Weekly Newsletter

Freedom Calls: 17/11/25, The China issue and it’s time to top up on tech

by

The team at Freedom Asset Managment

November 17, 2025

12 Minutes

Freedom Calls: 17/11/25, "The China issue and it’s time to top up on tech"

From the team at Freedom Asset Management

Firstly, let me thank all of you who joined last week’s webinar on “vibe coding”, hosted by Charles and Bryce. It was a big turn-out and I learnt a lot!

This issue is coming out early as I board my Cathay flight back to London. It is quite a long issue, (but I hope worth the read if you have the time), so I will summarise the key points up front:

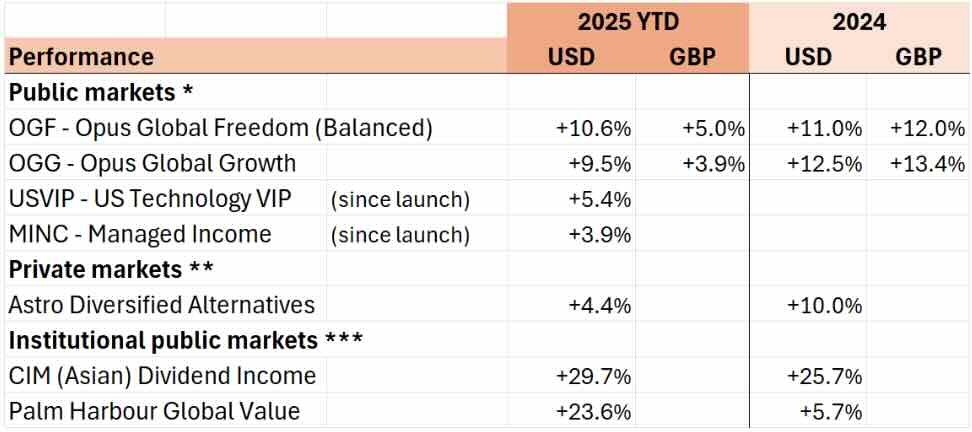

- Performance continues to be strong in our core balanced (OGF) and growth (OGG) funds estimated at +10.6% YTD and +9.5% YTD (respectively) in US dollars;

It is time to top up on tech – we are seeing a short term dip in prices, which would be foolish to miss out on if you are in any way a believer in the AI and technology revolutions. Email us if you would like a subscription form, or top-up form. I did a top up last week and I will probably do another one this week;

Cody and Bryce write about, “The great mystery of AI Return on Investment (ROI)”. This thoughtful piece argues that the economic benefits of AI cannot simply be counted in terms of Gemini or ChatGPT subscriptions, much to the annoyance of Wall Street analysts (and journalists);

- At a time of much excitement in markets, Justin Oliver gives us the “Reasons to feel confident about the health of the US financial system”;

- My write up on last week’s China visit.

As usual, please scroll down to read the articles.

“The China issue”

Last week I was briefly in Hong Kong, but long enough to confirm my belief that every Hong Kong Uber driver is long Palantir and Tesla. The main part of the last week’s trip was to visit one of our new managers in Hangzhou and then to meet other China A share managers in Beijing, around the CICC Investment Conference. As readers may remember we were granted an unlimited "QFII allocation" earlier this year, which allows our recently launched Hong Kong business to invest in Mainland Chinese companies - and we have set up and invested the first of several such funds we hope to launch.

Pictured: Anson and I joined by Stephanie and Andrew from Longqi Scientific at their headquarters in the wetlands of Hanzhou, Nov 2025

It has been a while since I was in Mainland China (2019 to be precise). I love Hong Kong, because it is visa-free for most of the world and you can zip in and out without any fuss, everyone speaks English and you can get a pretty good feel for Asia in a couple of days of meetings, most of which you can walk to.

I had been reluctant to find a week or two when I didn’t need my passport to wait for an official visa for Mainland China, so I had been putting this off. If you are an EU citizen you are fine, but Brits need to get a visa….. or use the slightly less well known “240-hour visa free transit scheme”. It basically means you can enter visa free for 10 days, but cannot arrive from, and return to, the same airport. So you cannot do a Hong Kong/Beijing return flight, but you can fly in from Hong Kong and leave to say Taipei, Abu Dhabi, London, or Macau as I did. Macau is only a one hour ferry ride to Hong Kong, so although it is not ideal, it is not such a big deal.

The whole system seemed a bit strange, so on Tuesday morning I showed up nervously at the Cathay counter in Hong Kong and say this is my plan to fly to Hangzhou, then Beijing then Macau in 4 days. The nice lady at Cathay then feavourishly input my travel schedule and flight numbers into my ticket details, smiled and said “yes that’s fine”. It seemed a bit too easy. But it was easy, no tricky questions in Hangzhou, just completing a landing card - and likewise on departure from Beijing, a quick stamp in the passport and I was off. The whole process was so simple in fact, that I will not hesitate to visit Mainland China more often.

China is definitely welcoming to international tourists and investors. In Beijing 6 years ago, you struggled to find a street sign, or anyone that spoke English, even in a western hotel chain. Now, in the capital, every road sign or information board is (also) written in English – and many more people speak English.

Some things haven’t changed though; from my western hotel’s wifi network, there was no access to Google, BBC News, the FT, LinkedIn, or that bastion of misinformation - the Guernsey Evening Press. And that is one key difference with Hong Kong; in Hong Kong, you can search away to your heart’s content. It is strange learning to live without Google for a few days.

The Chinese economy and stock markets

China is the great example that capitalism that brings people out of poverty, not democracy. If you don’t believe me, look at India for the opposite picture.

It might seem slightly counter intuitive also that China would have a stock market with 5,160 stocks and a daily turnover of $158bn, second only to the US with about 5,400 stocks and $230bn in daily turnover. How can the CCP sit on such vibrant capital markets? I still do not really know the answer to this riddle, but those markets are real and the CCP knows that they are part of the reason for China’s modern growth and prosperity.

Pictured: the blue skies and the bold, shiny skyscrapers in Beijing’s CBD, Nov 2025

In truth though, it has been a pretty rough ride in the equity market for Chinese A share investors in the last 5 years – until September last year that is, when Xi announced some major reforms to stimulate demand. Beijing has a history of announcing measures and then not totally following through with them as enthusiastically as the market would like. But so far, the market is staying with Xi on this one and his re-embrace of Jack Ma and technology post the DeepSeek moment in February 2025.

You have to remember that China did not see the enormous government stimulus packages during Covid in the same way as the West. Much of the West is still feeding off that one off massive boost to personal balance sheets.

The enormity of China’s escape from poverty to middle class wealth can be seen in every shiny office block and shiny appartment block – on every perfectly build highway with shiny new cars, and a quiet city centre with clean air, electric cars and electric motorbikes.

But therein lies the problem. Just like when you cut the engines of a massive supertanker, because of its huge inertia and momentum it can take 10 kms to come to a stop, trying to light a fire under the enormous, but stalling Chinese economy is proving really tough, especially when the US is trying to rewrite the terms of trade.

Much of the younger generation in China’s middle class are stuck with negative equity from years of declining Chinese real estate prices. So any sign that household wealth is improving could be a leading indicator of brighter times ahead.

There is a saying in our industry that the value guys are always depressed – this is in part because they are actively seeking out beaten up companies, so the only people they speak to are pretty depressed themselves, just like their stock prices.

Signs of brighter times in China?

So I sat down with a value guy in Beijing; Mr Xia was depressed. But he did pull out the above chart, to show a glimmer of hope. The chart shows changes in Chinese househould net wealth. For the first time in 5 years, there is a noticeable uptick. This might be the effect of the major stock market bounce in 4Q’24. In any event, the last time we saw an improvement of this strength was 10 years ago.

Anyway, let’s hope this means good news for China and China A share investors. The strategy we invested in at Longqi Scientific is quant based and so it does not need markets to go up to make money. Let’s see how they fare. We will look to open that up to our private clients early next year if everything goes to plan.

Performance

(Please see performance disclaimers below)

You may remember last week we talked about Mr Burry of the “the Big Short” fame. Well, less than a week after he announced his $1bn bet against Nvidia and Palantir, partly causing the market volatility we have seen in the last 2 weeks, he decided to close down his hedge fund. He obviously did not take my advice to close out his shorts quickly. I suspect he received a very large margin call the next day, because Palantir was up c.10%. It seems that predicting disasters is not as easy as economic historians would have us believe, and making money from them is even harder.

In the meantime, our core strategies continue to perform well and there is a great opportunity to enter tech names at a meaningful discount to recent highs - err… thank you Mr Burry.

This week

This week, I am back in London and Guernsey with Cody Willard talking revolutionary tech at a particularly helpful time. I am looking forward to seeing many existing clients and friends of the firm. The schedule is fairly packed, but do reach out if you would like to see Cody.

Wherever you are this week, let me wish you a wonderful and prosperous week ahead.

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

“Reasons to feel confident about the health of the US financial system”, 17/11/25

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Investors concerned about risks to the financial system can find reassurance in the Federal Reserve’s November 2025 Financial Stability Report (FSR). The FSR—which assesses vulnerabilities across the financial system—laid out far more strong areas than weak ones. It also presents a financial system foundation that looks more durable than brittle. Among the areas flagged to monitor were increased demand for higher-risk assets, elevated gross leverage among publicly traded firms, rising auto and credit card delinquencies, and leverage within hedge funds and life insurers.

In the FSR’s survey of “novel uncertainties” that could deliver a systemic shock, the top three perceived risks increased since the last FSR, issued in April 2025. Policy uncertainty rose from 50% to 61%, geopolitical risks from 23% to 48%, and the risk of higher long-term rates from 9% to 43%. Inflation concerns remained steady near 40%. AI-related risks were cited by roughly 30% of respondents surveyed—still moderate but notably higher than the 9% in the April report. Importantly, the report’s discussion of AI is limited to its use in algorithmic trading, not addressing the economy-wide impacts of widespread AI adoption. The FSR’s overall takeaway seemed to be that AI’s use in trading is a trend to keep an eye on but not a big stability risk right now.

Despite elevated financial asset valuations, the perceived risk of asset prices declining, declined! Only 30% of respondents cited it as a major vulnerability, down from 36% in the April report.

More good news is that the types of shock-amplifying vulnerabilities seen in past financial system crises appear to be absent. The housing sector is not positioned for the kind of downturn observed during the Great Financial Crisis of 2008; nor do banks exhibit the balance-sheet vulnerabilities that preceded that crisis. Likewise, the conditions for disorderly selloffs in equities, bonds, and real estate are not in place. Banks’ capital positions remain sound, and household and business borrowing levels are broadly manageable relative to income. Liquidity strains are unlikely under current funding conditions.

While the November FSR found just a handful of reasons to worry, it is possible to put forward at least a dozen positive takes on financial stability in the Fed's four main risk categories:

- Why elevated asset prices won’t lead to outsized drops. The FSR says that asset prices are high, but the conditions that can turn a market drop into a bigger problem—like weak bank balance sheets, heavy borrowing, and funding strains—aren’t showing up right now. In other words, even if prices did fall, the financial system looks much better positioned to handle it than in past periods when stress spread quickly. The report says that trading conditions in both the stock and Treasury bond markets have improved compared with the volatility and liquidity strains seen in 2022 and early 2023. Credit markets also look calm, with borrowing costs for companies not showing signs of stress. While commercial real estate remains an area of close monitoring, the report notes signs that vacancy dynamics and rent growth patterns have begun to stabilize rather than deteriorate further.

- Why business and household borrowing won’t lead to distress. The FSR underscores that household and nonfinancial corporate leverage remains manageable. Debt-to-GDP ratios are stable and notably below the levels recorded in the mid-2000s. Most publicly traded firms demonstrate the capacity to service debt. On the household side, debt is concentrated among borrowers with higher credit scores under post-crisis underwriting standards, and mortgage delinquency rates remain historically low. Credit card debt balances have stabilized.

- Why financial sector leverage won’t strain banks. The banking system remains well capitalized. Regulatory capital ratios are near historically high levels, and the FSR emphasizes that banks are positioned to absorb sizable losses under unfavourable conditions. Supervisory stress test results continue to show that large banks could manage substantial credit, market, and trading losses while maintaining lending capacity.

- Why funding risks are low. Funding stress remains low across the system. Growth in government money market funds has supported stability in short-term funding markets, and the FSR reiterates that these funds make up the least fragile segment of the cash management universe. Banks maintain high levels of liquid assets, and reliance on uninsured deposits is historically low. This significantly reduces the likelihood of rapid deposit flight or disorderly funding withdrawals.

In any list of “things to worry about”, the health of the US financial system appears to be well down the pecking order.

Justin Oliver

“We have clues into the great mystery of AI ROI”, 17/11/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

Introduction

“Big picture, to drive a 10% return on our modeled AI investments through 2030 would require ~$650 billion of annual revenue into perpetuity, which is an astonishingly large number. But for context, that equates to 58bp of global GDP, or $34.72/month from every current iPhone user, or $180 month from every Netflix subscriber.” -- J.P. Morgan analysis from November 11, 2025

For most of the last three months, the big debate on Wall Street has been whether AI will generate sufficient profits to justify the unprecedented, multi-trillion-dollar investment in AI since the only three-year-old technology went mainstream (the ChatGPT moment was November 30, 2022). And that’s absolutely a fair question to ask. Especially when we get guys like Sam Altman scolding imaginary short sellers on podcasts instead of simply explaining how OpenAI, a company with just $13 billion in revenue, could pay for $1.4 trillion in compute commitments by 2030.

Those poor explanations recently combined with the sheer magnitude of the level of spending from the hyperscalers (roughly $400 billion next year) has led to a lot of analysis like that quoted above. Analysts at J.P. Morgan and their ilk think in spreadsheets, and for them to justify this outsized AI capex, they need rows and columns showing the revenue and profits that will come from this AI spending.

But unfortunately it’s not that easy, because the ROI from AI will not come solely from paid ChatGPT or Gemini subscriptions. And that’s actually a good thing. If there were an easy way to calculate total “AI revenues,” subtract expenses, show profits, and calculate the total ROI right now, I would actually be bearish.

AI is a fundamental paradigm shift in not just the world of computing, but the entire economy. If the calculations for how to quantify this Revolutionary paradigm shift could be done by a junior analyst sitting at a desk in J.P. Morgan’s new midtown monolith, that would probably make me doubt that this thing we’ve been calling a Revolution is actually a Revolution.

So we’re going to look at how the ultimately trillions of dollars spent on AI might actually generate returns. While ChatGPT+ subscriptions are certainly part of the equation, the AI paradigm shift is much bigger than that, which makes fully understanding the nature of this Revolution a bit of a mystery.

But we think the key to unlocking that mystery of AI lies in the story of the Cloud, a story that we were heavily invested in over the last 15 years and which generated great returns for us over time. Thus, in this article, we’re looking back at the build out of the public cloud to see what we can learn about how The AI Revolution will play out, and how the companies spending these hundreds of billions of dollars annually on AI can possibly hope to earn a return on their investment.

The Cloud Build Out

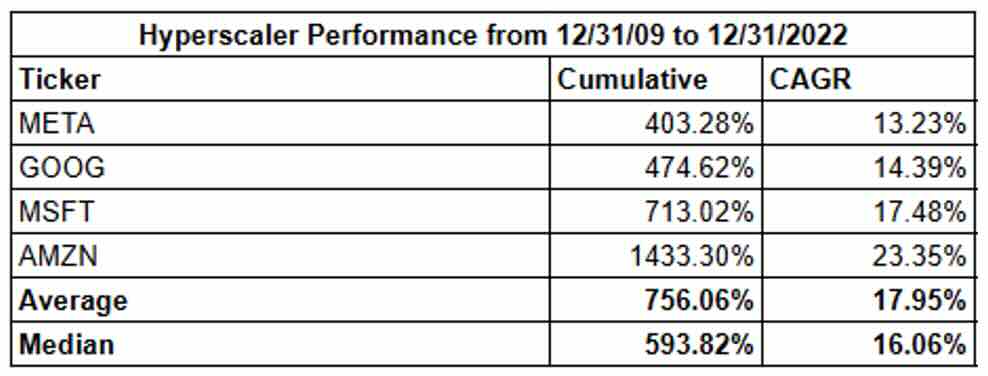

Amazon, Microsoft, Google, and Meta -- a.k.a. the “hyperscalers” -- spent somewhere between $500-$600 billion building their cloud infrastructure before the AI age started. Many criticized these companies for their heavy capex spending early on, making the same monetization arguments people today lob against AI spending. But looking back, it’s obvious that the clouds turned out to be genius investments for the hyperscalers.

However, the hyperscalers didn’t generate fantastic returns on their pre-AI cloud spending via direct subscriptions from end customers. Sure, Google made some money from Google Workspace subscriptions, and Amazon Web Services (AWS) made some money from iCloud storage (AWS is Apple’s primary cloud provider), but those are rounding errors compared to those companies’ overall cloud ROI. It would be insane to try and justify AWS capex based on $0.99/month iCloud storage subscriptions.

Clearly, the cloud represented something much more fundamental than a better way to save photos and documents. In our view, the “ROI” for the $500-600 billion in cloud investment came from four distinct sources:

- Efficiency gains from shared compute;

- Improved internal operations;

- Entirely new cloud-based business models; and

- Direct cloud subscriptions (those $0.99 iCloud subscriptions we mentioned).

We’ll discuss each in turn, and how we think The AI Revolution will somewhat mirror each component of the overall cloud ROI.

Rented vs. Owned Compute

First and foremost, AWS proved that sharing compute resources made a lot more sense than building and managing in-house IT infrastructure for most companies. Building servers, managing cybersecurity, hiring IT staff is inefficient for most businesses and it’s not part of their core competancies anyway, so it is better to outsource it. Moreover, a company rarely uses 100% of its in-house compute capacity 100% of the time, and the beauty of the cloud is that it offers elastic compute capabilities. You can spin up the servers you need, where you need them (geography is a big deal for latency), only when you need them. This saves AWS’s customers a pile of money and headache.

So in essence AWS and the public cloud presented a fundamentally more efficient way for the world to run compute workloads. You had a fixed asset (compute) which was underutilized because each company purchased and operated their own, and once those assets were shared (via AWS), utilization went up and overhead went down, driving revenue/profits for AWS and massive cost savings for the rest of the world.

The fundamental efficiencies of the cloud reshaped the entire software industry and led to the advent of Software as a Service (SaaS). Pretty much every legacy software company -- including titans like Microsoft and IBM -- were forced to switch to cloud-based subscription services because of the efficiency gains and instant distribution offered by the cloud.

In the early days of the cloud, who could have penciled in the fact that then 30-year-old Microsoft and 100-year-old IBM would fundamentally remake their entire businesses around the cloud? Not to mention, the shift to the cloud enabled a whole new crop of SaaS businesses which simply help their customers manage cloud workloads; think of companies like Snowflake (SNOW), CrowdStrike (CRWD), Cloudflare (NET), or MongoDB (MDB). And AI will be no different. In fact, there are already several AI startups (like Hugging Face) that exist simply to help you manage your AI.

But unlike the cloud, AI isn’t just a better way of computing, it represents a fundamentally more efficient way to perform cognitive work (and ultimately physical work too as robotics go mainstream). As Jensen Huang says, AI costs are now part of a company’s overall labor budget, not just the IT budget. If AI can do in seconds what took a human lawyer six hours, that’s a paradigm shift in efficiency. But this won’t necessarily show up as a simple line item on any one financial statement. AI’s productivity gains will show up in corporate profit margins over time, just like the efficiency gains of spreadsheets did in the 2000s.

These efficiency gains won’t just simply result in ChatGPT+ seats, because corporations will build their own AI tools, they will use open- and closed-source models, they will buy better AI software from incumbents like Salesforce, etc. That’s part of what makes AI’s efficiency gains so hard to model. But in the aggregate, if AI is orders of magnitude more efficient at cognitive work than humans, a good chunk of that value will accrue to the companies enabling AI, i.e. the hyperscalers (and chip makers like Nvidia (NVDA) and TSMC (TSM)).

Internal Improvements

Second, the cloud dramatically improved internal processes at the hyperscalers. The hyperscalers are simultaneously the largest sellers and buyers of compute in the world. These companies all run massive digital services (Google Search, Amazon, and Microsoft 365) that require a ton of compute to work properly.

What most people don’t recognize is that the growth of the externally-facing cloud businesses also drove growth and efficiencies for the hyperscalers’ core businesses. To serve millions of external developers, Amazon, Microsoft, and Google had to invent things like containerization, modern virtualization, automated deployment systems, global failover, and industrial-grade monitoring. By selling services to third-parties, the hyperscalers were forced to standardize, automate, and harden their digital services, and you can imagine how those techniques immensely improved the value of these companies' core products. Google Search is much better today than it was in 2010 in large part thanks to efficiencies that Google figured out running Google Cloud Platform (GCP).

Likewise, AI has and will continue to dramatically improve the services provided by the hyperscalers. Google and Meta have already shown remarkable growth in their advertising businesses using recommendation engines improved by GPU infrastructure. Microsoft built GitHub CoPilot which cut software development cycle time by over 55%. Amazon built Rufus which drives 60% higher conversion for customers that use it.

The moral of this story is that offering outside services to digital enterprises also helps the hyperscalers improve their own digital enterprises. There is a virtuous cycle that develops when these companies are forced to improve their cloud businesses in order to stay competitive with each other in a market with extremely sophisticated enterprise customers. We saw that with the cloud, and we’re already seeing it with AI.

While there is no easy way to quantify the improvement happening within the hyperscalers because of AI, we do know that their non-cloud revenue and profits have re-inflected in dramatic fashion since they started integrating AI into everything they do. This is the proof of the value of the AI pudding for the hyperscalers themselves. But we don’t know precisely how much of the capex goes toward supporting internal workloads, so there is no easy way to draw a direct line between AI spend and improving metrics for say, Google Search, for example. Again, showing why modeling AI ROI is so hard for Wall Street analysts.

Revolutionary New Businesses

This is arguably the largest bucket of the AI ROI that will be almost impossible to model. The cloud enabled entirely new Revolutionary businesses (several of which we have also owned over the years), like Robinhood (HOOD), Netflix (NFLX) (enabling the switch from DVDs to streaming), Spotify (SPOT), Shopify (SHOP), and AirBnB (ABNB) to name a few. These companies were able to build Revolutionary product categories on top of scaleable, reliable, and relatively cheap public cloud infrastructure. Critically, what enabled these companies to scale was not just the cost advantages of the cloud, but also the ability for instant global distribution to billions of people.

Almost no one in the early days of AWS could have predicted the plethora of new businesses that would be built on public cloud infrastructure and how that would drive massive ROI for Amazon. I also guarantee that no Wall Street analysts had a line in their model for “Revolutionary New Cloud-Enabled Product Categories.” It would have been impossible in the year 2008 to model the economic value created by the millions of successful cloud-based companies over the next seventeen years. Indeed, the entire Apple App Store and all of Apple’s services revenue would not really exist like it does today were it not for the public cloud underlying nearly the entire ecosystem.

Even though we are in the early days of the AI Revolution, there are already numerous new business models popping up that could not have been predicted even three years ago:

Replit built Agent 3 that builds full-stack, operable software with text prompts.

World Model built Marble which turns any picture, video or text prompt into a 3D, AI-generated model which you can explore (this was just released this week and it’s pretty amazing).

ElevenLabs’ builds AI voice and cloning tools and recently crossed $200 million in annual recurring revenue (ARR).

In just a couple years, AI will enable truly autonomous robotics, including humanoids and self-driving cars, and that alone unlocks two more multi-trillion dollar annual TAMs. In ten years, we’ll look around and there will be dozens of publicly traded AI-native companies with business models that we simply cannot imagine today.

Direct Monetization

The last and arguably smallest portion of the AI revenue pie is actually the most obvious, and this is where Wall Street spends most of its analysis time: direct AI subscription revenue. If you want to see models for what this revenue might look like, there are plenty you can find, and so we won’t spend too much time here.

OpenAI and Anthropic will generate a combined $24 billion in revenue this year, actually not bad for businesses that were basically at $0 in ARR three years ago. Cursor, the popular AI coding tool, announced last week that it is now over $1 billion in ARR with only 300 employees. Replit, had $150 million in ARR in September, up 50x year over year. Of course these companies represent just a small fraction of the observable AI universe and there is no good way to paint a complete picture of current “AI revenue,” but this gives us a flavor of what direct monetization looks like in these early days.

While still relatively small compared to the overall AI spend, the direct monetization path is growing much faster than it did in prior Revolutions. Both in terms of users and dollars, AI scaled from zero to one billion quicker than any technology in history. As ChatGPT, Gemini, Meta AI, Sora, and Claude continue to gain eyeballs and screen time, they will eventually add more monetization paths including more paid subscriptions, advertisements, and revenue share from product placement. This won’t be the sole source of AI ROI as we’ve discussed, but it doesn’t have to be. Direct monetization is basically the cherry on top of the AI ROI cake.

Conclusion

There’s one thing that’s always true about Revolutions, whether political or technological, they are messy, not clean. Wall Street doesn’t like that. The ROI for AI doesn’t fit neatly on an Excel spreadsheet, nor did the cloud. And AI, like the cloud, will only be obvious in hindsight. And we think that AI, like the cloud, will be very profitable for the hyperscalers.

The primary risk is that the hyperscalers overshoot their investments and get ahead of the ultimate demand for AI services. That’s a very real possibility and one we take seriously.

Further, there are also notable differences between The Cloud Revolution and The AI Revolution, most notably the costs of the servers, the use of debt to finance some of the buildout, and the fact that this is a whole new way of doing computing. Moreover, Amazon started AWS with compute it had lying around, not by purchasing billions of dollars of chips and building greenfield data centers. Nevertheless, we are aware of these risks, and in the long run if AI works out like we think it will, any over shoot in the near term will be a small speed bump along the way.

Moreover, we’re not saying that every single AI startup will turn into a viable business, in fact, we’re sure most won’t. But we are not investing in OpenAI, and every other AI startup. What we are doing is investing in the hyperscalers -- the primary companies enabling this Revolution -- and a few of the other publicly traded companies that are benefiting from and/or driving this Revolution. We know that we are not smart enough to predict all the ways that the stocks in our portfolio will generate returns from AI, but we know they will.

How can we be so sure that AI will work out somewhat like the Cloud? Because AI is fundamentally more efficient than human labor in many instances, just like the cloud was fundamentally more efficient than what came before it. Sure, a GPU might be more expensive than a CPU, but CPUs were also more expensive than abacuses. Cars were more expensive than horses. Trains and railroad tracks were more expensive than wagons and dirt roads. The aqueducts were more expensive than buckets.

GPU-powered AI is a paradigm shift compared to traditional computing. Both the costs and the outputs are orders of magnitude apart. And it’s ludicrous to compare the costs of the next paradigm to the output of the last paradigm. But that’s Wall Street’s way of doing math, and it’s why they almost never see Revolutions until after they’ve already happened.

In conclusion, we’re not making a blind bet on all things “AI,” but we are following the same playbook we followed with prior Revolutions, like The Cloud Revolution. We think Wall Street’s dogmatic, narrow view of The AI Revolution misses the forest for the trees. But therein lies the opportunity, because if it was obvious exactly how we were going get a return on all this AI spending, then everything would be priced to perfection and we wouldn’t be able to generate excess returns going forward.

Just consider this: the hyperscalers spent over half a trillion on capex from 2010-2022, and their stocks went up an average of almost 18% per year over that time. By 2028, they will be spending that same amount on AI every year. AI is more than an order of magnitude more spending than the traditional cloud, and if AI really is the economic paradigm shift we fully think that it is, the potential gains for the hyperscalers will be much larger.

Cody Willard & Bryce Smith

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 16/11/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 16/11/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.