.jpg)

Weekly Newsletter

Freedom Calls: 16/2/26, The end of an era for Schroders … and Happy Chinese Lunar New Year!

by

The Team at Freedom Asset Management

February 16, 2026

12 Minutes

Freedom Calls: 16/2/26, "The end of an era for Schroders … and Happy Chinese Lunar New Year!"

From the team at Freedom Asset Management

It is always a sad day when a storied family firm decides to throw in the towel and take the cash. But so it was last week in London with the surviving lineage of the Schroders family ending their 211-year ownership of the eponymous firm. They sold out to the large American institution - Nuveen. For those of us who worked there (for me 2007-2010), it was a magical place - essentially an unofficial offshoot of the Royal family; it was not unusual to pass Prince Philip, the Duke of Edinburgh, in the lift on your way to a meeting - and who else would you call upon to open your new London HQ in 2018 but Queen Elizabeth II - of course you would!

Pictured: (L) the famous Schroders cufflinks, and (R) The late Queen Elizabeth II is joined by the late Bruno Schroder (L) for the opening of Schroders' London office in 2018 - picture credit: The Financial Times.

One of my memories of working there were the cufflinks (above) that we gave to our most important clients - these stainless-steel cufflinks, which probably cost about $10 to make, were much sought after by clients, and worn with pride by people who had everything, because they enjoyed being associated with the magic of Schroders and all that it represented. That would not have worked with any other firm. I still have mine.

There have been many obituaries written about Schroders over the last few days, mainly lamenting London's decline, but ultimately Schroders came unstuck because the surviving family members (after Bruno passed away in 2019) had little interest in the business. Bruno Schroder was not only a wonderful figurehead for the business, but he also knew exactly what was going on - in 2009, when I brought in a $6bn mandate, he was straight on the phone… and flew his private plane to the other side of Europe to be the guest of honour at the party I organised afterwards! True class.

It seems difficult to imagine that clients of Schroders private bank will find quite the same cachet at being owned by a US institutional asset manager, especially one that is largely unknown in Europe. After the sale concludes, I suspect some private clients will be looking more critically at their performance numbers, fees and overall service levels, rather than enjoying the mince pies at Fortnum and Masons. Sadly, it is the end of an era.

Freedom awarded Private Wealth Manager of the Year in the UAE and Hong Kong by Pan Finance

We are obviously a little newer at this game than Schroders, but we are grateful to the people at Pan Finance for above award. We know that what we offer and what we do is different and it is obviously lovely to see that other people agree! What matters most to us is that our clients and investors receive world class performance and global insight from a team that is passionate about delivering for our clients.

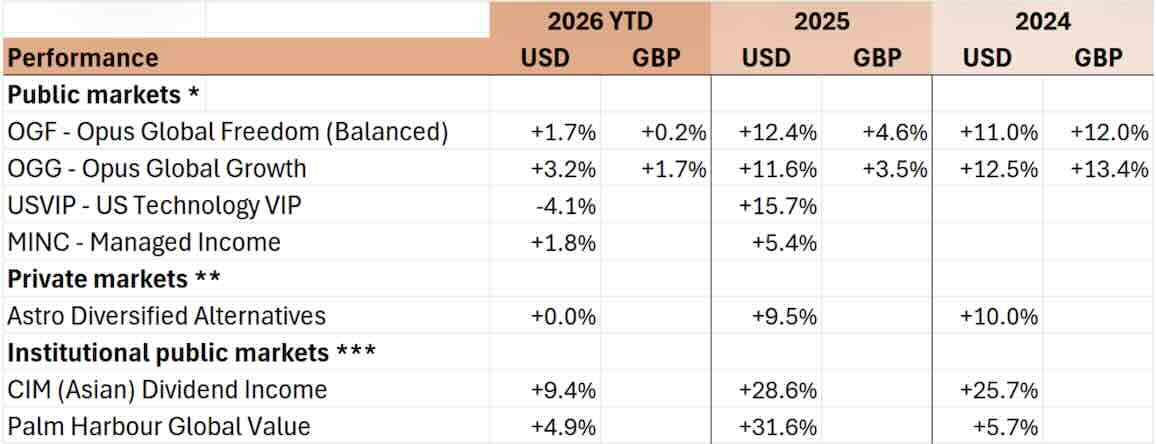

Performance

It was another lively week in US equity markets as we saw the latest innovations in AI bring some turbulence to more traditional sectors like wealth management (interestingly), real estate and logistics. The S&P500 is now flat on the year. The balanced and growth strategies have both done well from their exposure to Asia and emerging markets.

As you know, we like periodic volatility because it allows helpful entry points for top-ups and for new investors on a longer term investment journey - that is especially true of our tech strategy (USVIP). It is worth noting that USVIP has outperformed many of the Mag 7 greats, e.g. Microsoft (-17% YTD), Amazon (-13% YTD) and Apple (-6% YTD) - see below. Investors in our USVIP strategy will remember from last year that whilst it can get worse before it gets better, when it comes back, it does so at great speed and to great effect.

(For performance disclaimer see foot of email)

Our fund analyst team in Abu Dhabi are reviewing the commodities sector and we are looking at making an allocation there for our balanced fund in the coming weeks. After the recent volatility in the price of precious metals, there seem to be good opportunities in the broader commodity space - including oil and gas names. More on that soon.

Our articles this week:

This week we have:

Ramon Eyck - (Investment Committee member on Opus Global Freedom and Managed Income) - just back from Australia, writes about "Winter Sun and Rates rises Down Under”.

Canaccord's Justin Oliver - Adviser to the Opus Global Growth Fund tells us that "China gets serious about ending its property crisis"

10,000 Days' Cody Willard and Bryce Smith - Advisers to the US Technology VIP Fund write this week about the "The Fog of the Great AI War". Bryce is a military historian (amongst many other talents) and in this piece he frames the winners and the losers in the AI war using his examples in strategy from WWII.

Calendar notes

This coming week we have Chinese Lunar New Year for our friends in Asia. Please note Chinese stock markets are closed from Monday 16th - Tuesday 24th February. Hong Kong has a half-day Monday and will be back open on Friday 20th. We say goodbye to the "Year of the Snake" and welcome the "Year of the Horse"! Our Hong Kong office will be closed Tuesday-Thursday this week.

For our friends in the Muslim world, the holy month of Ramadan starts around Thursday 19th February. This means shorter working hours for our Muslim colleagues, but the office in Abu Dhabi remains very much open for business.

This week I shall be based in Guernsey and London (and definitely not for the weather!). Next week, I shall be back in Hong Kong and then onto Japan to see what everyone is talking about - so expect a note on Japan in a couple of weeks.

Wherever you are this week, please let me wish you a safe and wonderful week ahead,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

—————————————————

"Winter Sun and Rates Down Under", 16/2/26

By Ramon Eyck - Investment Committee member to Opus Global Freedom and Managed Income

With Christmas and New Year festivities in the rear vision mirror, this year I decided to slip my Aussie passport in my back pocket and escape down under for some January sun. While mainly a holiday, the joy of Freedom is that we have clients dotted around the globe so I was able to catch up with several of our investors and a number of industry colleagues along the way. Every trip is an opportunity to observe and learn, as well as to relax!

One thing that always strikes me when I return home is my compatriots’ invariably independent and unique perspective on the world. Sometimes that feels a little blinkered, but mostly it’s a function of distance, which continues to exist despite all our advances in technology and communications. Australia is obviously highly integrated into the global economy and a keen participant in multi-national organisations, but the people continue to maintain a healthy focus on the “here and now”.

During my time in Australia there were three events dominating the national discussion: (1) the Australian Open tennis, (2) the upcoming visit of the Israeli Prime Minister, and (3) the first increase in interest rates in the current cycle.

My knowledge of tennis is limited, but while the main talking points from the first part of the tournament seemed to be the weather (topping 40C on centre court), the men’s and women’s finals ultimately produced entertaining matches with tantalizing narratives about generational change.

The visit to Australia of Israeli PM Isaac Herzog to commemorate the Bondi massacre was arranged with good intentions, but ultimately produced sharp divisions across parts of society. Overwhelmingly, however, the sense I got from most people was a desire for it to be over so that the process of healing can continue without the political noise.

The interest rate rise (from 3.60% to 3.85%) is, however, the most globally noteworthy event: firstly, because it reiterates the “desynchronization” of global interest rate policy; and secondly, because of the political reaction to the shift.

While the US looks set to remain on a rate cutting path under Fed Chair nominee Kevin Warsh, several other G10 central banks have either come to the end of their rate cutting cycle (such as the ECB) or have started the process of raising rates (initially the BOJ and now the RBA). This shift in central bank policy is significant because: a) it is in response to a re-emergence of inflationary pressures, which are at least in part reflective of global pressures, and b) because growing rate divergence is likely to put downward pressure on the US dollar. Both factors remain important considerations in the management of our funds.

The second important observation was in relation to the public and political reaction to the change. To an older generation that experienced 17% mortgage rates (ie. my mother), a 0.25% rate rise seems insignificant, but with an annual-income-to-house-price ratio of 10-15x in Australia’s major cities, this increase will hurt a lot of people, particularly if it continues to climb.

The rate rise was in response to a surge in inflation (to 3.80% and forecasted to peak at 4.20% in 2026) and the RBA governor tied herself in knots trying to avoid connecting this to record government spending (which is expected to hit 26.9% of the economy in 2026). The fact that even the shambolic opposition Liberal party was able to land a few punches on the Treasurer emphasized how sensitive this issue is. With several central banks across the globe likely to follow suit in the next 12 months, politicians will be nervously following the fall-out.

So, while Australia might be a long way away and do its best to march to the beat of its own drum, events there are still pertinent to what is happening in other parts of the globe. Interest rate policy, like the seasons, moves in cycles and while those of us in Europe may not welcome rising interest rates, I’m sure we will all be looking forward to a bit of Aussie sunshine replacing our winter gloom!

Ramon Eyck

—————————————————

"China gets serious about ending its property crisis", 16/2/26

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Developments a few days ago could be remembered as the point that China finally got serious about ending its giant property crisis. But it is more likely to be the beginning of the end, rather than a defining moment.

China’s reckoning was 20 years in the making. Developers built across Asia’s biggest economy at extraordinary speed, fuelled by urbanisation and easy credit. Things then hit a wall in 2020 amid the Covid-19 pandemic. As giant projects stopped, demand cratered, prices plunged and developers were left with mountains of debt and 80 million surplus homes. The glacial response by President Xi Jinping’s Communist Party has left China with deflation and fending off talk of a Japan-like lost decade. This context explains why the recent news that China is launching a new effort to stabilize the market could be a significant development.

What is the new plan and will it succeed?

The pilot program targeting three large Shanghai districts aims to reduce the massive inventory of unsold homes using a “trade-in” mechanism. Residents of Pudong, Jing'an, and Xuhui will be able to sell their old homes to state-owned enterprises. The proceeds can be used to buy new homes, while the old homes will be converted into affordable rental housing units. If implemented properly, the impact would be threefold:

One, it would stabilize prices and enable developers to get back to work at idle construction sites.

Two, it would help younger Chinese priced out of the housing market access more affordable rental options closer to urban areas where the jobs are located.

Three, it would revive consumer demand, given that 70% of household assets are tied up in real estate.

There are many reasons why these efforts may not succeed. One is the lack of clarity on the scale of the effort, or a specific timetable. There is also the question about why it is just the Shanghai area which is being targeted. Why not implement the trade-in scheme nationwide?

In a February 5 report, Morgan Stanley described it as a symbolic gesture with limited potential impact. The investment bank worries that, if implemented poorly, the plan could exacerbate the problem of excess housing supply in the long run. Also, since new-home prices are markedly higher in Shanghai and other core urban areas than prices for older trade-ins, overly leveraged homeowners might become even more so.

Still, as Edward Chan at S&P Global Ratings explains, purchasing secondary homes could “provide liquidity to existing homeowners. If those homeowners use such proceeds to buy primary homes, that will also help destock excess housing inventory. In our view, elevated housing supply is a major factor hindering China’s property market recovery.” Chan additionally argues that the more success Xi’s party has in increasing the “availability of social rental housing for those in need,” the better the odds of increasing household confidence. This is vital to mobilizing China’s 1.4 billion people to deploy their $22 trillion in savings to support Beijing’s ability to grow the economy at close to 5% a year.

Morgan Stanley’s Robin Xing thinks it’s time for massive mortgage subsidies to revive the housing sector. He estimates that roughly $57 billion of subsidies will be required per year to “stabilize expectations.” Without them, Xing worries that the property sector might not bottom out until 2027—or maybe even later than that. Along with lower mortgage rates, economists think Team Xi should consider reducing downpayment thresholds and reducing transaction fees for homebuyers. Land-use reforms are also needed to enable rural land to be traded more like urban land, thereby increasing supply and lowering prices.

The timing of Xi’s housing plan seems connected to the other big news in China over the last couple of weeks: Xi’s push to position the yuan as the reserve currency of choice.

Xi has been trying to internationalize the yuan since at least 2016, the year it was included in the International Monetary Fund’s “special drawing rights” basket along with the dollar, euro, yen, and pound. It’s been a slow grind, though. Ten years on, the yuan accounts for just 2% of foreign-exchange reserves compared with 57% for the dollar and 20% for the euro. On January 31, Qiushi magazine, the Communist Party’s flagship journal, reported on a speech Xi delivered behind closed doors in 2024. Xi declared that China needs a “powerful currency” that’s “widely used in international trade, investment and foreign exchange markets, holding the status of a global reserve currency.” While the comments sound dated, the timing of the report, and its publication in the Politburo's chosen vehicle for announcing high-level policy shifts,, caught the attention of financial markets.

To many Sinologists, this effort suggests that Team Xi sees an opportunity, as President Donald Trump’s tariffs and attacks on the Federal Reserve have prompted many global funds to question the stability of dollar assets and whether the White House even wants to preserve that stability given Trump’s stated desire for a weaker dollar. “Policymakers could think that it’s … good timing right now because financial institutions have a strong consensus that the dollar is weakening,” argues Xing Zhaopeng at Australia & New Zealand Banking Group.

Ending China’s property crisis once and for all is a prerequisite to upping global trust in the yuan and its use in trade and finance. But myriad other needed reforms would bolster the case for the yuan too: scrapping strict capital controls, making the yuan fully convertible, increasing transparency, building globally trusted payment systems, strengthening institutional frameworks, creating a globally respected credit rating industry, and making the People’s Bank of China (PBOC) independent. So far, Xi’s reform team has prioritized increasing access to Chinese government bonds and stocks over the supply-side upgrades needed to increase global trust in China’s financial system.

The PBOC issue is particularly important given China’s deflationary pressures (consumer price inflation was essentially 0.0% in 2025). Xi’s broader priorities have constrained PBOC Governor Pan Gongsheng’s ability to increase liquidity to help alleviate the deflationary pressures. For those purposes, a weaker yuan would be more beneficial. Yet a weaker yuan might increase the odds that giant developers default on offshore debt. A lower exchange rate could prompt Trump to impose ever higher tariffs on China. In short, the liquidity that China needs to fight deflation would work at cross-purposes with Xi’s “strong yuan” mission to achieve reserve-currency status.

Still, the optics of deflation and persistent manufacturing overcapacity do little to bolster China’s position, hence Xi’s renewed push to stabilize the property crisis. The problem is that far more aggressive policy measures are needed to avoid a lost decade of slow growth, akin to that experienced by Japan in the late 1990s through the early 2010s. Possible responses include: a bolder effort to reduce housing inventories across China’s 22 provinces, more aggressive state-led purchase programs, lower mortgage rates to increase affordability, moving away from the old high-leverage model of housing purchases, building a bigger social safety net to prod consumers to save less and spend more, and repairing local government balance sheets.

Ultimately, while Xi’s Shanghai plan sounds promising, much more is needed. The drip, drip, drip response echoes Japan-like efforts to paper over financial cracks. In a December report, Federal Reserve Bank of Dallas economists Scott Davis and Brendan Kelly found that in 2024, about 40% of China’s bank loans to the real estate sector were made to companies with operating profits insufficient to cover interest obligations versus 6% in 2018. “There’s mounting evidence of ‘zombie lending’ in China—banks rolling over bad loans to unprofitable firms and allowing the status quo to continue rather than recognize losses.” In many ways, they argue, “the current experience in China mirrors that of Japan in the 1980s and 1990s. Rapid growth in private sector debt—also fuelled by domestic savings—was followed by the appearance of zombie lending. In Japan, that zombie lending led to the inefficient allocation of capital and decreased productivity, especially in sectors shielded from foreign competition.”

Xi’s Shanghai pilot program is a promising start––and a welcome sign of renewed urgency. But moving a $19 trillion economy beyond a giant real estate slump now in its fifth year will require a far more assertive policy response. Without it, Xi’s reserve currency ambitions may suffer, too.

Justin Oliver

—————————————

"The Fog of the Great AI War", 16/2/26

By 10,000 Days' Cody Willard and Bryce Smith - Advisers to US Technology VIP Fund

"War is the realm of uncertainty…" – Carl von Clausewitz

Bryce here. We have entered what I’m calling “The Great AI War.” AI has launched an attack on the software industry, but now the market is recognizing that the threat of AI is even larger. This week, certain stocks in non-tech sectors like real estate, finance, and logistics saw massive (20%+) drawdowns because of AI disruption fears.

Pictured: British and French troops “fighting” the Phoney War in France, 1939

What’s interesting is that nothing has really changed in the fundamentals, but the uncertainty surrounding the tech industry – and now the broader economy – is through the roof. This reminds me of the “Phoney War” stage of WWII (late 1939 to early 1940) after Germany invaded Poland, when France and Britain declared war, but there was essentially no fighting on the Western front. Then, like now, uncertainty was high, and Germany (sort of like AI) looked like an unstoppable force that could topple any established nation (or company).

While the market is rightly uncertain about the future with AI in the mix, I don’t think it’s framing AI in the right way at the moment.

Many people are worried that AI can just do anything in the digital world, and that once it can do that, there will be no need for software or any other digital services.

But one thing the market is fundamentally misunderstanding at this moment is that AI is just a technology. It is not a company, an app, or some mystical sentient force (at least not yet). Critically, AI is a weapon available to every company, tech and non-tech alike.

In other words, it’s an equal-opportunity disruptor. Virtually every company has access to the leading-edge models at relatively low cost via APIs. Just like the tank or the airplane in WWII, most players had access to the same core technologies that would shape the conflict. The differentiating factor came from how the belligerents produced, integrated, and applied those tools. The same will be true of AI.

Moreover, if the models themselves were truly capable of doing anything and everything, then the AI developers (OpenAI, Anthropic, x.AI, and Google) would NEVER license them to the public via APIs. The AI developers monetize their services primarily by integrating models into applications, and their apps would be equally at risk of being disrupted if the AI could just replicate any app with a single prompt. This illustrates that the models themselves are useless without a form factor. What matters is how AI is applied and integrated into the software we use.

So "The Great AI War" will be decided largely by how individual companies integrate and deploy AI. With that in mind – sticking with our WWII analogy – we can roughly divide the business world into the following categories:

The "Standard Oils"

These are the companies selling the key enabling ingredients required to produce AI. They benefit regardless of who wins The Great AI War. Here, only TSMC and Nvidia fall into this category. Despite all of the hand-wringing about ASICs and competition, Nvidia is still the king and its lead is expanding with the move to rack-scale systems. And of course, nearly every advanced AI chip on Earth is manufactured by TSMC.

The "Arms Dealers"

Every company on Earth will want to buy" weapons" (AI) for this war, and the companies peddling those weapons will clearly benefit, again, regardless of who wins The Great AI War. The hyperscalers are the only ones that can actually build the infrastructure which produces the AI, as they are the only ones with the capital (hundreds of billions of dollars) required to build the level of infrastructure required to satisfy the demand for AI services. Amazon, Google, and CoreWeave are direct beneficiaries of the arms race by the belligerents of The Great AI War. Microsoft is both a belligerent and an arms dealer, and it has to defend its legacy Windows/Office ecosystem, making it less of a pure play.

The Defenseless

Despite a valiant effort, Poland lost to Germany when it found itself fighting panzers with cavalry. Soon, we will see a lot of legacy services companies finding themselves completely ill-equipped to fight the coming AI onslaught. This week, we saw the sellers come for “old-world” sectors like finance, real estate, and logistics. These companies will quickly find their perceived “defenses” – like their large customer bases and decades-long relationships – wholly inadequate to defeat AI. If AI applications can provide a better version of your service at 1/100th the cost, you won’t stand a chance.

The Anachronists

In 1940, France looked fully, if not more militarily capable, than Nazi Germany. However, the country was quickly overrun by Germany’s modern tactics – i.e. Blitzkrieg – which overwhelmed the Allies’ superior numbers. France was fighting the last war, and one of the factors why they lost to Germany was because they did not adapt to modern technology and tactics fast enough.

There are a lot of tech companies that appear well-positioned to benefit with AI, but if they don’t integrate it quickly enough, they too will find themselves overtaken by faster-moving rivals. Unfortunately, it’s difficult to identify which seemingly well-positioned companies are integrating AI well or poorly until after the fact. Again, France looked well-prepared to fight Germany until it didn’t. In this category, I’d put a lot of the old, behemoth, legacy software firms like IBM, SAP, Oracle, and Microsoft (with respect to its Windows/Office products). I simply doubt that they can move fast enough to keep up with their AI-native competitors.

The Disrupters

Germany’s modern military and lightning war tactics looked unstoppable in the early innings of the war. Likewise, AI is being treated as an unstoppable force that can demolish any sector or industry with a prompt. The early rounds of The Great AI War clearly go to the AI developers – OpenAI, Anthropic, and Google – who have built some of the most Revolutionary applications ever created.

But going forward, winning The Great AI War will take more than just innovation. Just like in WWII, the winners won because of their scale, distribution, and logistical advantages. America and Russia produced mostly inferior equipment compared to Germany, but they did so at a ratio of roughly 4:1, and that was enough to turn the tide of the war.

Going forward, I think the winners of The Great AI War will be the companies that best integrate and distribute AI at scale. I think Google and Meta are well positioned here, as they are already integrating AI in amazing ways into their existing product suites with billions of users.

And Apple resembles America in WWII: a sleeping giant with untapped potential but which is thus far uninterested in fighting the war. But we are also making some selective bets on the software companies we think will fall within the disrupters category, like Zscaler, Snowflake, and Synopsys.

The Adopters

Companies that operate mostly in the physical world are neutral beneficiaries of The Great AI War. They are the Switzerlands of this battle, if you will. Companies like Coca-Cola, Caterpillar, and McDonald’s will just adopt the winning software/services/apps that come out of The Great AI War.

Conclusion

Those who adopt, integrate, and distribute AI the best will be the winners of The Great AI War.

The level of uncertainty right now is understandable given that we know big things are about to happen, but we don’t know who the ultimate winners and losers will be. But keep in mind, as the war starts to play out over the coming quarters, we will start to see which category companies fall into fairly quickly. As this happens, we will see stocks rerate very quickly, and there will be a lot of money to be made for those who correctly picked the winners and losers.

Sitting here at the beginning of the war, the clearest bets are on the Standard Oils (NVDA and TSMC) and "arms dealers" (GOOG, AMZN, and CRWV), and we are willing to stick our necks out on the few software companies we mentioned earlier.

That said, we will continue to monitor all of the relevant players and we will likely move decisively when we find companies that we think will come out on the winning side of this war. This war will be decided by the execution of the individual companies more than anything else, and that means being an active, disciplined investor is more important than ever.

Cody Willard and Bryce Smith

—————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 15/2/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 estimate takes the MCAS December 2025 estimate and deducts the estimated charges of the Astro feeder fund. *** Morningstar as at 15/2/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2026 Freedom Asset Management Limited.