Weekly Newsletter

Freedom Calls: 4/8/25, “Arise King Donald IV of Scotland…"

by

Freedom Asset Team

August 4, 2025

7 Minutes

Freedom Calls: 4/8/25, “Arise King Donald IV of Scotland…"

From the team at Freedom Asset Management

“Donald” in Scottish means “Ruler, or king of the world”. So it was slightly amusing, and not without irony, to see Mr Trump welcome Sir Keir and Lady Starmer to his Turnberry golf residence in Scotland. It looked very much as though the protocols had been reversed - see below - but, hey this is Mr Trump and Starmer is smart enough to just roll with it in return for a better trade deal than the EU!

Picture credit: The Washington Post, July 2025

Might Trump be right?

There is growing discontent and disbelief amongst financial journalists that Trump’s tariff policy might actually be working. That is to say that many countries have now folded and agreed to: (1) give US businesses (better) access to their markets, (2) pay (increased) tariffs on exports to the US, and (3) buy lots of US weapons. And this is all whilst the US continues to keep growing at a meaningful pace. The FT reported 16/7/25 that the US had collected an extra $50bn in customs revenues since the start of the recent tariff war, "at little cost".

Trump’s tariff announcement on Friday (on all those countries that have no yet signed an agreement) was unhelpful for markets, but it keeps with the programme and we should expect those countries to come back into the negotiation room in due course, with the possible exception of China.

And make no mistake these tariff negotiations are about China. Whether it be the transshipment tariff of 40% on Vietnam, or the fact that Ursula van der Leyen was able to strike a deal on behalf of the EU. Politico claimed last week the EU deal was due in large part, because van der Leyen had played hardball with China's President XI a week earlier at what was supposed to be a celebration of 50 years of EU/Chinese diplomatic relations.

Trump’s focus is on China. If there is going to be a war over Taiwan, (and we all hope there isn’t) the last thing Trump wants is the US filling China’s war chest ahead of time, whilst China also depletes US manufacturing capability. By signing trade deals and reminding everyone to buy US weapons and technology, as politically incorrect and economically impure as it may be, at least Trump is tipping the scales and probabilities back in favour of the US should that day, or any other day in the South China Sea, occur.

We always have to reflect that Russia and China can play a very long game, unworried about election cycles. In the West, we live by short political cycles, social media and hysterical journalism, which is why you have to be in a hurry to get things done…. hence the big marker pen and the executive orders.

This week’s articles:

- Cody Willard talks about "Revolution investing to the moon” and how we are looking at investing in space stocks

- Charles Harris and Laurence Gee write about US exceptionalism and ask whether any cracks are starting to appear. Laurence has been with us over the summer in our Guernsey office working on the investment research team. This is an excellent article.

Please scroll down to read the articles.

Performance - a little tariff wobble on Friday

Friday was a wobbly day, having been a good week until that point - due to Trump’s renewed tariff announcement and some weak-ish US consumer numbers.

Source: * Estimates Freedom Asset Management as at 3/8/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and also launch date of USVIP 10/2/25, ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** FT Markets as at 3/8/25, I shares.

I always like to think that occasional wobbles provide helpful entry points for money sitting on the sidelines. And we should always be mindful that in these summer weeks of August, market volumes are typically lower, which can sometimes lead to price distortions. Importantly, for sterling thinking investors (and just in time for the summer holidays of course), sterling has started to weaken significantly from $1.37 to $1.32 in the last 10 days or so. We expect more sterling weakness.

This week, I am enjoying a view out over the beautiful bay of La Baule in France. I hope you are enjoying the summer wherever you are, and do reach out to the team if there is anything you would like to talk through.

In September, we have our US tech team on tour - Cody Willard and Bryce Smith - visiting London, Guernsey, Abu Dhabi, Dubai and Hong Kong, so make sure to grab some time with them. They are highly knowledgable and equally entertaining investors - investing in technology can be highly rewarding and does not need to be dull!

Wishing you a wonderful and peaceful week ahead,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111* // M: +971 585 050 111 // M: +852 5205 5855* (*also WhatsApp)

----------------------------------------

“Revolution investing… to the moon” 4/8/25

By Cody Willard, Adviser to the US Technology VIP Fund

We're living through a time in which the biggest economic Revolutions in human history are developing at an ever accelerating pace.

Clearly, The AI Revolution is front and center right now as the largest, smartest, most profitable US tech (not sure I need to include this “US tech” descriptive, as US tech companies are the largest and most profitable, non-government-owned companies on the planet companies on the planet anyway) companies are constantly increasing the capital expenditures that they are spending to build The AI Revolution. These are not some Pets.com startups wasting venture capital money. These are companies that know how to win at the highest stakes poker games in the world and have been winning The PC Revolution, The Internet Revolution, The App Revolution, The Cloud Revolution, etc already. And they clearly wouldn’t be spending trillions, literally trillions, of dollars on building the infrastructure and LLMs and other inputs that The App Revolution is being built upon.

The amount of innovation, services and applications that we’ve already seen in The AI Revolution are clear precursors of all the wondrous productivity, efficiency, creativity and artistic wonders that we will see in literally every single white collar job, every single corporation and many small businesses over the next two to ten years.

Much of the current VIP Tech Fund is built around these AI Revolution companies and that’s not a coincidence, obviously. We want to be concentrated in the companies that are about to change the world and this AI Revolution is certainly that. But it’s important for Revolution Investors to always be looking ahead into the future trends that will be creating trillions — nay, tens of trillions of dollars of economic value in the next decade or two.

And that’s exactly why we own companies that have exposure to The Robotics Revolution, as it is the next — and perhaps even larger — economic Revolution that’s about to change the world, even if it’s not quite ready for prime time just yet. Tesla, Nividia, Google, Apple and other companies in the current batch of VIP Tech holdings will certainly also be major contributors to and beneficiaries of The Robotics Revolution, but we also hold Texas Instruments and Qualcomm as investments because every single robot will need dozens or even hundreds of analog chips (that is, Texas Instrument chips) and many of those same robots will also need 5G/Satellite/Broadband connectivity chips (that is, Qualcomm’s modem chips) and mobile CPU chips (that is Qualcomm’s Snapdragon in many cases, although there are plenty of competitors in the CPU market overall).

Although The Robotics Revolution is certainly starting to warm up, it’s still barely the first pitch of the first inning in The Robotics Revolution. But starting next year, we’ll begin to see some commercial sales and maybe even some consumer hit products from The Robotics Revolution. And over the next few subsequent years, we’ll see hundreds of billions of dollars of economic growth from The Robotics Revolution and by the year 2030 or so — just five shorts years from now — we’ll be seeing robots, especially humanoid robots, changing the world, making it safer, healthier and more prosperous.

Meanwhile, The Space Revolution, is developing in its own right although it’s got a bit of a slower ramp up than either The AI or The Robotics Revolution.

That said, as launch costs have to continue to collapse towards de minimus levels so that launching people into space becomes as routine as sending people on a first class ticket around the world in coming years, we’ll see the Space Revolution take off (sigh, sorry for the pun again). That’s not as crazy as it sounds, because launch costs have already dropped 99.9% over the last twenty years as SpaceX has Revolutionized the industry. SpaceX’s Starship will be another major Revolution as it will drop launch costs another 99% as its reaches scale, probably sometime after 2030. As the cost and ease of reaching space become comfortable for millions of people and hundreds of thousands over the next five years after that, The Space Revolution will be going into orbit itself (sorry, obviously another easy space pun).

At 10,000 Days Capital, we’ve spent the last ten years preparing for The AI Revolution and for the last five years, we have been deep in the weeds traveling to meet both Robotics and Space Revolution companies and learning how to/preparing to invest in them. I think it’s a bit early for the market to recognize how big of an opportunity The Robotics Revolution will be for both Texas Instruments and Qualcomm and other companies that drive it but I think that will start to change over the next year as the Robotics Revolution heats up. On the other hand, I think the market has taken most publicly-traded space theme stocks to the moon valuations, despite it probably being several years away from seeing the best space investments hitting the public markets.

I think we will have much better pitches, much more developed/softer businesses from The Space Revolution in which to invest in another five years or so. That said, I do think I am open to adding at least one or two Space Revolution stocks to the portfolio sooner rather than later, just to get our toes in the water (not sure how that metaphor works as a space analogy, but you get my point!).

Anyway, I am, without a doubt, more excited than ever about The Tech Revolutions we are invested in — and about to invest in. The AI, Robotics and Space Revolutions are, after all, going to be worth tens of trillions of dollars of value each over time. Hang on tightly, we are about to see the world’s economies and societies change faster than ever before. We’re ready for it. Are you?

Cody Willard

——————————————

"US Exceptionalism - are any cracks appearing?”, 4/8/25

By Charles Harris and Laurence Gee - Investment team

The notion of US exceptionalism — once viewed as unshakeable by many— is increasingly being questioned by investors. As the world grapples with political realignment, monetary policy divergence, and record levels of public debt, a familiar paradox has emerged: Can a global hegemon remain dominant without compromising its own internal resilience? This is the American version of the Triffin dilemma — the tension between supplying the global economy with liquidity through deficits, and maintaining fiscal and monetary discipline at home.

Inflation remains moderate, printing at 2.7% in June. The labour market is firm, with unemployment stable around 4%, and GDP growth has broadly returned to pre-COVID trendlines. On the surface, this is a resilient macro backdrop, but are there any cracks starting to appear?

At the most recent FOMC meeting, two Fed governors dissented for the first time in over 30 years — calling for a rate cut against the consensus. Both were appointed under the first Trump administration, raising uncomfortable questions about political influence within what has historically been an independent institution. If the perception takes hold that monetary policy is no longer technocratic but partisan, the long-term credibility of the Federal Reserve — and by extension, the U.S. dollar — could be compromised.

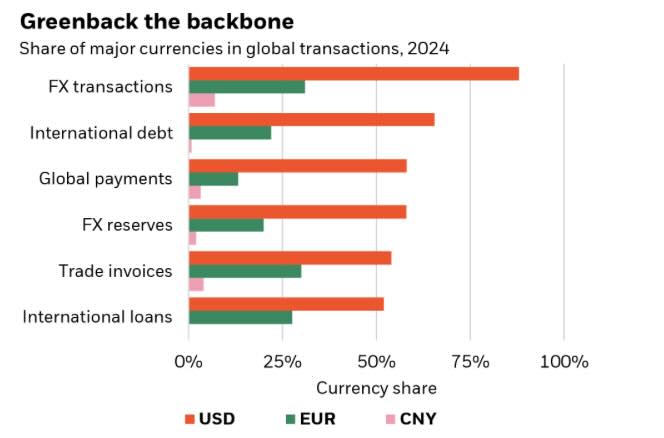

None of this changes a simple fact - the dollar remains the global reserve currency and will continue to for a very long time. As Barry Eichengreen puts it, “The eurozone lacks fiscal unity, China lacks convertibility, and no other currency has the institutional depth.” The chart below demonstrates just how dominant the US dollar is as a currency for global transactions, with the Euro a distant second.

Source: BlackRock Investment Institute, July 2025

But while there is no immediate alternative, there is now a growing desire for one. Central banks, especially in the Global South, have been quietly increasing gold reserves; at the same time, the dollar’s role in global trade is being reevaluated amid tariff policies and shifting geopolitical blocs.

Amid these challenges, the US retains one significant—and often underappreciated—structural advantage: energy security. The US is now the world’s largest producer of oil and gas and has remained a net energy exporter since 2019. This insulates the economy from many of the supply shocks plaguing Europe and Asia and provides a meaningful cushion against geopolitical volatility. As we’ve seen in recent months, energy-importing economies remain vulnerable to chokepoints—from the Red Sea to the Taiwan Strait. The US is far less exposed, giving it a strategic buffer that supports not just growth, but asset stability.

The U.S. also continues to lead the world in research, development, and intellectual property creation. It attracts the lion’s share of global venture capital and remains at the forefront of technologies such as AI, biotechnology, and advanced manufacturing. A younger and faster-growing population—bolstered by immigration—further supports long-term productivity growth and domestic consumption.

While China is closing the gap in select areas, the US innovation engine remains without peer in terms of ecosystem scale, institutional strength, and capital depth.

Against this backdrop, however, fiscal sustainability is becoming harder to ignore. US federal debt has now surpassed 120% of GDP, and interest payments have overtaken defence spending—an unprecedented development. With deficits projected to exceed 5% of GDP for the foreseeable future, there is growing concern that investor tolerance for structural imbalances may be reaching its limit.

Markets are beginning to price in this risk through higher term premiums, weaker dollar demand in some regions, and increased demand for inflation protection.

Exceptionalism does not vanish overnight. But it can erode quietly—through fiscal complacency, political interference, or loss of institutional credibility. We believe the U.S. still holds a superior structural position, but that position is no longer unassailable. In this environment, vigilance, balance, and forward-looking diversification will be critical. The rules are not broken—but they are shifting. And at the appropriate time, portfolios must be prepared to shift with them.

Charles Harris and Laurence Gee

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.