.jpg)

Weekly Newsletter

Freedom Calls: 22/12/25, Happy Christmas and what happens when Vegas goes full AI!

by

The team at Freedom Asset Management

December 22, 2025

5 Minutes

Freedom Calls: 22/12/25, “Happy Christmas and what happens when Vegas goes full AI!"

From the team at Freedom Asset Management

Pictured: the “Guernsey” team Christmas lunch in London (L-R: Charles, Alan, Bill, Ramon, Bob) and missing Dave.

Pictured: the Abu Dhabi team Christmas dinner (L-R: Greg, Nikita, Sandrine, Toby, Shawn, Shireen, Clany, Derek and Charles) and missing Sam.

As we head into the home straight that is the week of Christmas, I want to take a moment to thank all our investors, clients and "friends of the firm" that have put either their trust or their money (preferably both) with Freedom this year. We know there are many other places where you could invest your time and your money. We are always grateful.

We never forget our first job is to make money for our investors. Along the way, we also try to inform you about what is going on out there, hopefully in an accessible way, and sometimes against a cacophony of clickbait seeking journalists, hysterical politicians, and other “experts” often talking their own book. The difference between us and “them" is that Freedom is always on your side.

And that is what these Monday letters are all about - I imagine us grabbing a quick drink, or going out for lunch, and these are the topics we would pick up on this week, pulling on the research and anecdotes from our investment teams and sources. I hope it gets your week started with the stuff that matters, the stuff that people are talking about…. and occasionally stuff that really does not matter at all(!)

Let’s get performance out of the way first.

Performance - "I will have some more of that please"

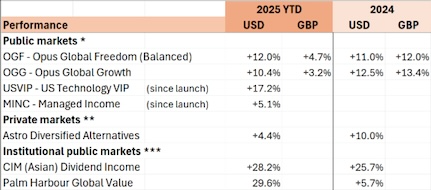

Barring natural (or unnatural) disasters before the end of the year, we have printed another set of double-digit US dollar returns in our core private client balanced (OGF) and growth (OGG) funds. We are excited about how 2026 looks from here as Justin’s article below articulates.

(See performance disclosures at the foot of this email)

We are delighted with the start of our new private client funds - our US Technology VIP fund (USVIP) has made a blistering start, at the forefront of the AI and robotics revolutions. We think we are still in the first innings here, so strap yourself in for the ride. We are looking to bring an institutional version of this fund to our European clients in 2026.

Our Managed Income fund (MINC) has made an excellent start, as our most cautious investment strategy, delivering returns that have beaten US dollar bank short term deposit rates, especially those from UAE banks.

Our Astro Diversified Alternatives fund (ASTRO) is our feeder into Mubadala Capital's $4bn highly diversified private markets portfolio. Performance numbers are always difficult to map week-to-week, because this fund only prices quarterly, but our recent conversations with the Mubadala Capital teams encourage us to expect a good set of fourth quarter numbers, which will materialise in 1Q’26.

Institutional clients

For our long-standing institutional clients, the CIM Dividend Income fund has delivered another knock-out year of performance and now stands at over $1bn - and is the Asia value fund of choice for some of the most respected institutions across Europe. That strategy is well placed to perform in 2026, as yield hungry Chinese insurance companies load up on high yielding “H” shares (amongst other reasons).

New on the block for us this year has been Palm Harbour Capital’s Global Value fund. We have great hopes for this strategy, which is the very essence of global stock picking in its purest form. Peter Smith has put in a great set of numbers this year and we look forward to taking that message out to our European institutional clients in 2026.

Our articles this week:

10,000 Days’ Bryce Smith and adviser to USVIP goes to Las Vegas to compete in the "World Series of Team Roping" - he reports back on the likely path to AI adoption in America’s favourite playground

Canaccord’s Justin Oliver and adviser to OGG, gives us his outlook for 2026, which (spoiler alert) is pretty positive

We are saving up some articles for next week, so expect a bumper edition between Christmas and New Year.

I am in Guernsey with the family over the Christmas week and then in London for the New Year’s celebrations.

Wherever you are spending this special week, I wish you a Happy Christmas!

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

———————————

“Las Vegas… team roping, and AI in casinos!", 22/12/25By 10,000 Days’ Cody Willard and Bryce Smith, Adviser to the US Technology VIP Fund

Bryce here. I'm back from a week in Las Vegas competing in the World Series of Team Roping. I was fortunate enough to win a check in one of the ropings (just enough to go back next year!). But while I was there, I of course had a couple thoughts on investing and economics that I wanted to share.

My father and I about to run our short round steer in the World Series.

The fundamental math of casinos and investing is opposite, yet most people approach both as if they’re the same

Casinos are a business, and the house doesn’t offer any games where the odds favor the player. Even though pretty much everyone knows this, millions of people collectively spend billions of dollars gambling every year, hoping to get lucky.

And that’s how most people approach the markets too. But the major difference with the markets is that the odds, in the long term, favour investors, (especially when you bet on the averages and invest in Revolutionary tech). This is because as an investor, you are generally investing money in companies that earn profits, i.e. create value.

Of course, there are winners and losers, bull and bear markets, booms and busts. But in the long term, entities that create value for the world (i.e. earn a profit) return most of that value to shareholders. Moreover, the indices offer a special advantage because they add the winners and eliminate the losers.

Further, while it’s almost impossible to gain an edge in the casino, it is possible to gain an edge in the markets. We've seen that our strategy of finding Revolutionary tech companies early on and holding them forever can lead to outperformance over time. These are the companies driving the most value creation for the world, and their stocks have worked out remarkably well for investors.

Of course, what we do still has risk. Any time you hand your hard-earned money to someone else and hope for a return, you are at risk. That's why I often reference this Peter Lynch quote:

"Frankly, there is no way to separate investing from gambling into those neat categories that are meant to reassure us. There's simply no Chinese wall, bundling board, or any other absolute division between safe and rash places to store money."

And just like you can get lucky in the casino, you can get unlucky in the markets (and many people do). Short-term trading, emotions, etc. all cut against an investor’s expected value (EV), to use a gambling term. But the difference is that in a casino, EV is always negative, whereas it is normally positive in the markets over the long term.

In addition, the principle of compounding works in your favour in the markets, and is basically absent in the casino. The longer you stay in the markets, the better your odds of success. The opposite is true in Vegas, where every role of the dice is an independent event with fixed odds that work against you.

But despite these stark differences in the fundamental maths of casinos and investing, most people approach them the same way. They invest randomly and emotionally, and never stay in long enough to let compounding work in their favour. In other words, most people turn positive-EV markets into negative-EV games through their behavior.

Accordingly, our job is to always ensure that we let the maths of investing work in our favour. That means finding the most Revolutionary tech platforms early and riding them through the volatility.

This world is not an "AI world" yet

Vegas still feels very old world to me. I think a lot of investors believe AI has sort of played out already, given the big moves we've already seen in the AI players like Nvidia and Google, but when you look at the real world, there is still so much value for AI and robotics to create over time.

Whether we look at Vegas sportsbooks, MGM’s website, or the many tired bartenders and dealers, you can see how AI and robotics will make everything about the town incredibly more efficient and entertaining. In the future, casinos will use AI to help create content, or build a better AI-powered app, or create new games and shows that are custom-tailored to different audiences. Not to mention, most of your transportation around town will almost certainly be in autonomous vehicles (Teslas, Waymos, and newcomers, like Amazon's Zoox).

Further, there is a good chance that most dealers, bartenders, and bellhops will be replaced and augmented by robots. We don't think that means there will be no jobs for humans, they’ll just move further up the value chain, performing more creative and strategic jobs than standing at a table shuffling and dealing cards for hours on end.

That said, humans will likely command a premium price where they do remain in these jobs, as many customers will still prefer to engage with a beautiful/handsome bartender or dealer, rather than a robot.

Although AI has already made so much progress, it's not surprising that Vegas has been slow to adopt and change. Just think about how long it took for old-world companies to adopt prior tech Revolutions like the internet, smartphones, and social media. It took five, ten or sometimes even fifteen years before most companies had websites after the internet went mainstream. It took seven years after the iPhone's launch for most companies to launch their own app. The same was true of social media. Today, basically every consumer-facing enterprise has a website, an app, and a social media page.

Looking forward, it's only a matter of time before every company in Vegas integrates AI and robotics as a fundamental part of its business model. Every hotel will have a custom AI to make check-in seamless. They will have custom AI-built websites which drive higher bookings and conversions. They'll have AI-designed shows and advertisements. AI-powered voice agents will handle 99% of customer phone calls.

Pictured: An image of an AI/Robotics-powered casino I made with ChatGPT's new image model

For us as investors, this means there is still a long way before The AI Revolution is "played out”. Until you can call MGM Grand and book a room with a fully AI system, see a fully-AI generated show, and be dealt a hand of blackjack from an Optimus Robot (to name just a few examples) there is still A LOT more efficiency and entertainment for AI/robotics to create.

So to wrap up, I'll reiterate what Cody has been saying all year: "there's never been a better time or place to be a Revolution Investor than right here, right now."

Bryce Smith

———————————————

"The year ahead”, 22/12/25

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Our central forecast is that US real GDP should expand by roughly 3.0%–3.5% in 2026, building on what appears to be a 2.0%–2.5% gain this year.

With the labour force likely to rise only about 0.5%, this growth profile implies productivity gains of 2.5%–3.0% next year. Stronger productivity should help push unit labour cost inflation down to around 2%, bringing CPI and PCE inflation back towards the same level. Under these conditions, we expect S&P 500 earnings per share to rise from $268 in 2025 to roughly $310 in 2026. Several forces underpin this constructive outlook:

1. Trump’s focus on affordability pressures

President Donald Trump is preparing a nationwide tour under the banner “Making America Affordable Again”, a campaign tailored to the cost-of-living frustrations that dominated the November 2025 off-year elections. His strategy appears partly driven by polling data showing slippage in his economic approval ratings, as well as concerns over the 2026 midterms. The messaging will likely highlight proposals such as the “Freedom Means Affordable Cars” plan and measures aimed at reducing energy expenses, although Trump has at times downplayed the affordability challenge as a partisan fabrication.

The political salience of affordability intensified after Zohran Mamdani’s victory in the New York mayoral race, which shifted expectations for congressional control. Betting markets (Polymarket) show the probability of Republicans retaining the House falling from roughly 40% pre-election to 21.5% now. Trump has argued that a Democratic House would attempt a further impeachment.

Trump has repeatedly floated the idea of issuing $2,000 rebate cheques to lower- and middle-income Americans, funded through tariff revenue. He reiterated this proposal during a 2 December cabinet meeting, claiming the government would distribute a “dividend” in 2026 due to “trillions” collected. In reality, he would need congressional approval, and no legislation has been introduced. A legal challenge to the administration’s tariff authority could also undercut the revenue source. Meanwhile, tariffs have contributed to higher durable goods prices, meaning some levies may need to be rolled back if affordability remains politically damaging.

2. OBBBA as a significant fiscal boost

The One Big Beautiful Bill Act (OBBBA), enacted in July 2025, will deliver a substantial burst of stimulus in early 2026. Because many of the tax provisions were made retroactive to January 2025, households have largely not benefitted through payroll withholding; instead, the gains will arrive as large refunds at tax time.

Key provisions include:

Deductions of up to $25,000 for tip income

$12,500 (single) or $25,000 (joint) deductions for overtime pay

A $10,000 deduction for interest on personal-use auto loans

Additional age-based deductions of $6,000 (individuals) and $12,000 (couples) over 65, marketed as effectively eliminating tax on Social Security income.

On the corporate side, the bill reinstates several incentives from the 2017 Tax Cuts and Jobs Act, including full expensing of equipment and machinery and immediate deduction of domestic R&D costs, retroactive to 2025. These measures should support a revival in capital spending. The Congressional Budget Office estimates that OBBBA will lift real GDP growth by about 0.4 percentage points in 2026, taking their forecast from 1.8% to 2.2%.

3. Baby Boomers’ spending power

By 2026, Baby Boomers will be aged 62–80, and large numbers will continue transitioning into retirement. This cohort represents the wealthiest generation in US history, holding $85.4 trillion in net worth, or 51% of total household wealth, including $27.4 trillion in equities and mutual funds. Equity market gains therefore translate directly into a strong wealth effect, reinforcing their consumption.

4. Monetary policy turning supportive

The Federal Reserve has cut rates by 175bps since September 2024. Chair Jerome Powell noted in October that policy had moved considerably closer to “neutral.” Moreover, the Fed ended its quantitative tightening cycle on 1 December, shifting to a balance-sheet maintenance regime at roughly $6.6 trillion. This decision reflected concerns that reserves were nearing the lower boundary of “ample,” and it sought to avoid disruptions similar to the September 2019 repo stress. With policy lags still working through the system, this easing should meaningfully support 2026 growth.

5. Technology investment and onshoring momentum

The Magnificent Seven—Microsoft, Amazon, Alphabet, Meta, Apple, Nvidia and Tesla—are collectively expected to deploy over $500 billion in capital expenditure in 2026, guided by management outlooks signalling continued expansion of AI-related infrastructure. The bulk of this spend will come from the major cloud providers, all of which have indicated that their 2026 investment budgets will exceed 2025 levels.

Separately, onshoring remains a powerful driver of fixed investment. The administration has negotiated tariff arrangements that encourage foreign firms to build facilities in the US in exchange for favourable tariff treatment, with the White House highlighting nearly $10 trillion in cumulative public- and private-sector investment commitments.

Risks to the Outlook

Despite a constructive baseline, there are several potential downside risks:

1. Bond-market stress

The OBBBA-driven deficit will expand materially in FY2026. Some fear a potential sovereign debt episode, particularly with Bond Vigilantes already pressuring Japan and the UK. While US yields could face spillover pressure, the Treasury demonstrated in November 2023 that it can actively manage the curve by shifting issuance toward bills if required, reducing the likelihood of a disorderly spike in long-term yields.

2. Private credit vulnerabilities

High-yield spreads remain calm, but attention has turned to the rapidly growing private credit sector. We are less alarmed than many commentators: Fed easing supports refinancing, and lenders generally hold broad, diversified portfolios that can absorb isolated defaults. We will continue to track the performance of private-credit ETFs as a barometer.

3. A potential equity “melt-up” followed by a correction

Our base case assumes the expansion continues through the decade, sustaining the equity bull market. However, the late-1990s pattern—rapid valuation expansion followed by a sharp reversal—cannot be ruled out. A meaningful equity downturn could depress both consumer and business spending.

4. A retrenchment in consumer spending

Recent economic resilience has depended on strong spending by higher-income households and retiring Boomers. However, weaker job growth, tougher hiring conditions, and the affordability squeeze are weighing on sentiment. Consumption has held up impressively so far, but will be stress-tested in 2026.

5. Productivity disappointment

Our optimistic long-run outlook is anchored partly in sustained productivity gains. Critics argue the recent improvement is temporary and that AI may deliver limited near-term efficiency benefits. Historically, major technologies often reduce measured productivity early on, with benefits only materialising after long adoption periods.

6. Major geopolitical conflicts

Most geopolitical shocks ultimately create buying opportunities, but conflicts such as a Chinese invasion of Taiwan or Russian military escalation into Europe would radically alter the economic and market backdrop.

Despite these risks, we remain firmly on the optimistic side. The combination of robust productivity trends, sizeable fiscal stimulus, accommodative monetary policy, demographic spending power, and an unprecedented technology-investment cycle supports a constructive medium-term outlook.

Justin Oliver

————————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 21/12/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 21/12/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.