.jpg)

Weekly Newsletter

Freedom Calls: 11/5/26, Back in the UAE, the sun is shining... and performance rocks

by

The Team at Freedom Asset Management

May 11, 2026

12 Minutes

Freedom Calls: 11/5/26, “Back in the UAE, the sun is shining... and performance rocks”

From the team at Freedom Asset Management

It is always great to be back in the UAE, but last week was a little more special, because the country is still grappling with an unpredictable and belligerent neighbour, whilst trying to live life as normally as possible. The Arabian Gazelles were having breakfast on our early morning walk in Saadiyat, yesterday (see below) - they seem pretty untroubled.

In the office, it felt a bit like the initial post-Covid blues, i.e. the brief fun and convenience of working from home has been replaced by the missed social interactions of the workplace. We should be back to a full house in the office on Monday, today, so we are all looking forward to that.

Pictured: Out for the Friday team lunch - last week's scaled back Freedom Abu Dhabi "in office" team (L-R: Shawn, Charles, Shireen, Adrian and Nikita), May 2026

The inconveniences are minor: GPS jamming is still a thing - so taxis get lost easily, and your Strava run will look pretty impressive - see below a 107km run in 18 minutes(!); but these are just inconveniences.

There is much better targeting of missile warnings, so last week, although there was some missile and drone activity, unless you were very close to it, you would not have received the warnings, and therefore you would have gone through life without knowing anything about it. Emirates (into Dubai) and Etihad (into Abu Dhabi) are flying much fuller schedules and are amongst the safest airlines on the planet. They certainly get our votes.

In short, the UAE is very much back in business, which is helpful, because the fund performance is excellent.

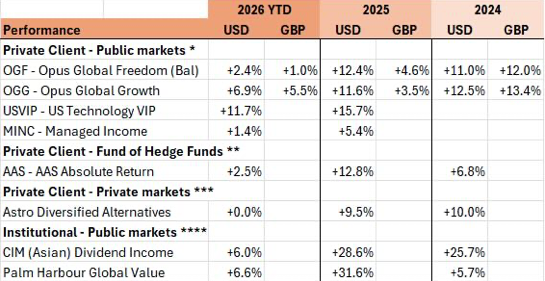

Performance - let’s keep it coming...

(For performance disclaimers see foot of email.)

In the pack above there is some great performance in Opus Global Growth (OGG), which as you may remember blasted through the Iran war with 100% equities on full throttle. Well done Justin.

As for Cody, well our US Technology VIP fund (USVIP) continues to put in performance on rocket fuel. USVIP is now up 29% from its inception in February 2025, with plenty of gas left in the tank to perform through the rest of this year and well beyond. Strap yourself in for the ride.

And our balanced fund, OGF, made it through the war with the lowest draw-down across those three equity-based funds, cutting equities into the war, and with only 40% equities at its low. That fund is now positioned back to 60% equities for a strong remainder to the year.

The more observant will notice a new line in our table, which is our fund of hedge funds, AAS Absolute Return Fund. Its predecessor fund launched in 2016, which we recently re-opened after moving the master fund to Abu Dhabi. We will talk about that one in another Monday piece.

Our articles this week:

Canaccord’s Justin Oliver, Adviser to Opus Global Growth (OGG) writes about the secondary effects of the short term spike in oil prices and the delays we are seeing in the Strait of Hormuz.

- 10,000 Days’ Cody Willard, Adviser to US Technology VIP (USVIP) looks at how technology stocks have staged an impressive come back from their Iran war lows of only a few weeks ago, but reminds us that we are still at the beginning of something that is effectively “inevitable".

Next week, we will commence our new series of articles studying famous fund managers, starting with Stanley Druckenmiller. We will also feature an article on the battle for Chinese LLMs.

Please scroll down to see this week's articles.

Back in Europe: the UK votes for Reform and the Greens, but what does it all really mean?

To our readers outside of the UK, it may seem like any coverage of UK regional council elections - i.e. the people that organise waste collection, road repairs, education and social care - is probably not much an international political event. But this time it was. For many months we had been warned that the two incumbent parties, Labour (the left), and the Conservatives (the right) were seeing their share of the vote eroded by more extreme parties - to the right “Reform", and to the left the Greens. And on the day it happened a massive swing to Reform, and to a lesser but still important extent, the Greens.

Pictured: Reform's leader Nigel Farage looks happy. Picture credit: Byline Times, 2024

Reform are led by the charismatic populist figure Nigel Farage, who was almost single handedly responsible for BREXIT. He enjoyed strong support from former Conservative voters who felt that the Conservatives have gone too soft on BREXIT and immigration, amongst other things.

The Greens are led by Zack Polanski, who before his glittering political career, was an (alleged) former conman - the con: to convince ladies he could increase their breast size by hypnotherapy from a clinic in London’s expensive medical capital, Harley Street. His greatest other professional achievement seems to have been as “an immersive theatre actor”. He is a pro-Palestine activist, avowed communist and believes that environmental issues should be deprioritised at the Green Party. Yes that is the quality of political candidate we attract in the UK. Curious.

So how did that happen? And what does it mean?

Basically, the Green Party has been highjacked by the hard-left members of Labour. So you have all these well-meaning, open-toe sandal-wearing types who thought they voting to make the world a kinder place, and a plant a few more trees, being joined by the extremist pro-Palestine lobby and hard-core communists.

So anyway, I reached for that bastion of balanced journalism, “The Communist”, in search of a sympathetic critique of Scam Polanski’s new Green policies.

Pictured: (L-R) Green Party’s leader "Scam" Polanski and the not visibly thrilled Hannah Spencer MP (who joined the Green Party "to save dogs from dog racing” rather than perhaps its new agenda), Source and picture credit: www.communist.red

Even "The Communist" struggled to be sympathetic:

"Polanski primarily aims his message at workers and youth whose main priority is ending brutal austerity, rampant inequality, environmental destruction, and imperialist war. Thus far, however, this appeal has mainly involved rhetoric and ‘vibes’, rather than any real political substance. Polanski’s campaigning has mostly been limited to a description of the problems facing British workers, in place of any clear solutions.” The Communist, 9/4/26

Oh well, I guess it’s tough being a communist, because the only outcome is "inevitable failure" as Mrs Thatcher rightly pointed out. And if you are looking for supporters of communism, don't go looking in Eastern Europe - those memories are still too recent, as one of my former Schroders colleagues from Poland used to say:

"…on Wednesday we stood in line for bread… and on Thursday it was for toilet paper…. Nobody in Poland is going back to Communism anytime soon."

But it does, in some respects, mirror the moves happening on the other side of the Atlantic, with New York City recently voting for socialist Mayor Zohran Mandami. He is now grappling with the fact that the big tax payers in New York City have a choice on where to live - and a number of key financial businesses are down-sizing in the city, including JP Morgan, Citadel, Apollo and Goldman Sachs, choosing instead to build their franchises in more tax friendly states - like Texas and Florida. At that point, strangely, the socialist maths does not work any more. Surely we have to move to a version of democracy, where to be eligible, the party leaders must at least have taken an A-level equivalent paper in Economics, or Mathematics - and preferably both.

But all is not lost. In the UK at least we know what the solution is: the Conservatives and Reform need to sort out their problems - together they would win an outright majority - and the UK would once again play to the right of centre, which is where it belongs. But sadly, we still have another 3 years before that can happen at national government level.

This week Abu Dhabi

This week I am with the team and investors in Abu Dhabi. The following week it will be Abu Dhabi, Guernsey and Hong Kong (in that order) - so you can be sure there is no "air miles shame" at Freedom!

Wishing you all a wonderful and peace week ahead,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

———————————————————

“Looking beyond the spike in crude oil prices”, 11/5/26

By Canaccord’s Justin Oliver, Investment Adviser the Opus Global Growth Fund

The economic consequences of the conflict involving Iran are increasingly extending beyond crude oil markets. While much of the initial investor focus centred on the implications for energy prices and the Strait of Hormuz, the disruption is now spreading through global supply chains for a wide range of industrial commodities, chemicals and agricultural inputs. The resulting shortages and price increases risk creating a more persistent inflationary shock than many had initially anticipated.

The Gulf region plays a critical role in the global petrochemical industry, hosting close to 200 major complexes that collectively account for a significant share of worldwide supply. Damage sustained by facilities in Kuwait and Qatar has already materially impaired production, with several operators declaring force majeure. Qatar’s Ras Laffan complex, a major exporter of liquefied natural gas and helium, may require years of repair work according to early estimates, though some infrastructure elsewhere may be restored more quickly once shipping routes normalise. Even if portions of production recover within months, supply interruptions are already affecting a broad list of commodities including sulphur, methanol, ammonia, urea, naphtha, benzene, styrene, aluminium and helium. Many of these materials are essential inputs across manufacturing, agriculture, technology and clean energy industries.

Source: Yardeni, Capital Alpha

The consequences are particularly acute for sectors linked to the global energy transition. Aluminium, sulphur and helium are all critical to semiconductors, batteries, solar technology and energy storage systems. The International Energy Agency recently described the Strait of Hormuz crisis as potentially the largest energy security threat in modern history, while the UN Economic Commission for Europe warned that industries dependent on these inputs may be forced to scale back production as costs rise sharply. Chemical producers are already signalling caution. Dow Chemical has warned that higher raw material costs and geopolitical instability may lead to delays or cancellations of planned investment projects. At the same time, supply disruptions are creating further stress for industries already contending with slower demand growth and rising financing costs.

Fertiliser markets have become a particular source of concern. Approximately one fifth of global seaborne fertiliser trade passes through the Strait of Hormuz, while the percentages for ammonia and urea are even higher. The UN Food and Agriculture Organization has warned that disruption to roughly three million metric tonnes of monthly fertiliser supply could negatively impact key planting seasons later this year, ultimately reducing crop yields and increasing food inflation globally.

The implications extend well beyond agriculture alone. Higher diesel prices are increasing farming costs, while disruptions to petrochemical feedstocks are driving up packaging expenses for food producers. Aluminium prices, meanwhile, are pushing canned food costs higher. Fertiliser prices themselves have reportedly risen by around 80% since the conflict escalated.

The broader inflationary impact could prove especially damaging for emerging economies. Food and most globally traded commodities are priced in US dollars, meaning a stronger dollar further increases import costs for poorer nations already under pressure. Countries heavily dependent on imported fertiliser or grain across Asia, Africa and Latin America may face growing economic and social strain should elevated prices persist. China’s recent actions have added further pressure to already fragile supply chains. The country, which accounts for roughly a quarter of global fertiliser production, has tightened export restrictions across several categories of fertiliser products. Reuters estimates that between half and four fifths of mainland fertiliser exports are now subject to restrictions, impacting countries such as Thailand, Vietnam and the Philippines particularly heavily.

Beyond fertilisers, the knock-on effects are spreading into industrial metals and mining. Sulphur prices have risen sharply, increasing costs for nickel, copper and cobalt processing. Indonesia, one of the world’s largest nickel producers, has already reduced operating rates as production economics deteriorate. Macquarie estimates that rising sulphur costs since early 2025 have increased Indonesian nickel production expenses by around $4,000 per tonne for sulphur-intensive refining methods. Aluminium markets have also tightened significantly following production disruptions in Bahrain and the UAE. Prices recently climbed to near four-year highs, creating additional cost pressures for industries ranging from electric vehicles to data centre construction, both of which continue to experience strong structural demand growth.

Governments are beginning to respond through increasingly protectionist measures. China plans to restrict sulfuric acid exports, Turkey has already enacted export bans, and India is reportedly considering similar actions. Such developments risk amplifying existing shortages and further fragmenting already stressed global supply chains.

In the United States, these disruptions are also complicating efforts to secure critical mineral supply chains. The Trump administration’s proposed “Project Vault”, designed to establish strategic reserves of critical materials for industrial use, faces the difficult task of sourcing materials at a time of volatile prices and constrained supply. Policymakers have increasingly acknowledged that processing capability, rather than simply raw material availability, remains one of the US economy’s greatest vulnerabilities.

Against this challenging geopolitical backdrop, financial markets have nevertheless continued to demonstrate resilience. Corporate earnings expectations in the US remain robust, with analysts raising forecasts for both revenues and margins. Forward S&P 500 profit margin expectations recently climbed to a record 15.3%, while expected earnings growth for the coming year has risen to nearly 20%. Several sectors continue to exhibit particularly strong profitability trends, most notably technology, communication services and financials. The information technology sector now carries forward profit margins approaching 32%, supported by continued investment in artificial intelligence infrastructure and digitalisation trends. Meanwhile, revenues and earnings expectations across much of the broader index remain close to historic highs despite ongoing geopolitical uncertainty.

This divergence between geopolitical stress and underlying corporate resilience highlights an important feature of the current environment. While supply chain disruption, commodity inflation and food security risks represent genuine threats to the global economy, large parts of the corporate sector continue to benefit from strong structural demand trends, particularly within technology and infrastructure-related industries.

Ultimately, the conflict’s economic consequences are unlikely to be limited to a short-term oil shock. The breadth of affected supply chains, combined with rising protectionism and pressure on agricultural markets, raises the possibility of a more prolonged period of elevated input costs and uneven global growth.

However, while these developments create clear risks for inflation and economic stability, the continued strength of corporate earnings and investment in long-term growth themes suggest that markets may remain more resilient than headline geopolitical developments alone would imply.

Justin Oliver

————————————————————

“It’s just the beginning… what we invest in as revolutionary investors is inevitable”

By the team at 10,000 Days, Investment Advisers to the US Technology VIP Fund

She looked at me with big brown eyes and said

"You ain't seen nothing yet

B-b-b-baby, you just ain't seen n-n-n-nothing yet

Here's somethin' that you're never gonna forget” — Bachman Turner Overdrive

Well, I wrote in last month’s factsheet that: “I’ve been Revolution Investing for nearly 30 years now and this is perhaps the single best long-term set up I’ve ever seen for my approach”. Amazingly enough, most every Revolutionary tech company’s stock is up huge since last month and the US Tech VIP fund had its best month ever. The fact of the matter is that I think that this is just the beginning.

The economy has continued to chug along here even as oil and energy prices as well as war and geopolitical tensions all continue to escalate. Other than the War with Iran and the potential for it to spiral into a vicious cycle as all wars can, by far the most important near-term economic theme here is the incredible CapEx super cycle that we’re living through as the hyperscalers like Amazon, Google and Microsoft along with neoscalers like CoreWeave and Nebius and in-house AI power players like Meta and Tesla (in-house, because they use all of their compute internally rather than selling/renting it to others) are still upping their spend on CapEx for AI.

The impact of nearly 3% of the US GDP — more than a trillion dollars of economic activity from the AI super cycle spend this year alone, up from less than $100 billion a few years ago — is simply unprecedented in the history of economic cycles, including rail roads and the Internet or even the Roman aqueducts. Those spending cycles took decades to happen and never accelerated at the annual pace that this incredible super cycle of AI CapEx is.

Just as important is that the ROI on this AI CapEx super cycle is so high and so quick that these companies are trying to spend as much as possible and the main constraint is simply supply, which is being addressed just as quickly in a CapEx super cycle in the semiconductor industry.

I often tell people that what we invest in as Revolutionary Investors is probably inevitable— the question is one of timing. It might take five more years or ten more years to get to the point where instant custom movies are mainstream. But we will get there at some point.

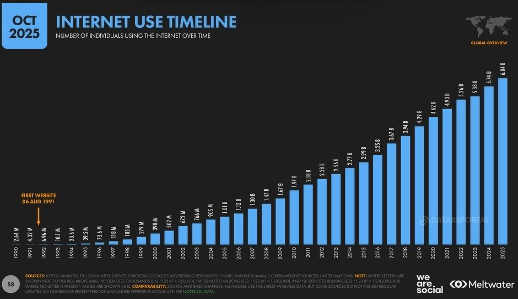

Look at this chart, which we have used before, of Internet traffic over the last thirty years as its inevitable growth took hold:

That growth is currently accelerating once again as The AI Revolution takes off.

There are just so many virtuous circles rotating out from The AI Revolution and we’re just now starting to see those fundamentals accelerate and spread out in their impact on so many other sectors of the economy too that we will likely be blown away by how strong the US (and much of the global economy) will be this year vs current expectations. Next year’s economy will likely be even stronger given that we don’t have a prolonged period of oil being, say, above $150 for three or four quarters in a row which would likely hurt the middle class and many industries badly enough to undermine the super cycle and cause a recession. Even then, there’s no doubt that the AI CapEx will continue to grow longer-term, it’s just that the magic results that we’re seeing every day from The AI Revolution might take a little longer to be realized than they currently look like they will be.

I haven’t even mentioned The Robotics Revolution yet, which itself is starting its own super cycle which is less than 1% of the way completed. The integration of robots into industry is happening so much faster than most analysts realize. You’ve got farmers in New Mexico who have just started using laser beam-shooting robots to cut costs and improve yields. You’ve got high rise construction companies in Abu Dhabi who have just started using rebar-tying and Sheetrock-hanging robots to cut costs and improve efficiencies, productivity and time-to-market. You’ve got the militaries around the world who are increasingly starting to use drones (a form of robots, of course) in the air and in the sea to save lives, protect resources and, unfortunately, to fight each other too.

The Space Revolution? Yup, accelerating too as the SpaceX IPO and the Starship get ever closer too.

There’s a lot for Revolution Investors to be excited about near-term. There’s oh so much more for Revolution Investors to be excited about long-term. We were 99.9% fully invested with de minimis cash on the day the market bottomed last month. And, yes, we’ve had an incredible move off the bottom in the month since. But with this economic set up, these valuations (which are up from where they were when I was pounding the table but are still incredibly compelling here) and these inflection points each getting started but at various first inning stages here (The AI Revolution is maybe half way through the first inning, The Robotics Revolution is barely one batter into the top of the first inning, and The Space Revolution is still in pre-game warm ups!), well… baby, you just ain’t seen nothing yet.

Cody Willard

—————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated.

Sources:

* Estimates Freedom Asset Management as at 9/5/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25.

** Performance estimated from JP Morgan supplied estimates, using Class B shares. Fund prices monthly, with monthly subscriptions and quarterly (qtr/90) redemptions.

*** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 estimate takes the MCAS December 2025 estimate and deducts the estimated charges of the Astro feeder fund.

**** Morningstar as at 9/5/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Unit 2117, Level 21, New World Tower 1, 16-18 Queen's Road Central, Hong Kong.

© 2026 Freedom Asset Management Limited.