsApp, and it’s not hard to imagine a future where we will be running our businesses by texting agents on WhatsApp. And if you’re in Milan watching the Olympics, don’t worry, you can talk to your Manus Agents via your Meta Ray Ban Glasses.

Soon, the “jobs” of human employees will be training and coordinating agent employees. Salespeople won’t log in to Salesforce to update a lead, they’ll just text their Manus Agent. Or they can teach their Manus Agent to do it automatically as soon as they send a sales email. Analysts won’t build spreadsheets in Excel, they’ll just connect their data source to Manus and ask Manus any questions they might have.

Most of today’s enterprise applications will essentially be reduced to “dumb” databases storing information, and all of the value will be captured at the orchestration layer, i.e. Manus, which is performing the actual work. A company’s edge will be determined by how well they train and orchestrate their agents. All digital tasks will be done by computers, and our job will be to determine which digital tasks those agents perform.

To be clear, I don’t think Meta will be the only player here (I think Google has a real chance of being the other major competitor), but I do think Meta has a strong lead out of the gate versus the competition.

Meta has two distinct advantages that give it a good chance to be the leading agentic platform of the future: (1) dedicated compute; and (2) an unrivaled user base.

First, Meta is the only big tech company that has the massive compute required for agents and isn’t selling that compute to third parties. Agentic AI requires orders of magnitude more compute than chatbots (remember, these things work for hours (and soon days) at a time, like real employees). Google, Amazon, and Microsoft all have more total AI compute, but they have to split those resources amongst their existing services, and critically, their third-party cloud customers. Every GPU that Microsoft puts to use powering an agent is a GPU that they cannot rent to a customer at ridiculously high margins right now.

I think Zuckerberg sees this and that’s the reason he is pressing forward with a massive compute build out despite Meta not having its own cloud business (ironically, this is why the stock is down recently). Meta will be uniquely positioned to scale always-on, agentic employees to billions of users because it will have literally millions of Nvidia GPUs dedicated solely to this purpose. This also gives Meta a big advantage over startups like OpenAI and Anthropic (which, to be clear, see this coming and are also trying to build the agentic OS layer) which have to rent compute from others.

Second, Meta can instantly scale and distribute agents to billions of users, and shockingly, it has the largest user base of businesses of any platform in the world. Today, over 50 million businesses use WhatsApp to interact with customers (that’s the number of businesses, not the number of users!). That’s more than five times the number of businesses using the next largest SaaS platform (which is Google Workspace). The chart below compares Meta’s business user-base to those of the next largest enterprise SaaS companies:

To be fair, the average Microsoft 365 customer is worth a lot more than the average WhatsApp Business customer. But Meta is just getting started, and they will exploit this massive user base to move up the market. It is worth noting that WhatsApp Business is bigger than just free messaging accounts. Paid business messaging on WhatsApp is approaching a $3.6bn annualized run rate. They also recently rolled out "Click-to-WhatsApp" which lets consumers reach out directly from ads they see on Insta and Facebook. Finally, there are also 5 million businesses paying for enterprise scale usage via the WhatsApp API.

As individuals start using Manus agents for their personal lives, they will bring them into the organizations they work at, just like they did with the iPhone. Unlike all of its competitors, Meta won’t need a gigantic B2B sales team to push Manus to the corporate world.

In conclusion, I think Meta has the potential to be the layer at which all digital work of the future is coordinated. Almost everyone sees Meta as a social media company, and I know the Wall Street analysts don’t have any enterprise SaaS revenue baked into their financial models for Meta. Meta is trading at about 21x forward earnings, its social media revenue is accelerating to 30% y/y next quarter, we’ve got the potential for billions of AI glasses shipping in the next few years, and now we’ve got the Manus AI kicker with the potential to uproot and expand the $500 billion annual enterprise SaaS market. In short, we really like the risk/reward setup for Meta here. We maxed out our allocation to Meta in the US Technology VIP fund this week in case you were wondering.

Bryce Smith and Cody Willard

—————————————

“Europe organises a committee …. to be decisive", 23/2/26By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

After a year of navigating the duelling trade policies of the US and China, Europe finally has a plan to boost competitiveness and potential economic growth. Whether that plan is enough, or will be enacted with sufficient haste, is still an open question.

On February 12, European Union officials gathered in a Belgian castle to address a range of stalemates, from bureaucracy to excessive regulation to investment to the long-sought integration of capital markets. Former European Central Bank (ECB) President Mario Draghi, a leading proponent of increasing competition, urged leaders to “move faster.” French President Emmanuel Macron said there are “no taboos.” European Commission President Ursula von der Leyen gave the bloc until June to agree on a long-stalled union of financial markets.

From all the lofty talk, something remarkable emerged: EU officials finally admitted that it has taken far too long to get all 27 member countries to agree on a plan for greater economic efficiency. So if the EU makes insufficient progress by June, smaller groups - as small as nine members - could move ahead on “enhanced co-operation” to accelerate reforms.

Von der Leyen told reporters: “Often we move forward with the speed of the slowest and the enhanced co-operation avoids that. The pressure and the sense of urgency is enormous, and that can move mountains.” Much of that urgency is coming from Washington and Beijing, both of which are sending different kinds of headwinds the EU’s way.

Draghi, who since 2024 has been publishing reports on how to revamp Europe, called the current economic world order “defunct” and “dead.” At issue, the former Italian prime minister said, is that the EU faces a US that “emphasizes the costs it has borne while ignoring the benefits it has reaped” over the decades. Where President Donald Trump takes his trade war in 2026 is anyone’s guess. His threat of a 100% rate on eight European countries over Greenland suggests Trump hasn’t gotten tariff-slapping out of his system just yet.

With China, Draghi said, Europe faces a rival that “controls critical nodes in global supply chains and is willing to exploit that leverage, flooding markets, withholding critical inputs, forcing others to bear the cost of its own imbalances.” China’s overcapacity and the knock-on effects of President Xi Jinping’s decade-old “Made in China” program are making life difficult for Germany and other top European economies. The ever-increasing threat from BYD and other mainland electric vehicle makers alone is challenging the continent’s industrial model. It’s also the case that China is speeding up the globe’s economic clock. For all its challenges, including a giant property crisis that’s fuelling deflation, the hyper-competitiveness emanating from its $19 trillion economy is remaking commercial relationships everywhere.

All this has the EU racing to implement a “One Europe, One Market” strategy. Just not nearly fast enough. The hope is for the initiative to be operational by the end of 2027. Given the threats coming from Washington and Beijing though, that’s around 22 months too late.

The plan consists of three main pillars:

(1) Lowering administrative hurdles. Among the notorious administrative burdens that slow economic upgrades to a crawl and have to go are: 1) “gold-plating,” which requires national legislatures to ratify all EU directives; and 2) the “sunset clause” that automatically expires regulations and agreements, forcing the 27 countries to renew them over and over again.

(2) Integrating markets. Creating a single, integrated market for capital across EU member states would diversify funding sources for small businesses, especially startups, and strengthen the competitiveness by reducing reliance on bank lending. It would take off the drawing board the so-called “28th regime” that creates a single, harmonized set of rules for startups and put it into action.

(3) Creating a single energy market. Having one EU energy market with cross-border energy grids is considered vital at a time of Russian aggression. The idea is for the rubber to hit the proverbial road at the European Summit in early March. Yet for all the ambition on display at Alden Biesen Castle, the same self-inflicted wounds that long hobbled change are on still on display. One is the traditional rift between top EU economies. Germany thinks deregulation and the simplification of financial rules are more important. France wants to slap tariffs on China and prioritize “Made in Europe” policies that protect local manufacturers and increase public investment funded with Eurobonds. German Chancellor Friedrich Merz said “I will not support” the issuance of joint debt. There are many reasons to worry EU leaders are biting off more than they can chew. The vital step of ending gold-plating, for example, would mean countries’ transferring more national power to Brussels than tolerable.

How to incentivise the ample private investment needed to make economic disruption worthwhile for EU member states is an open question. Carsten Brzeski at ING Bank thinks a European sovereign wealth fund could do the trick. Funded by private and public capital and open to retail investors, the fund could invest in pan-European projects across infrastructure, defence, and AI. The EU would have to act boldly and credibly to succeed. Europe, Brzeski noted, “has never really suffered from a lack of plans or grand vision; the real obstacle has almost always been weak implementation and national interests taking precedence over European ones. Whether this time will be any different remains to be seen.”

Draghi, who’s known for doing “whatever it takes” during his ECB days, said at the summit that unless Europe learns to adapt to a fast-changing world and respond with strength, it risks “becoming subordinated, divided, and deindustrialized at once.” In a world “where trade and security intersect,” he concluded, “our strengths cannot protect our weaknesses.”

Ultimately, the question is not whether Europe understands the urgency. It clearly does. The question is whether it is prepared to match rhetoric with decisive action, even when that means surrendering some national discretion for collective gain. In an era where trade, technology and security are increasingly intertwined, hesitation carries its own cost. If Europe fails to move with speed and unity, the risk is not merely slower growth, but diminished influence in a world that is reorganising at pace.

Justin Oliver

—————————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 21/2/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 estimate takes the MCAS December 2025 estimate and deducts the estimated charges of the Astro feeder fund. *** Morningstar as at 21/2/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2026 Freedom Asset Management Limited.