.jpg)

Weekly Newsletter

Freedom Calls: 15/12/25, A weekend in Saigon and 40,000 finance professionals speaks volumes for Abu Dhabi's success

by

From the team at Freedom Asset Management

December 15, 2025

7 Minutes

Freedom Calls: 15/12/25, "A weekend in Saigon and 40,000 finance professionals speaks volumes for Abu Dhabi's success"

From the team at Freedom Asset Management

A weekend in Saigon (Ho Chi Minh City)

There is a still a lot of Asia that I have not visited, so when a long time friend of the firm suggested on Wednesday that we take the 2.5 hour hop with Cathay to Saigon for the weekend, I did not need much encouragement. In a city with 9.5m (mainly young) people, there is something for everyone and all budgets in Saigon: history, culture, restaurants and a vibrant nightlife. The one thing I would definitely leave to the locals would be the driving, where it seems only a cursory glance of the Highway Code is enough to get your driving license; the 169 near misses I witnessed on my way from the airport makes Cairo drivers look positively thoughtful and reflective, and Dubai taxi drivers part of a military procession. Despite the fact that my 48 hour trip was shortened by 2 hours standing in immigration lines (1 hour each way), I highly recommend a visit.

No trip to Saigon would be complete without a visit to the curiously titled "War Remnants Museum". Looking at the exhibitions, it is a timely reminder that it is the victors who write the history books. But history does soften, otherwise it presents modern day challenges in economics and geopolitics.

Pictured: A preserved CH-47 Chinook in the War Remnants Museum, Saigon, Dec 2025

Whilst communism won the day in 1975, it is JP Morgan's logo which towers over Saigon today - and the Mandarin Oriental will soon join the clutch of luxury hotel chains that sit next to Gucci, Rolex and other high end stores (see below). Proof if ever it was needed that capitalism always wins in the end (perhaps Mr Mamdami might like to pay a visit).

Everybody wants to be friends with the USA (and capitalism)

In geopolitics, we are all friends now in Vietnam. Because the alternative is that they become a vassal state of China. And as much as China and Vietnam are spiritually aligned at the political level, the Vietnamese do not want to controlled by Beijing. So there has been a concerted effort to reach out to the USA, Korea, Japan and other nations, e.g. all British passports holders can now enter on business or leisure visa-free for 45 days. International tourism and business are strongly encouraged.

In this context, the aforementioned "War Remnants Museum" has now rebranded itself as a tribute to peace - and counts many Americans as visitors.

Like all good "communist" countries, the leadership have realised that the only way to stay in power is to allow capitalism to work its magic and lift the living standards of its population.

Which brings me to China. I sat down with other friends of the firm in Hong Kong last week to listen to their current read on China.

Much is being made in the western press of China's $1tr trade surplus with the world, reached in only 11 months this year. Surely the riches of this trade surplus should allow the Chinese government to provide much needed stimulus to their economy? Well not so, according to our friends, for two reasons:

Chinese regional governments funded their budgets with land sales - the Chinese real estate sector is not in good health, as has widely been reported, therefore they are not finding it easy to sell that land, and

Those significant export numbers are being made with massive subsidies to those industries to keep the factories running - apparently 40% of Chinese car maker BYD's profits come directly from government subsidies.

So although the Chinese government would like to stimulate demand, they apparently do not have the money to do so. Hence the need to embrace the stockmarket and our capitalist friends. This is part of the reason why, as domestic interest rates have fallen, China has given the green light to domestic insurance companies to buy more Chinese equities to meet their insurance policy yield targets, and in consequence there has been sustained buying of high yielding "H" shares (Hong Kong listings of Chinese stocks) via the southbound connect. So despite an insipid economic environment in China, all of these things support our favourite allocation to Asia - the CIM Dividend Income fund, which has traditionally had about 50% of the portfolio invested in "H" shares.

Final thought on China - we asked our friends about who will win in AI - there is a belief that although DeepSeek was first, it is the mega caps including Tencent that are probably going to emerge as the winners, because they have access to far greater resources to keep scaling the improvements that the technology requires.

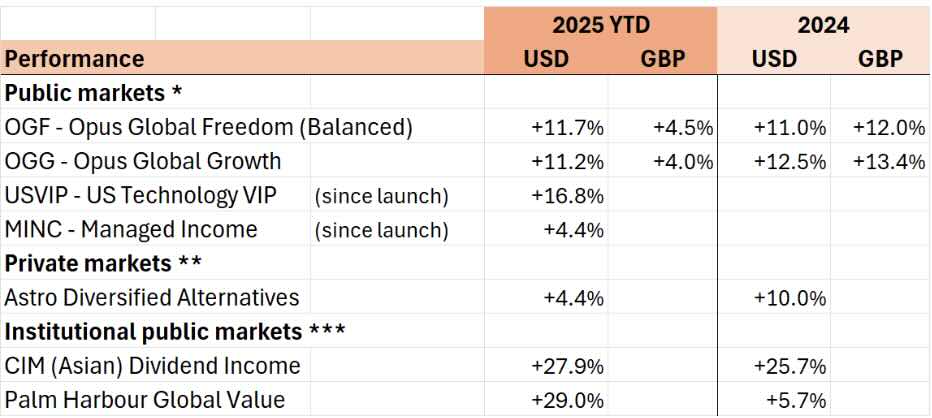

Performance - all good

(Please see performance disclaimers at the foot of this email)

We are in the closing run for the year - which is a time when market volumes are traditionally lighter, but hopefully also the news flow is easier. The Fed rate cut came through last week, which was by then heavily expected. What was less expected was the narrative around the next Fed cut, which Fed Chair Jerome Powell seems to be talking down.

In USVIP, Elon's talk of a possible SpaceX IPO at a $1.5tr valuation, put the wind behind Echostar's sails and that stock was up 30% on the week. As you may remember this is the most pure-play public market reference stock for SpaceX. This move now makes Echostar the 4th largest position in USVIP.

Thank you to everyone who joined us on the USVIP webinar last week. Recordings will be available on request in the next couple of days.

This week's articles:

Sandrine Reynaud gives us a round up of last week's "Abu Dhabi Finance Week" - the region's biggest, boldest and most beautiful finance event

Canaccord's Justin Oliver tells us that reports of the US dollar's demise as a reserve currency are somewhat exaggerated at this point

I shall be in Hong Kong and London this week, before settling in Guernsey for the Christmas period.

Wherever you are this week, please let me wish you a wonderful week ahead,

Adrian

p.s. only 10 days left until Christmas!

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

————————————

"Abu Dhabi Finance Week": 40,000 finance professional speaks volumes for Abu Dhabi's success", 15/12/25

By Sandrine Reynaud, Co-Founder and Senior Executive Officer at Freedom Asset Management (Middle East) Limited

With 40,000 professionals annouced over 4 days it was always going to be an action packed week. This year, Abu Dhabi Finance Week (ADFW) 2025, was held under the theme "Engineering the Capital Network," focused heavily on the convergence of Artificial Intelligence (AI), energy transition, and techonolgy in shaping the future of the global financial landscape, but also the future of the UAE.

The key question that H.E. Khaldoon Khalifa Al Mubarak asked in the opening ceremony was “what kind of infrastructure would be required in 2040?” His view it is not about size, but the ability to move fast and remove friction to attract capital and talent. AI/Digital adoption is the future to provide a strategic advantage whether that be in construction, manufacturing, services or of course finance.

Clear messages from the Economic forum regarding the UAE and Abu Dhabi:

no longer about the quantity, but rather quality of players coming to the UAE

not just about providing capital for a return, but how do those investments benefit the ecosystem of the UAE (bring IP, Manufacturing, Technology, talent...)

The diversification away from oil revenue is happening faster than planned, no-oil GDP grew by 19.5% in 2024 and GDP growth is healthy at 6.6% YoY in Q2 2025.

"The UAE has been noticed" and is hosting one of the most influential finance forum – “we welcome leaders from across the world representing more than 60 trillion dollars in assets, representing over half the world's GDP.”

It is difficult to summarise all the topics that were discussed over 4 days, but obviously crypto, alternatives and private markets were heavily represented, and to some extent public markets – ADX pitched some of its listed companies.

What I enjoy most at those events is the spectrum of ideas and opinions, there is no "wrong” answer:

Are you epecting a Private Market bubble in 2026? UBS CIO no – Ray Dalio - definitly

Is AI capex investment too high? Unamed HF yes – Big Technology investor not enough!

Is Crypto becoming more mainstream and a new investment asset class?

Will the USD weaken in 2026?

So what we learned in the investment streams, yet again, is that there is a lack of consensus on 2026 and the only “free lunch” in town is sensible portfolio diversification.

Some the major announcements and highlights during the conference included:

USD 1.9bn Polio Pledge: A major humanitarian announcement was made on Day 1, with a global coalition, including the Gates Foundation and the Mohamed bin Zayed Foundation for Humanity, committing a total of USD 1.9 billion to the Global Polio Eradication Initiative (GPEI).

Regulatory Approvals and New Entrants: The Financial Services Regulatory Authority (FSRA) of the Abu Dhabi Global Market (ADGM) granted formal authorization to Binance's global platform and gave In-Principle Approvals (IPA) to global investment bank Cantor.

Infrastructure and Real Estate Expansion: Mubadala and Aldar committed to a significant AED 60+ billion (USD 16+ billion) expansion of Al Maryah Island, involving extensive office, residential, and retail development - a well as the announcement of a strategic JV - Aldar Capital.

Strategic Partnerships (MoUs): A total of 24 Memorandums of Understanding were signed between various local and international entities to foster collaboration in fintech, investment, and talent development.

It is truly impressive to see how this financial centre has grown from little more than a building site 10 years ago to now being the capital of capital in the Middle East. Hats off to Abu Dhabi and everyone who has backed them on that journey!

Sandrine Reynaud

——————————————

"The US dollar is doomed… or maybe it isn't!"

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

As 2025 began, arguments that "the US dollar was doomed" were almost too numerous to count. Among them: US debt zooming to $38 trillion, rising inflation, Donald Trump’s tariff plans, and China’s yuan internationalization push. Yet 11-plus months into the year, the “sell America” trade hasn’t been paying off quite as well as the de-dollarization bears expected. While there has been weakness of late, there are reasons to believe that recent dollar losses represent a correction, not the start of a downtrend, and reasons to be relatively bullish on the dollar’s outlook for the year ahead.

Dollar bears often seem to miss the global context. A single variable here and there - like the Fed’s cutting interest rates - surely matters. But a comparison with each of the other four units in the International Monetary Fund’s special drawing rights basket of reserve currencies reminds us why “King Dollar” still reigns.

Looking at the currency competition:

The euro. Though the Eurozone economy is having a solid 2025, broadly speaking, there’s a valid reason the euro currently accounts for only around 20% of global reserves. The 20 countries that use the euro refuse to enter into a strong fiscal union to match the monetary one. So Europe has no single debt instrument to rival US Treasuries. The euro’s limitations are a reminder that the US markets offer unparalleled depth and liquidity;

The yen. Given high expectations for the Bank of Japan to tighten on December 19 for a second time this year, the yen would seem poised for a surge. Yet with Japan skirting recession and Prime Minister Sanae Takaichi’s entire economic strategy predicated on a weak exchange rate, yen bulls are hanging back. Just as RIP-dollar trades haven’t worked out, yen rally predictions get little traction, if any;

The pound. Brexit hasn’t been kind to the globe’s sixth-biggest economy. Recent UK governments haven’t been able to sort out London’s finances. Three years after then - Prime Minister Liz Truss practically broke the bond market, current leader Keir Starmer finds himself fending off speculation that Britain may need an International Management Fund (IMF) bailout. As the Bond Vigilantes watch every word and action by Chancellor of the Exchequer Rachel Reeves, the pound hardly gives off safe-haven vibes;

The yuan. The Chinese currency’s making the majors is a top goal of President Xi Jinping. Next year marks 10 years since the yuan’s inclusion in the IMF’s top-currency club. Yet the yuan still isn’t fully convertible, the People’s Bank of China is anything but independent, and the nation’s underlying economic fundamentals are best described as 'difficult'. Case in point: a seemingly never-ending property crisis that’s generating deflation.

Let’s not be Pollyannish about the dollar’s trajectory. The dollar has plenty of drawbacks. John Maynard Keynes in 1936 likened the currency market to a beauty contest. It’s hard to think of a time when that observation was more relevant than now. But in this pageant, the winner isn’t the prettiest contestant, but the one with the fewest flaws.

One reputed negative for the dollar is the perception that the Fed is being pressured into adding liquidity to an economy that scarcely needs it, and with inflation running hotter than ideal at around 3.0%. Although the fact that Treasury bond yields have been going up in advance of an expected Fed rate cut suggests this might not be the dollar negative it’s cracked up to be. Other dollar drawbacks include the fact that the US can’t claim AAA rated credit anymore and risks associated with Trump’s trade war and disapproval of Fed Chair Jerome Powell.

There’s no telling where Trump's trade war might go in 2026. Trump has teed off on more minor things than news that China’s trade surplus in goods surpassed $1 trillion for the first time and in just 11 months. Then there’s the risk that Trump’s choice to replace Powell as Fed chair triggers a panic in the US Treasury bond market. And there’s always the chance (who knows?) that Trump could try to act on his occasional threats over the years to devalue the dollar.

But there’s no denying that carry trades, borrowing in low-yield yen or Swiss francs, are ending 2025 favouring bets on the dollar’s strength. Or that de-dollarization efforts by China, Saudi Arabia, and “Global South” nations aren’t proving universally successful. The dollar still commands about 60% of central bank reserves, it remains the primary tool in import and export invoicing, and dominates global corporate borrowing.

Disentangling the dollar would be a lengthier, costlier, and more disruptive process than even most adversaries would want to attempt. These are all solid reasons for carry-traders to go long a currency that many detractors assumed would be underground by now. “King Dollar” isn’t likely to be dethroned in 2026.

Justin Oliver

——————————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 14/12/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 14/12/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.