Weekly Newsletter

Freedom Calls: 8/9/25, “Cody on the road …. And when can I retire?”

by

Freedom Asset Team

September 8, 2025

7 Minutes

Freedom Calls: 8/9/25, “Cody on the road …. And when can I retire?”

From the team at Freedom Asset Management

If last week was the gentle “back to work/school” week, this week will be full-on with an obligatory tube strike in socialist London just to get us back into the mood (see image below). Only under socialism do driverless-trains (the DLR) get to go on strike to demand a 32-hour week… because of “fatigue management and extreme shift patterns”?! Oh well, New York, be careful what you wish for…

Picture credit Yahoo UK, Sept 2025

We are officially on the road with the Cody Willard and Bryce Smith talking US Revolutionary Tech for the next 3 weeks

This week it is London (tube strike or not) and Guernsey. Next week it is Abu Dhabi and Dubai. Cody will be on CNBC on Monday 15th September at 0800 local time from Abu Dhabi – we are grateful to our friends at CNBC for hosting us. The last week of the trip is Hong Kong where Cody will be delivering a keynote speech at a family office conference in partnership with our friends at UOB Kay Hian. We look forward to seeing as many of our investors and friends of the firm over the coming 3 weeks. Please reach out if we haven’t yet sorted out a slot for you.

“When can I retire?”

For some of our investors who enjoyed the summer holidays too much and are thinking about the glide path to retirement, September is always a good time to reflect on how the pension pot is looking and whether there is enough. And what is “enough” anyway?

There are no hard and fast rules on this, because we are all different, but I share a few observations we have gleaned from speaking to our investors and trawling through the research:

- You seldom need as much income as you think. The reality is that in retirement you just spend (much) less than you did when you were rushing around catching early morning expensive trains, buying expensive coffees and sandwiches (if you are in London), or hanging out in glitzy restaurants 3x nights a week and sneaking off to the Maldives for a long weekend (in the UAE).

- Get rid of the kids. Ideally, make sure the kids are through school and university and off the family payroll before your retire. (Don’t worry, I do appreciate the irony in this comment!)

- Get rid of the mortgage. Whatever you call home, make that mortgage-free before you do any pension calculations – if you are lucky that might be two homes, but don’t forget long term rentals on Airbnb are becoming an attractive alternative to the “second” home these days.

- Cash alone is unlikely to get you there. Unless you have a very large pot to start with, we are moving to a world of lower short term interest rates (starting probably this month in the US) and probably higher long term inflation – so bank deposits alone are going to come up short when you take inflation into account.

- The 4% rule. Research suggests that if you were to invest your money in a balanced fund (like the Opus Global Freedom Fund - OGF), and withdrew 4% a year, not only would that provide you with an “income”, but also it should protect the value of your savings from reasonable inflation. So your ideal target return is something like 8% p.a. in the world’s most important currency, i.e. US dollars, and OGF is our “one stop shop” for that risk/return profile.

There are obviously so many caveats to the points above that it is impossible to list them, so I won’t try. And please remember, in the words of the former UK deputy prime minister, Angela Rayner, “everyone should seek specialist tax advice”, or at the very least understand the basic tax rules of the country they wish to retire in.

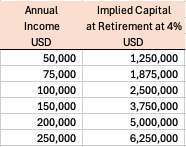

So what does it mean in real numbers?

In the maths of pension planning, “more is always more”, but this simple table shows you how much you should be starting retirement with to reach your target “income” numbers and for that pension pot to have a good chance of keeping pace with inflation:

Source: Freedom Asset Management

For most of us this is a bit of a wake-up call, but it is never too late to do something about it. Selling the children, or marrying a rich widow are options… but it is generally better to keep the family on side with some sensible savings and retirement planning.

We use our Opus Global Freedom fund as a core position and add the other funds around that to reach the risk/return profile we think is right for us. Our more sophisticated investors will choose maybe just one or two of our funds that slot into their overall portfolio and risk profile.

If you are younger, or can accept higher risk, then the Opus Global Growth fund should produce higher returns through the cycle, but comes with higher volatility. If you want to add some rocket fuel to your portfolio, an allocation to the world’s most exciting revolutionary tech names through our US Technology VIP fund, can make a big difference - we have some very happy investors in that strategy already. Our Managed Income fund (MINC) as the name suggests, will give you an income in the knowledge that you are taking lower risk than our balanced fund, OGF. You can also use MINC as a lower risk way of accumulating capital.

Please remember we are always up to talk about these things – please reach out to any of the client team in the cc line, or ping me an email. There are no stupid questions anymore, just angry partners if we get this wrong.

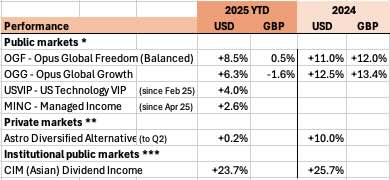

Performance – “green everywhere”

All the funds ticked up this week as the S&P500 reached new all-time highs. Journalists like to make a big deal out of new highs, but if you think about it logically, the only way we all make money in the long term is if the markets make new highs continually. So it’s not the excitement some people would like to make of it – it’s actually just a good thing.

Capital at risk. Source: * Estimates Freedom Asset Management as at 6/9/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch date of USVIP 10/2/25, ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** FT Markets as at 6/9/25, I shares.

Our articles this week:

- Cody Willard, adviser to the US Technology VIP fund, writes about “Why we stick with the revolution investment playbook”

- Charles Harris, Investment Analyst talks about some of the latest news in the European defence industry in “Building NATO’s Northern Front Line”. As readers will know, we were early investors in the defence theme in our balanced strategy which has played out very well for us.

Please scroll down to read the articles.

I am in London and Guernsey this week, wherever you are let me wish you a peaceful and prosperous week ahead (and as tempting as it may be, don’t sell the kids!)

All the best,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111* // M: +971 585 050 111 // M: +852 5205 5855* (*also WhatsApp)

--------------------------------

“Why we stick with the revolution investment playbook”, 8/9/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

There isn't one right way to invest. As we might say in rural New Mexico, "There are more ways than one to skin a cat." Warren Buffett, George Soros, Jim Simons, Peter Lynch, and Paul Tudor Jones radically diverged in their approaches to investing, and all of them were successful. Many others have attempted to replicate the success of the greats to no avail. That's why we have to pave our own way, while also attempting to learn as much as we can from those that came before. Regardless of the investing method employed, discipline, flexibility, conviction, hard work, and a little luck are universally required ingredients for a successful investing career.

The Revolution Investing approach we've refined over the last 20 years or so is unique to us and it's been successful (knock on wood). While we are constantly refining how we do what we do, our main job is to stick to the playbook that's worked so well for us over the last two decades. In this article, we wanted to lay out why we invest the way we do, and compare that to some of the other common investment strategies in our space. This isn't an exercise in self-aggrandizement, it's simply us codifying what we do.

Our style of investing, what we often call "Revolution Investing" is unique in the marketplace. If we could sum up our investment process, it would go something like this:

We invest in the companies building the most Revolutionary technology on the planet with highly differentiated business models and tremendous growth opportunities, while also paying extraordinary attention to valuations, economic cycles, and the trends in the broader markets in order to protect against downside risk.

Right now, most investors face this dilemma:

- Option 1: Chase disruptive tech or "innovation" with little valuation discipline or cycle awareness → huge drawdowns.

- Option 2: Hide in passive indexes → never beat the benchmark.

- Option 3: Avoid tech altogether → miss the most important wealth-creating trends of our lifetimes.

Our style really sits somewhere between Option 1 and Option 2. Most investors face a false choice between avoiding Revolutionary technologies, chasing them speculatively, or passively owning the market. Our process bridges that gap: we build core positions in proven leaders, actively manage around cycles and valuations, and selectively add exposure to the next generation of companies with true 10x–100x (or more!) potential.

So what makes our style different? When considering our Revolution Investing strategy at first glance, it might sound sort of like "thematic" investing. Google defines thematic investing as "an investment strategy that focuses on identifying long-term, macro-level trends and investing in companies that stand to benefit from them." This is basically the Cathy Wood approach. She identifies big trends that she is excited about – AI, energy storage, genomics, etc. – and then buys a bunch of companies that are playing in that trend.

The problem with a purely thematic approach is that it focuses more on the theme than the individual companies, and in our opinion often leads to the ownership of low-quality companies that are just riding the hype surrounding the theme. The themes that Cathy is following, like AI, are often the right themes, but then she ends up owning low-quality businesses like Teladoc Health (TDOC), 2U (TWOU), Pacific Bioscience (PACB), and others. For every good company in a theme – like Tesla (TSLA) for AI/Robotics – there are a hundred imitators, pretenders, and outright scams.

Under our approach, we employ a very high level of due diligence to ensure that the companies that say they are Revolutionary are actually Revolutionary. Moreover, we ensure they have the management prowess and balance sheet to execute on their Revolutionary vision. Here is the basic framework for how we evaluate individual companies:

Step 1: Know the Vision

- From the outset, we have to know the company’s Vision and the potential of what it could be in the long run.

Step 2: Monitor the Execution

- We require demonstrable execution on the Vision within a fixed amount of time (this is company specific of course).

- Our key performance indicators may include (1) major improvements in successive iterations of the company’s products/services (e.g. Moore’s-Law-type curves); (2) achieving targeted/modeled revenue growth; (3) improving profitability; (4) achieving scale in manufacturing; (5) rapid customer adoption; (6) ensure adequate balance sheet to achieve scale.

Step 3: Evaluate Management

- How much faith do we have that management can do what they say (or we think) they can do?

- Look at their history (e.g. Elon’s history of repeatedly achieving the impossible).

- Always “Bet on Brilliance.”

Step 4: Trust Our Analysis!

Think about the Robotics Revolution for example. People have been dreaming about autonomous humanoid robots since the 1800s, but no one has successfully produced them at scale yet. That's because this is an incredibly hard problem to solve, takes years of R&D, requires the most advanced AI in existence, and incredible manufacturing capabilities (and capital) to scale. There is really only one company today that has a reasonable chance of pulling this off (Tesla), and the next most likely competitors would be the companies building the AI platforms to power robotics like Nvidia and Google. We also have confidence in Elon's ability to achieve the impossible (he's done it a half dozen times already), and Tesla has the capital and manufacturing capabilities to do this at scale.

And while we do make speculative bets from time to time, the bar for a venture-style company to make it into the portfolio is extremely high (they have to make it through the same framework above). Moreover, we never chase hyped up theme/meme stocks just because they happen to be in a sector we are interested in.

Essentially, our avoidance of overvalued, hyped-up, or scammy companies is one of the primary ways we manage risk. In the long run, we know that the stocks of good companies with growing earnings will perform well, so we aren't really worried about short-term draw downs (we usually buy more). And while we aren't going to nail every top, by avoiding trashy companies, we can protect the against massive, permanent drawdowns. Remember, the ARK Innovation Fund (ARKK) is still down 50% from its all time high while the QQQ is up about 73% since then:

Source: Yahoo Finance

On the other end of the spectrum, traditional "value" investors obsess over near-term valuation metrics like EV/EBITDA, price/book value, FCF yield, etc. However, these metrics cannot account for the growth potential present in Revolutionary companies. This nearsightedness leads most value investors to miss out on some of the most incredible opportunities in the market. As I often say, all investing is "value" investing (no one consciously seeks to pay more than their estimation of a company's fair value). But many value investors don't have the vision to see how a company that looks expensive on paper today can actually grow revenue and earnings over the long term, in which case it might look quite cheap on a five, or ten year basis.

To arrive at a sense of fair value, we build financial models for every company we own looking out five, ten, and even fifteen years. Typically, we'd like to see a company have a five-year price/profits ratio in the single digits, and when we put a future multiple on those earnings, we are looking for an annualized return of 20%+. Of course, some of the most speculative bets require us to look out even further, and in those instances we have to size the position appropriately to account for the additional risk.

Like so many other things in investing, determining whether a company is fairly valued or not is an art, not a science. Every company is different, and the valuation they command depends on their unique positioning in the market. But our models help us visualize how a company succeed, and if they do succeed, whether we will earn an adequate return on our investment based on the current purchase price. Our models may end up being wrong, but they keep us grounded and at a minimum keep us from wildly overpaying for a company.

The difficulty of investing in Revolutionary tech without overpaying for growth has left a lot of investors choosing a third option: index investing. Index investing seems to offer the best of both worlds. American tech companies dominate the indices, and a lot of people are content to ride the indices as they've performed quite well on the backs of the dominance of American tech. So they get exposure to growing tech trends while avoiding the most speculative corners of the market.

This approach is fine for a lot of people, but it lacks exposure to some of the undiscovered, Revolutionary tech names that are not appropriately represented in the indices. Moreover, index investing fails to capture a lot of the value that we can capture when we get big dislocations in the megacap tech names that we see from time to time. This is where our approach active management can help drive superior returns. We are constantly assessing our positions against the market and "trimming" and "nibbling" as the opportunities present themselves.

Moreover, when the dislocations get extreme, we take the opportunity to load up on our favourite names, making high-conviction, concentrated bets on the biggest and best companies when their stock prices are getting punished by the market. You would think that as large and dominant as these companies are, the market would never sell them off, but it's amazing how often these megacap tech names get beat up and crash for one reason or another.

Think of our Google investment earlier this year for example. We were pounding the table on Google when the stock was around $160 in May of this year. At that time, the stock was down around 23% from its recent highs, and was significantly underperforming the indices as everyone was worried about the AI threat to Google's search business. We've owned Google for a very long time, know the business extremely well, and when we did our homework, we were more confident than ever in Google's AI strategy. We saw an opportunity to load up on one of our favourite names at a cheap valuation (about 15 forward p/e, five-year p/p of 7) that is also at the forefront of building out the Revolution we are most excited about at present (AI). We made Google our second largest position at that moment.

Last week, Google put in a new all time high after the Federal judge overseeing the antitrust trial ruled that Google didn't have to sell its Chrome browser or divest the Android operating system. We continue to think this is a stock that has a lot of room to grow over the next ten years or so as the company is one of, if not the leading AI company.

The point of the Google story is that there is a lot of opportunity to outperform the markets by actively managing our megacap exposure. Google is up about 43% since the date of our Deep Dive, compared to just 17% for the Nasdaq 100 ETF (QQQ).

Of course, we are not perfect and we have made mistakes (and unfortunately will occasionally still make mistakes) – but acknowledging those mistakes and fixing them is part of the process. But over time, we are confident that our approach to Revolution Investing will deliver outperformance compared to the indices, the average tech/innovation funds, and the old-school value funds. We might not catch every 10- or 100-bagger in the short run, but we also expect that we won't own the overhyped stocks that end up crashing 90%+ from their highs and never recover.

At the end of the day, investing is an art, not a science. We've developed a system that works for us, and our main job now is to believe and trust in that system over the long term to make superior returns for our investors.

Cody Willard

--------------------------------------

“Building NATO’s Northern Front Line”, 8/9/25

By Charles Harris – Investment Analyst

Last week marked a pivotal shift for European collaboration as the UK cemented its role as a principle naval partner to Scandinavian allies through two major, yet distinct, frigate export deals. The UK Ministry of Defence announced that it had landed its largest warship contract to export at least five Type 26, advanced anti-submarine warfare (ASW), frigates to Norway in a contract worth GBP10bn (USD13.5bn), it was also later revealed that Denmark and Sweden were in advanced talks with the UK to purchase the Type 31, general purpose, frigates. This heralds a new era of naval cooperation and bolsters the UK’s defence industry.

Figure 1 - BAE Systems Type 26 Frigate – aka ‘Global Combat Ship’

The Anglo-Norwegian Alliance - The Anti-Submarine Partnership

The Norwegian frigate deal is the centrepiece of the new alliance. The Norwegian Royal Navy will be equipped with 5xType 26 frigates, BAE Systems’ Global Combat Ship with the first delivery expected in 2030. The UK’s Type 26 programme will remain unchanged, first delivery is expected in 2028 and will receive all 8x ships during the 2030’s. Together with the Royal Navy’s ships, they will operate a combined fleet of 13 anti-submarine frigates “to detect, classify, track and defeat hostile submarines” (MoD). The deal is not only Britain’s largest warship deal, but also Norway’s biggest defence capability investment to date - a significant win for the British defence industry, as it beat bids from French, German and US contractors. But this is a deal where shared geography and pooling of resources is everything.

The frigates will be constructed by BAE Systems, the primary contractor, at its shipyard in Glasgow.

Strategic Significance - This deal is fundamentally driven by the critical need to enhance Anti-Submarine Warfare (ASW) capabilities in the High North; Norway is NATO’s monitor for a 2 million square km area in the North Atlantic used by Russia’s northern fleet of nuclear submarines. For NATO, it is also a crucial investment to counter increased Russian submarine activity near vital undersea infrastructure. A notable element of the agreement is that the vessels will be “as identical as possible” allowing the two Navy’s to operate as a unified force, sharing logistics, training, and tactical procedures.

Economic Benefit - The deal is a triumph for the British shipbuilding industry, securing around 4,000 jobs, including 2,000 in Scotland, and supporting 432 domestic companies. For Norway, the agreement is underpinned by a comprehensive industrial cooperation plan, ensuring that investment equivalent to the acquisition's value will flow back into the Norwegian economy.

Canada and Australia have also selected variants of the Type 26 frigate for their own Royal Navies – opting for the River class destroyer (Canada, 15x vessels) and the Hunter class frigate (Australia, 6x vessels) as opposed to Norway’s selection of the City class frigate.

The 'Arrowhead' Alliance - Flexible Naval Power Projection

In contrast to the Norway deal, the UK's collaboration with Denmark and Sweden centres on the general-purpose Type 31 frigate - Babcock’s Arrowhead 140. Denmark is expected to finalize an order for 3x frigates and may seek to build additional vessels domestically under license. Sweden on the other hand is considering a purchase of 4x vessels; however, the deal is slightly more complex, as it mulls over a competing offer from France for its FDI frigates.

The Type 31’s very existence stems from the high cost and specialised design of the Type 26, the Royal Navy initially ordered 13x Type 26’s in 2015 and revised it to 8x as it was deemed unaffordable – the Type 31 filled the void. The Royal Navy have 5x under construction with Babcock all due to be ready by 2030.

Strategic Significance - The Arrowhead 140 provides a modern, cost-effective, and versatile general-purpose frigate. Adoption by Denmark and Sweden aims to bolster security in the strategically complex Baltic Sea and North Sea regions. The frigate's modular design allows each navy to tailor the vessel to its specific needs, from maritime patrol and surveillance to participating in international operations.

Economic Benefit - For Babcock’s Rosyth shipyard, the combined Danish and Swedish orders could be worth up to GBP1.75bn(USD2.4bn), representing a significant boost for UK exports. For Denmark and Sweden, the Arrowhead 140 offers an efficient pathway to fleet modernization. The design’s flexibility may also allow for significant local industrial involvement in the construction and outfitting phases, supporting their respective domestic shipyards.

A New Era of Strategic Partnerships, or finally we get to fight with the Vikings?!

These new deals are far more than a number of lucrative defence contracts; these are the foundational pillars to a more robust European security architecture in the High North. The deals forge a de facto ‘Northern Fleet’ of technologically advanced and interoperable warships that will operate on common platforms and training standards, creating a powerful deterrent to maritime aggression. This new model of "partnership procurement" is likely to serve as a blueprint for future defence collaboration amongst NATO allies, moving beyond transactional sales to the co-creation of shared security ecosystems.

It has often been said that Europe’s greatest military weakness is it the fragmented nature – these agreements symbolise the beginning of the end of this time old vulnerability.

Looking forward, the UK’s defence industry, specifically naval shipbuilding, is now positioned for international competitiveness and the continuous production lines for the two separate frigate classes will support thousands of jobs and hundreds of businesses. The UK has not only revitalised its domestic shipbuilding industry but simultaneously placed itself at the epicentre of NATO’s maritime resurgence.

Charles Harris

--------------------------------

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.