.jpg)

Weekly Newsletter

Freedom Calls: 1/12/25, Farmers protest in London and there's value to be found in China

by

The team at Freedom Asset Management

December 1, 2025

10 Minutes

Freedom Calls: 1/12/25, "Farmers protest in London and there's value to be found in China"

From the team at Freedom Asset Management

Farmers protest on the streets of London

Every French President knows that it is unwise to upset the farmers. Last week, for the much-feared occasion of the UK budget, British farmers decided to protest on the streets of London, bringing all manner of farm equipment and slogans with them to make their point. It was all fairly good humoured, and to be honest the farmers seemed more interested in showing off their shiny new tractors to each other, but suffice it to say on Wednesday it was easier to walk to meetings than take road transport!

In the end, the UK budget was the worst managed PR event in history. Having prepared the country for mass misery in a run up of several weeks and months, the actual event neither fixed the gaping hole in public finances, nor did anything to address spending on the welfare state (in fact they increased it)…. and as for economic growth, well that is being left for future governments obviously. It is just possible that Labour have now given up - and decided it's better to give their mates what they want for the next 3 years before they are banished from taking power ever again.

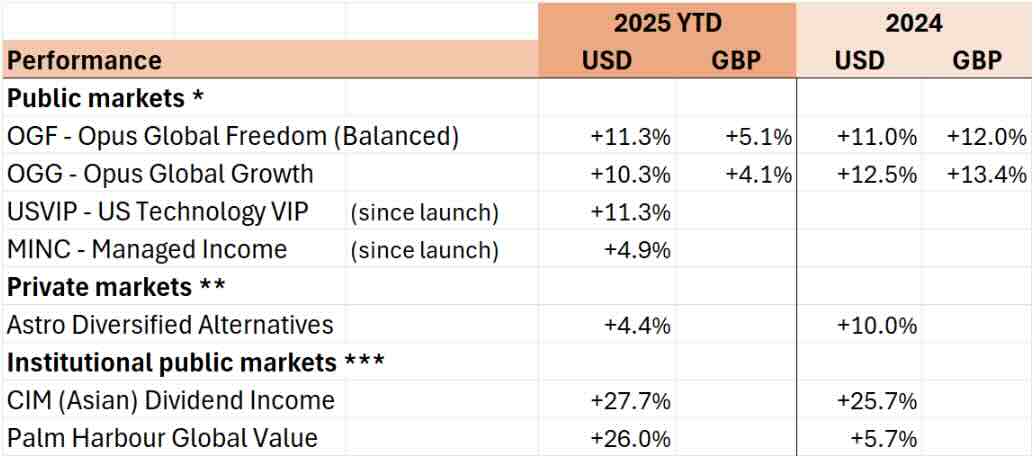

Performance - a great week all round

(See performance disclaimers at the foot of the email)

Well done to everyone who took the cue to come in or top up on Monday last week. Not that we are completely surprised, but OGF was up 2%, OGG up 3% and USVIP up 6% on the week.

Whilst I don’t pity the short sellers and the “end is nigh” people, it’s rough out there trying to make money out of other people’s misfortune. Long may that continue.

The news that drove markets forward was the increased likelihood of an interest rate cut in December from the Fed. Having only a week earlier seemed less than likely, the sentiment changed and together with a bit of Thanksgiving spirit, the S&P was up strongly.

We are still about 6-8% off prior highs on USVIP, so apart from the near-term "discount", the market has gone back to liking some tech/AI stocks again. This is immensely logical because everyone agrees that AI is a good thing that will bring productivity gains in the workplace, leading to deflationary cost pressures on businesses and the economy more broadly. That being said, at these levels some of those AI, space and fintech plays are still off around 40%+ from their recent peaks, so there are plenty of bargains to pick up for the well informed.

Importantly also, OGG had a good run last week, with its outsized exposure to healthcare finally being rewarded.

Ukraine - a deal seems possible

Whilst we did not get the Ukraine peace deal signed before Thanksgiving as Trump had hoped, it does look like we are now on a one-way street to an outcome which will work for enough people.

Some might say that the timing on the release of another corruption report inside the Ukrainian government may not be entirely accidental, possibly to "encourage" some compromise, but most of the world will be happier when this is settled. The people who will win the most out of it will be the Americans; the people who will end up funding it all are the Europeans; and the Russians will end up paying twice - once for the tract of land they have just acquired by way of reparations to Ukraine, and then secondly to rebuild that very same bomb site they have just acquired.

I sat down with one of the UK's leading sanctions counsel last week. His analysis was that we should expect OFAC sanctions to come off in a structured but relatively quick manner when a deal is announced, but we should not expect the same haste in the UK or the EU. This will present another set of economic advantages to US firms over their European cousins.

Our articles this week

Cody Willard and Bryce Smith from 10,000 Days, advisers to US Technology VIP (USVIP), write about how "AVs will blow your mind!"

Justin Oliver from Canaccord, adviser to Opus Global Growth (OGG), tells us that "AI takes the lead in online shopping"

Finally we have an article from Florian Weidinger, CIO at Santa Lucia Asset Management. Florian manages the highly successful c.$1bn CIM (Asian) Dividend income Fund, which we own in the OGF (Balanced) fund and the firm has distributed to mainly European institutions. He talks about how a value fund manager can find opportunity (to great effect) when others only see negative headlines and numbers.

Please scroll down to read the articles.

Bank holiday in the UAE

Please remember there is a bank holiday today and Tuesday in the UAE. This means that our ADGM office will be closed and our ADGM funds will not deal today, but will deal on Wednesday instead, using all subscriptions that met last Friday's cut-off, priced at last Friday's close of market.

I am in Abu Dhabi until 9th December and will be attending the Mubadala Capital AGM on Friday for an update on private equity and venture markets. I also look forward to meeting many friends of the firm at Abu Dhabi Finance Week starting next Monday.

Wherever you are this week, please let me wish you a wonderful and peaceful week ahead,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

——————————————

"Autonomous Vehicles (AV's) will blow your mind!", 1/12/25

By 10,000 Days’ Cody Willard and Bryce Smith, Adviser to the US Technology VIP Fund

Bryce here. While we often talk about the very attractive economics of autonomous vehicles (AV), but we also have a moral imperative to deliver safe autonomous driving. Globally, road traffic crashes kill about 1.2 million people every year—roughly four times the number of American service members killed in action in World War II. In the U.S. alone, we lose around 40,000 people annually to traffic fatalities, which is about sixteen times the total American deaths over two decades of war in Afghanistan.

But last weekend while in Austin, TX for a University of Texas (UT) football game, I got a glimpse of a better future of transportation: Waymo (owned by Google) and Tesla Robotaxi.

Apologize as I forgot to get pics of the Waymo (note the Tesla safety monitor was in the driver’s seat in the pic above because there were four of us in the car, and she’s holding the wheel here but the display showed us in full autonomy the whole time).

Both services are extremely impressive and the autonomous experience is far better than taking an Uber or a taxi. To my surprise, my group of seven cowboy/rural American friends all preferred the AVs to regular Ubers. Mind you, these are guys who drive Ford F-350s, not Tesla Model Ys.

As both a Tesla and Google shareholder, I recognize that I am biased, but it is hard not to recognize the objective improvements in AVs over traditional rideshare/taxis when you experience them first hand. And seeing all of my friends talk about how impressed they were with the AVs and how they all actively preferred them over the traditional options just reaffirmed my long-held thesis that this is a MASSIVE Revolution that is still in its infancy. AVs are barely getting started, and they are going to unlock trillions of economic value and save millions of lives over the coming decade.

I recognize that many of our readers have probably never experienced a ride in a fully autonomous vehicle, so I’ll start with my takeaways from the experience, and then we’ll hit on some of the investment/economic implications.

First and foremost, the quality of the autonomous “driver” was just better than most human drivers in my opinion and those of my friends. The consensus amongst the group was that Waymo was a smoother driver than Tesla at this point, but across the board, everybody preferred not having a random human (who can often be erratic) behind the wheel.

On that note, one of the most shocking things to me was that neither I nor my friends ever felt unsafe, and I would even go as far as to say that the AVs already feel like much safer drivers than humans. No sudden braking, no quick lane changes, no yelling at other drivers, no honking; just a safe, smooth drive. Plus, you as the passenger are in total control of the music, climate, etc. and you actually look forward to a ride in an AV.

One thing that you don’t truly appreciate until you ride in an AV is how nice it is to get in a vehicle with just you and your guests. Every Waymo and Tesla we rode in were super clean, smelled nice and new, and we didn’t have to make small talk with some stranger questioning us about our politics when we were just trying to get to a restaurant. The whole experience is absolutely a step change in the method of getting from Point A to Point B.

And of course, the cost difference, and this is where Tesla really took the cake. The Tesla Robotaxi service was consistently about 1/10th the cost of both Uber and Waymo (we’re talking $2-$3 for a 20-minute ride across downtown vs $25-$35 for Uber/Waymo). I recognize that Tesla is likely offering promotional pricing for Robotaxi to drive user growth in these early days, but it's reflective of Tesla’s massive long-term competitive advantage. Tesla’s Model Y (equipped with eight cameras) costs the company around $32,000 to make and “just works” using the same FSD software Tesla has been selling for years, whereas the Waymo vehicle (equipped with 4 lidar, 6 radar, and 13 cameras) costs somewhere around $150,000-$200,000 and requires advanced pre-mapping of every city before it can be used. In the long run, I think there will be room for both services (as I discuss below).

My recent autonomous experience reinvigorated my excitement for The AV Revolution, and I couldn’t stop thinking about it all week. And the more I thought about it, the more I realized that The AV Revolution has so much potential and it will be much bigger than just Tesla Robotaxis (although Tesla will be the biggest player given its cost advantage). This is very much in the same vein as the epiphany I had a few weeks back when I realized that The Robotics Revolution would be much bigger than simply humanoids.

So let’s talk a bit about the economics of AVs. Autonomous vehicles are fundamentally a story of two things, asset utilization and safety. If the cars can drive themselves, the use case is no longer limited by human time. My autonomous car can take me to work at 7:00am, then it can take my neighbour to work at 8:00am, then it can take my neighbours cousin’s kid to school across town, then it can go to my favorite Italian restaurant which happens to be next to the school and pick up lunch for me and bring it to my office. That’s a lot of productive stuff (efficiency) happening when my car would otherwise be idle.

And second, in terms of safety, I’m ready to say that AVs are already safer than human drivers, and probably safer than human drivers by an order of magnitude. Tesla and Waymo have both released data to back this up. Millions of humans die every year on the roads, and we have a moral imperative to figure out a safer way to move ourselves around. Even though an AV will likely hurt someone at some point in the future, they will save millions more lives than they ever take, and the technology will only get better with time (that’s not true with humans).

Importantly, I don’t think the AV market will be a winner-take-all market. More likely there will be tiers of offerings and there will be room for both Tesla’s Robotaxi (which will likely be the mainstream, low-cost option) and Waymo (the premium/luxury tier). Just look at the auto market today: the cheapest car doesn’t always win. There is a huge market for higher-end vehicles. People like different body styles, interior features, colors, etc, as the car is an expression of personality for a lot of people. I think the same will be true for AVs. And for that reason, Waymo and Tesla will likely start selling “autonomy as a service” (AaaS) for all those people that want to buy a fully autonomous Lexus or Mercedes or Ferrari.

And even while the technology keeps developing, capturing a small sliver of the transportation market in the near term could be huge for both Waymo and Tesla. For context, Uber and Lyft give almost 40 million rides per day between the two services. If Waymo can tap just 10% of the existing market by the year 2029 (not to mention, the market will grow dramatically as AVs drop the price of transportation), our very-conservative model below shows that the service could be worth between $140-$230 billion in incremental valuation to Google.

Critically, the model shows very attractive returns for Google as the operator of the service (over 50% return on assets by 2028) which is driven by the high efficiency and utilization of the robotaxis themselves. Using the most recent public data from Waymo, I calculated that each Waymo is giving about one ride per hour (on a 24/7 basis), which is already exceeding human efficiency. The Uber CEO recently confirmed that “the average Waymo is busier than 99% of our drivers in terms of completed trips per day” (note Uber is Waymo’s exclusive rideshare partner in Austin, TX and Atlanta, GA). Again, this efficiency will only improve as Waymo further improves its technology, adds more cars to the fleet, and makes the service available more broadly.

In conclusion, the AV experience is truly mind blowing and this Revolution is barely getting started. The future of transportation is going to be radically different from the transportation of the past. Some day, we will tell our kids stories about what it was like to ride with a crazy Uber driver and how dangerous traveling used to be. Waymo and Tesla will both likely operate massive robotaxi fleets, and also sell autonomy as a service to other companies who will find amazing new ways to apply the technology (trucking, delivery, etc.). This is the future of physical AI, and in the US Tech VIP fund, we have outsized positions in the two primary companies driving this burgeoning Revolution (GOOG and TSLA). And more importantly, this new technology will save tens of millions of lives in the coming decades!

Bryce Smith

———————————————

“AI takes the lead in online shopping”, 1/12/25

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Retailers are deploying artificial intelligence throughout their operations to become more efficient. AI is helping retailers to manage inventories, build customer profiles, improve demand forecasting, optimise pricing, and increase loss prevention. But consumers will interact the most with AI shopping agents, which will help them pick out gifts for themselves and others.

Consumers are quickly adopting AI as a tool to research and comparison shop. Generative AI was used for search and product comparison by 30%-40% of US consumers surveyed in October by Bain & Company. In just the 12 months, from October 2024 to October 2025, ChatGPT’s referrals to retail websites surged from 1.7 million to 14.4 million and OpenAI’s percentage of total referrals made to retailers’ sites nearly doubled from 7% to 16%. In fact, for some retailers, like Home Depot and Etsy, ChatGPT referrals account for 25% of all referral traffic but still less than 1% of total traffic. That said, just over half of consumers surveyed (51%) claim to distrust AI agents.

Looking forward to this holiday season, online shoppers said they’d start shopping primarily at traditional online retailers, but 17% cited an AI agent—be it Chat GPT, Perplexity, or another—as a planned resource as well. The mix of shopping resources that respondents said they’d tap (choosing all that apply):

Amazon (73% of respondents)

Other retail websites (37%)

Google (30%)

Website of a specific brand or product (24%)

Social media platform (20%)

ChatGPT (13%)

Blog or review site (7%)

Other search engine (6%)

Other AI chat bot or assistant (4%)

Perplexity (4%)

As third-party AI agents become more popular, retailers will have to ensure that their sites and offerings can be searched by AI agents, if they haven’t already. They will also need to decide who executes the final transaction—the retailer or the AI agent? The answer may determine who “owns” the consumer in the future.

In time for the holidays, ChatGPT introduced a personal shopper that helps consumers find and research products before making purchases, according to the company’s blog post. Users can describe what they’re looking for, the AI can ask additional questions to narrow the search, and the search can be refined along the way. The new service works best with products that have a lot of descriptive detail. Eventually, buyers will be able to make purchases directly through ChatGPT from merchants in its Instant Checkout program.

Rufus, Amazon’s AI shopping agent, has recently been upgraded to teach this not-so-old-dog new tricks. The agent uses large language models—including Anthropic’s Claude, Sonnet, Amazon Nova—and a custom-built model that draws from Amazon’s product catalogue, reviews, and Q&As, as well as information from across the web. It uses RAG, or retrieval-augmented generation, to tap popular publications (e.g., The New York Times, USA Today, Good Housekeeping, Vogue) for answers about products and trends.

More than 250 million customers have used Rufus this year, and those who have are 60% more likely to make a purchase during their shopping trip. No wonder: Rufus can compare similar items and highlight the differences between them. It can “remember” the shopper’s Amazon history to offer recommendations—such as suggesting appropriately cushioned running shoes for a shopper who plays tennis. It shows consumers items available on both Amazon and other online retailers’ sites. For those of us who are old school, Rufus will take uploaded photos of handwritten shopping lists and deposit the items in one’s Amazon shopping cart. Rufus can also solve problems. Show it a carpet stain, and Rufus will display the most relevant cleaning supplies.

Rufus may give real dogs competition for the title of “man’s best friend”!

Justin Oliver

—————————————

"The value investor's guide to China", 1/12/25

By Florian Weidinger, CIO of Santa Lucia Asset Management

2024 and 2025 were the years of the biggest property price declines in China. These were also the years where the Hang Seng China Enterprise stock market index (HSCEI) posted gains of +27% and +25%, respectively outperforming US equities.

In public market investing it is all too tempting to draw a straight line from the newspaper headlines, the macroeconomic statistics, and the look and feel of the streets. We do all of the above in our research, including pounding Asian pavements relentlessly.

But the conclusion on the right investment choice needs to contrast that "look out of the window" with an assessment of “what is in the price”. Public market investors don’t trade their perceived manifestation of today, they trade their priced expectations of the future.

This short piece is not a case for the Chinese economy - indeed there are quite a few negatives out there, namely:

- household wealth, local government finances and banking equity have all been burdened by losses from the decline in property prices, leading to reduced consumption, investment and lending capacity;

the economy has been over-reliant on historically investment, manufacturing and net exports, and the economy is struggling to raise the share of consumption in GDP;

global fracturing into spheres of influence and China-US confrontation leading to uneconomic choices by state actors are a net loss to all concerned.

Yet there were opportunities in Greater China publicly listed equities, labelled “uninvestable” at a point in time when it was not very costly to do so (when the Hang Seng lagged, followed by e.g. Stephen Roach prognosticating the end of Hong Kong near the low).

Even after a strong recent run in Greater China equities, (the HSCEI produced a total return of 63% over the last three years in US Dollars,) there are investable bright spots available at reasonable valuations:

1. Significant equity risk premium available to harvest for value investors

The dividend yield of the Hang Seng China Enterprise Index (HSCEI) at 2.8% is around 1.6x the 10-year government bond yield in China at 1.8%. For the S&P500 it is – you guessed it – the reverse, with the dividend yield of around 1.1% at just over a quarter the treasury yield around 4.0%. The earnings yield of the HSCI at around 8.6% is a significant spread to the corporate cost of borrowing which is routinely below 4%, incentivizing accretive capital management.

2. Rising earnings contribution from foreign earnings

While China’s domestic economy is weak, many highly competitive manufacturing firms have found export success abroad in countries of the Global South, such as Latin America, Southeast Asia, Africa, but also the Middle East. Exports to the US are only around a tenth of China’s total by now.

China is trading more and more with its friends, and this is becoming a major earnings driver for e.g. the industrial goods sector, which is displacing Korean and Japanese competition. An example from the portfolio is the fund’s Zoomlion investment, up around 70% since initial purchase last year, and still attractive at only 11x 2026 earnings and a 7% current dividend yield via the H-shares. The company is an interesting little microcosm of China’s industrial firms navigating domestic weakness in taking global market share and thus exporting industrial goods deflation to the rest of the world.

Ostensibly a construction equipment maker in a weak economy, profits from its overseas business now make up more than 80% of total profitability, initially not recognized by the public market. This is generally easier if you are a midsize company i.e. there is a possibility to add a segment or a business line, compared to the very large companies where the opportunity is more capped by the size of the total pie. As China’s share of global manufacturing hits 30%, its market share in many global industrial categories to the world excluding the US may well creep up.

3. Shareholder Value orientation

“Value Up”, improvements in governance, capital management with buybacks and rising dividends, is radiating out from Japan across Asia, with China/HK (and Korea) as the leading hotspots. Beijing has paid close attention to the Japanese experience. China started quietly with transformative reforms under SASAC of the state-owned enterprise sector, making return on equity targets a mandatory KPI, encouraging share buybacks and creating more than one hundred state-owned firms with share option schemes for management. This is broadening to the private sector now. Following the securities regulator CSRC’s release of Market Value Management Guidelines in Nov 2024 (which had followed the January guidelines for SOEs), according to brokers CLSA “450 A-share companies have disclosed a market value management policy and c.220 A-share companies have released a value enhancement plan so far”; an effort that’s off to a good start.

4. Local marginal buyers (insurers, households) positioning to purchase more local shares

US$23tn of Chinese household deposits earning measly interest of around 1% p.a. in the bank could be tempted into the equity market. There are early signs that animal spirits are rising: trading accounts by retail hit their second highest monthly reading after September 2024; sales of wealth management products are up in issuance; and record Southbound Connect purchases of more than US$100bn this year flowed into Hong Kong H-shares from mainland investors.

More immediate, according to Goldman Sachs over US$1tn of incremental purchases of Chinese equities by insurance companies (following a lift of regulatory ceilings) could be targeting specifically high yield dividend stocks. The free float of Greater China equities yielding more than 4%, suitable for insurers to purchase, may only be around $2tn. In other words, insurers would have to purchase close to half the float of all dividend yielders if they wanted to supplement their portfolios, starved of income at a time of sovereign bond yields of 1.8%.

The principles of the late legendary international value investor Peter Cundill, the “C” in our CIM flagship fund name, and author of “There is always something to do” are timeless: in every market, whatever the headlines, the disciplined investor can find something interesting to do and exploit. And when the relative risk-rewards and circumstances change again, the beauty of the public market consistently allows us at SLAM to reassess and find the next interesting thing to do in our big universe of Asian equities, so frequently misunderstood.

Florian Weidinger

————————————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 30/11/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 30/11/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.