.jpg)

Weekly Newsletter

Freedom Calls: 27/4/26, AI is winning everywhere…

by

The team at Freedom Asset Management

April 27, 2026

5 Minutes

Freedom Calls: 27/4/26, “AI is winning everywhere… "

From the team at Freedom Asset Management

After a busy week of travel, the weather in Guernsey made for a glorious calm spring weekend, see below, which felt a bit like reading the performance numbers on the funds after all the market volatility we have seen in recent weeks:

Pictured: (L) Early morning over Castle Cornet, and the Islands of Herm and Jethou, (R) L’Ancresse Beach, April 2026

Two weekends, two games of rugby… and AI

I was invited to the local rugby game on Saturday by one of the legal firms we use here in Guernsey. It was not exactly Hong Kong's Kai Tak stadium with a 55,000 capacity crowd (in fact, think more like 400 people), and the standard of rugby was perhaps not quite the same, but this game like so many others, was a great opportunity to bring together like-minded middle-aged men to discuss the world’s most pressing problems over a cold beverage or two. The most animated subject was about AI in the workplace.

For the lawyers around the pre-match table, AI is very much here and is used to help draft agreements, to check for omissions, or to ensure that capitalized terms are correctly referenced and standardized across documents - tasks that previously may have taken many hours or days can now be completed confidently in a matter of minutes.

But there are pitfalls of AI in the legal world and they are not so obvious:

Loss of legal privilege - the moment any information is uploaded to a non enterprise version of ChatGPT, as part of a prompt or question, you have just lost legal privilege on that information. Apparently that is in ChatGPT's terms of service. It might be easy for senior people to understand and remember that, but what about the juniors trying to do some extra research over the weekend on their home laptops…, and

Your AI searches are discoverable in a legal process - this is really important, and the point here is that we are taught to be very efficient in our prompts - so you are more likely to spell out your intentions in an AI prompt, vs a Google search, e.g. “how can do I avoid tax in Germany on this transaction?”. By definition, in a court of law, this shows your intent - and this could be tricky to come back from.

Both of the points mean that we need to make sure our teams know the rules of how we can safely use AI in our businesses.

Iran - best left for another week

I am going to keep it very brief on Iran this week. There has not been much movement. This should not really be a big surprise - as we said last week, Trump can play the long game here on the Strait of Hormuz and the Iranians are fighting amongst themselves to decide who will attend the peace talks. Our sources say we should expect this negotiating period to last for a month or so.

But importantly, whilst we are waiting, the ceasefire will stay in place, and that is all that US markets care about. Back in Abu Dhabi the team are back in the office, children are back to school and life has returned to normal. Sometimes getting back to normal is a great thing.

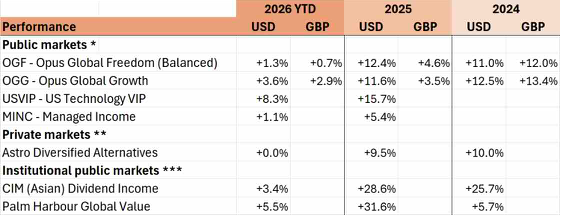

Performance - AI is back!

Last week saw a break-out in tech names so US Technology VIP (USVIP) is powering ahead and is now up +8.3% YTD - which is a reversal of around +18% in 4 weeks. This is an all-time high NAV on this fund, so that means by definition every investor in this fund is making money. Remember all-time highs are good things, (despite what you might read from click-bait seeking journalists), because you need to keep breaching all-time highs to make money on any investment in the long term - it’s just simple maths and it's normal.

The chart above (from the WSJ 26/4/26) shows how the different US indices have performed. We often use the S&P500 as a reference point when we think about levels of risk. Outside of USVIP, the funds are doing what they should be doing for the different levels of risk they are taking and you can see a real differentiation in outcomes now. Importantly, all our funds are in positive territory YTD and we see a clear path forward for the return to risk taking - in other words: a good time to invest or top-up.

(For performance disclaimers see foot of email below)

Our article this week:

Canaccord’s Justin Oliver, adviser to the Opus Global Growth Fund writes for us about currencies, in “what do geopolitics mean for currencies"

Global Small Cap Value - a webinar with Palm Harbour Capital's Peter Smith

On the institutional distribution side of our business we have taken on a remarkable classic value manager. London-based Peter Smith at Palm Harbour Capital runs a UCITS fund that seeks out the most interesting undervalued small cap stocks that nobody else owns - from telecoms companies in Austria to battery manufacturers in Korea. I caught up with Peter last week in London. In a world of ETFs, large caps and passive, he is a welcome breath of fresh air for active allocations. The fund is now over $60m - and one of Freedom's UK institutional relationships has just placed $13m into the fund. Whilst this fund is targeted at institutions, as it is a UCITS fund, it can be bought over any good brokerage account with no minimums.

You can see from the performance table above the fund is up +5.5% YTD. We are hosting a webinar with Peter this week, if you would like to learn more please feel free to sign-up below:

When: April 30, 2026 15:00 London

Topic: Palm Harbour Global Value Fund Webinar - Q1 update Fund Manager Peter Smith and Equity Analyst Konstantinos Kontos

Register in advance for this webinar:

https://us06web.zoom.us/webinar/register/WN_Bn3NZcGsRu6sRA31sXXntQ

Cody Willard (US Technology VIP Fund) in Europe

This week we have Cody Willard in London, Germany and Guernsey - and I shall be with him in London and Guernsey. We still have a couple of slots free if you would like to meet him, please let me know.

Wherever you are please let me wish you a safe and prosperous week ahead,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

————————————————

“What do geopolitics mean for currencies”, 27/4/26

By Canaccord’s Justin Oliver, Investment Adviser the Opus Global Growth Fund

The geopolitical backdrop has, once again, become a dominant driver of currency markets, with the conflict in the Middle East challenging long-standing assumptions around safe havens. While the U.S. dollar has historically strengthened during periods of heightened uncertainty, recent price action suggests that this relationship is weakening. Instead, a more nuanced framework is emerging; one that blends cyclical growth exposure with selective defensive positioning.

Despite the escalation in geopolitical tensions, the U.S. dollar has only appreciated modestly. Both the DXY index and broader trade-weighted measures remain toward the lower end of their multi-year ranges, an outcome that is somewhat surprising given the typical “risk-off” playbook. This subdued response reflects deeper structural issues. Elevated policy uncertainty in the United States, combined with ongoing economic and interest rate headwinds, has eroded the dollar’s traditional safe-haven status. In contrast, currencies such as the Japanese yen and Swiss franc are increasingly being viewed as more reliable defensive assets. At the same time, global trade dynamics remain supportive of a different set of currencies. Export-oriented economies, particularly those linked to resilient global demand, are beginning to outperform, reinforcing the case for a diversified FX approach.

At the heart of any FX strategy is a relatively straightforward assumption: the United States is likely to seek a de-escalation path to prevent further damage to economic sentiment. The global economy entered this period of conflict in relatively solid shape, supported by accommodative monetary and fiscal policies. To date, economic indicators have not shown meaningful deterioration. However, the duration and trajectory of the conflict remain critical. The longer tensions persist, the greater the risk of a slowdown in global growth.

There appears to be three potential scenarios in how the conflict will evolve:

Continued tension without escalation

This “status quo” scenario limits extreme downside risks, while maintaining elevated uncertainty. Growth remains supported, but business investment decisions may be delayed. In this environment, the U.S. dollar is likely to remain broadly flat to slightly weaker, while pro-growth currencies gradually outperform.

Ceasefire and improved clarity

A move toward meaningful negotiations would boost confidence, lower energy prices and reinforce a risk-on environment. This is the most favourable outcome for trade-sensitive currencies, with the euro, Singapore dollar and select emerging market currencies likely to lead gains.

Escalation of conflict

A breakdown in negotiations would trigger a sharp deterioration in sentiment, potentially leading to a prolonged downturn. In this case, defensive currencies, particularly the yen and Swiss franc, would outperform, reflecting their safe-haven characteristics.

A blend of the first two scenarios may be the most likely outcome. With political incentives aligned toward avoiding a prolonged conflict, particularly in a mid-term election year, the probability of a severe escalation appears lower. Notwithstanding this, there are several forces which would argue for a weaker US dollar over the medium term.

First, global growth dynamics are shifting. While the U.S. economy remains resilient and supported by strong consumer activity and a relatively healthy labour market, other developed economies are beginning to close the gap. This convergence in growth rates historically favours non-U.S. currencies.

Second, interest rate differentials are no longer as supportive. As other central banks adopt relatively more hawkish stances compared to the Federal Reserve, the narrowing spread in real yields is putting downward pressure on the dollar.

Third, valuation remains stretched. On a real trade-weighted basis, the dollar is still approximately 15% above its long-term trend, with purchasing power parity models indicating similar overvaluation. This leaves limited room for further upside and increases the likelihood of gradual depreciation. Importantly, the dollar is no longer technically oversold, having rebounded from earlier extremes. Momentum and positioning indicators now sit closer to neutral, removing a potential support that had previously underpinned the currency.

USD remains expensive

Against this backdrop, currencies can be broadly grouped into three categories: pro-growth leaders, defensive hedges and structural laggards.

The most attractive opportunities lie in currencies leveraged to global trade and improving growth dynamics. In this regard, the euro stands out. It has shown resilience despite higher energy prices and benefits from improving manufacturing conditions, particularly in Germany. Fiscal support measures are also likely to provide an additional tailwind.

Meanwhile, the Singapore dollar offers a high-beta exposure to global trade. With no evidence of deterioration in relative growth trends, it remains well positioned to outperform if the global expansion continues. A basket of emerging market currencies also presents opportunities. While these currencies have faced pressure from capital outflows and energy concerns, many economies are more resilient to higher oil prices than commonly assumed. Within this group, currencies such as the Brazilian real, Korean won and Malaysian ringgit are particularly attractive due to favourable domestic dynamics and valuation support.

EM currencies have been relatively resilient

While the base case is constructive, geopolitical risks remain elevated. As such, maintaining exposure to defensive currencies is prudent. The Japanese yen is notably undervalued, trading at levels not seen in decades. Although it has underperformed in the near term, its risk-reward profile is compelling, particularly in the event of a global downturn. The Swiss franc also continues to demonstrate strong safe-haven characteristics. Its performance during previous periods of economic stress highlights its defensive value, and it remains a preferred hedge against downside scenarios.

The Japanese yen is extremely cheap

At the other end of the spectrum are currencies facing structural headwinds. Developed commodity-linked currencies such as the Australian dollar, Canadian dollar, New Zealand dollar and Norwegian krone, have largely moved sideways. High household debt levels and housing market vulnerabilities are likely to constrain both growth and interest rate potential over time.

Similarly, the UK pound remains range bound. Weak relative growth prospects and unfavourable interest rate dynamics limit its upside, while underlying economic and political challenges suggest further downside risks versus the euro. The Swedish krona, despite its sensitivity to global trade, is also constrained by aggressive monetary easing and domestic imbalances.

In this current uncertain environment, maintaining a balanced and flexible approach to currency allocation remains critical. While the U.S. dollar continues to play a central role, its position as an unquestioned safe haven appears to be moderating amid structural overvaluation, narrowing interest rate differentials and evolving growth dynamics, suggesting scope for gradual weakness. A diversified mix of pro-growth currencies, such as the euro, Singapore dollar and select emerging markets, offers exposure to improving global conditions, while defensive allocations to the yen and Swiss franc provide important downside protection. This combination of cyclical opportunity and defensive resilience is likely to be the best approach in navigating an increasingly complex and uncertain landscape. Opus Global Growth’s international equity allocation effectively reflects and implements this balanced approach.

Justin Oliver

—————————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 26/4/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 estimate takes the MCAS December 2025 estimate and deducts the estimated charges of the Astro feeder fund. *** Morningstar as at 26/4/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Unit 2117, Level 21, New World Tower 1, 16-18 Queen's Road Central, Hong Kong.

© 2026 Freedom Asset Management Limited.