Weekly Newsletter

Freedom Calls: 27/10/25, “Reasons to stay bullish and the overlooked robotics supply chain”

by

From the team at Freedom Asset Management

October 27, 2025

7 Minutes

Freedom Calls: 27/10/25, “Reasons to stay bullish and the overlooked robotics supply chain”

From the team at Freedom Asset Management

It was a “fresh” start to last week in Guernsey with a morning swim in the English Channel joined by our UK based colleagues. I will spare you that photograph, but pictured below, from the relative warmth of the Guernsey office (L-R): Robert Brown (Head of Risk and Compliance in Guernsey), Bill Francis (European Institutional Sales), Ramon Eyck (Investment Committee Member - MINC & OGF) and Alan Walker (European Institutional Sales). It has been a particularly strong year for our European Institutional team and it is always good fun to get the gang together to swap notes and stories over a variety of unhealthy dining options. This time was no different!

ADCP Portfolio Forum 2025 in Abu Dhabi

A couple of days later, we joined our favourite Sovereign Wealth Fund at the Abu Dhabi Catalyst Partners' Portfolio Forum, in the beautiful surroundings of the Louvre Abu Dhabi. Sandrine has captured many of the key messages in her article below.

Pictured below (L-R): Mubadala Capital's Simon Temple pointing to the Freedom logo, Sandrine Reynaud and Achim Kuessner - Freedom’s Non Exec Director in Abu Dhabi.

We are always grateful for the support we have received from Mubadala Capital’s ADCP, who have been strategic investors with us since 2019 when we launched the business in Abu Dhabi.

Performance - a strong bounce forward

Despite the best efforts of doom-sayers, the march forward has found its feet again - a case in point, defence stocks were back up 6% last week - and some of the previously wobbly tech stocks put on 4-5%. The “historic crash" in the gold price had subsided by Friday to be off less than 3% on the week. This does not mean we are complacent, it just means: don't believe the click-bait doom-sayers all the time.

Statistically of course, they will be right one day, but your opportunity cost of believing them every time they cry "wolf" is likely to cost you more in the long term than being invested throughout - that is, so long as you stay invested to catch the inevitable bounce back after whatever "doom" event happens.

If you have a long time horizon (5+ years), don't be scared by volatility - embrace it. If you have a shorter time horizon or just want to minimise your volatility, the Managed Income Fund (MINC) below might be a strategy to look at. Never be afraid to send in an email, or WhatsApp, or pick up the phone to your Freedom contact if you have any concerns about the strategy you are invested in - we love talking to our clients, always - and I promise you there are no stupid questions.

(For detail, please refer to disclaimer section below)

Things we are watching out for over the next few weeks:

- "Progress" seems to be the right word to describe China/US trade issues, but that can change on a dime/tweet

In socialist Britian, we are expecting another "soak-the-rich" budget, expect Sterling to reflect briefly on this, and then fall

Trump is trying to punish Russia on its oil exports to India, but Trump has told Saudi to keep pumping, so we are not expecting this to be a major event right now in terms of demand and supply of oil, but that could change

The Canadians have upset Trump on trade, so expect theatrics, but in the end there will be a sensible deal because, despite his bluster, Trump does actually like and need the Canadians, as we all do

Our articles this week:

- Sandrine Reynaud, Co-Founder and SEO of our ADGM business captures "The key messages from the ADCP Portfolio Forum 2025", which show the strength of Abu Dhabi as base to do business in the AI revolution

Derek Akkiprik on the investment team in Abu Dhabi discusses "GCC fixed income"

Justin Oliver, Adviser to Opus Global Growth (OGG), gives us his "Reasons to stay bullish"

Cody Willard, Adviser to US Technology VIP (USVIP) writes "The overlooked robotics supply chain is at an inflection point".

Please scroll down to read the articles.

This week, I am in Abu Dhabi and Dubai - in part with Justin Oliver, who will be giving client updates on OGG. Remember Justin is now based in the UAE, so much easier to catch up with for our UAE-based private clients.

Wherever you are, please let me wish you a wonderful and peaceful week ahead,

All the best,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

—————————————————

"The key messages from ADCP's Portfolio Forum 2025", 27/10/25

By Sandrine Reynaud - Co-Founder and Senior Executive Officer

UAE's Growth Engine: Investment, Infrastructure, and the AI Revolution

The recent ADCP conference highlighted the dynamism of the UAE’s economic landscape, showcasing significant growth in real estate, robust technological infrastructure plans, increasing private equity interest, and the transformative impact of Artificial Intelligence (AI) on asset management. The overarching theme was a strategy built on partnership, tolerance, and a forward-looking embrace of technology.

Real Estate: Aldar’s Exponential Trajectory

The afternoon started with an interview of Talal al Dhiyebi, CEO of Aldar, who framed the UAE as a story of economic development and partnership, with real estate serving as a direct "by-product" of this success. Post-COVID-19, Aldar has experienced dramatic growth, with sales surging from $1 billion in 2021 to a current $9 billion.

Aldar’s strategy is centered on creating integrated, themed lifestyle destinations, ensuring safety is paramount. Key developments include, as we have all seen, the Saadiyat cultural district, the Yas entertainment hub, and the ADGM financial district. Connectivity is a future priority, with a 28-minute speed train linking Downtown Dubai and Abu Dhabi expected by 2030.

This environment has made Abu Dhabi highly attractive to global capital, with 30% of Aldar's off-plan properties being sold to non-residents. Looking ahead, Aldar's strategic focus is to commoditize real estate to establish it as a formalized investment asset class.

Technological Advantage: Capital, Cost, and Data Centers

The session with Omar Ismail, Head of Technology at MGX, illuminated the structural advantages the UAE possesses in the tech domain. The region is positioned for a major shift from traditional search engines to AI. This transition is underpinned by significant institutional backing, with the UAE boasting an estimated $2.2tr+ in AUM collectively held by Sovereign entities like Mubadala, ADIA, and ADIC.

Crucially, the UAE offers a major cost advantage with cheap energy priced at approximately 6c/Kw, significantly lower than the 20c to 30c per Kw seen in other countries. This makes it an ideal location for energy-intensive technology infrastructure. The discussion pointed to data centers as a stable, long-term investment horizon (10-15 years), favoured over Large Language Models (LLMs) due to the reliable, clearer cash flow derived from long-term lease contracts. Furthermore, the region has demonstrated an inherent ability to build infrastructure fast.

Private Equity’s Strategic Pivot to the GCC

The Gulf Cooperation Council (GCC) is rapidly solidifying its position as an emerging new market for global Private Equity (PE) investors. Established firms like TPG, Bain, and General Atlantic (GA) who were on the panel, are expanding their focus, capitalizing on the region’s increasing strategic importance and development.

General Atlantic initially leveraged its regional presence by extending the reach of existing consumer portfolio companies, such as Joe & the Juice and Gymshark.

Now, the firm is directly investing in local champions like the direct-to-consumer eyewear retailer eyewa and the online platform Property Finder. Bain has accelerated its direct regional investing over the last two years. TPG is approaching the region by strategically linking its vast portfolio in India—particularly in healthcare and pharmaceuticals—to the GCC market and is establishing a presence in the UAE to facilitate this nexus.

AI’s Role in Asset Management: Augmenting Human Capability

Discussions with technology investors, including Brian Sheth of Haveli and Benoit Verbrugge of Clipway, detailed the practical integration of AI into financial processes. Firms like Clipway, a relatively new firm, are deploying AI to analyse deals and price portfolios, which has delivered substantial process improvement and higher-quality information. The consensus was that implementing AI is easier for newer firms unburdened by legacy systems.

The technology is seen as an AI agent for discrete, analytical tasks, while traditional software remains superior for deterministic functions and calculations. Critically, AI's limitations, such as the risk of hallucination, mean it will continue to require human oversight. Far from displacing roles, AI is expected to increase the analyst's ability and overall productivity, serving as a powerful tool to augment, not eliminate, human expertise.

A lot of food for thought for the Freedom team to digest and make the most of networking during the day.

Sandrine Reynaud

-------------------------------------------

"GCC Fixed Income: Yield, Duration, and a Measured Pause", 27/10/25

By Derek Akkiprik - Junior Investment Analyst

We are based in the Middle East and so investors naturally expect us to have a view on fixed income in the region, so here is our take on where Gulf Cooperation Council ("GCC") fixed income is at right now.

If 2025 has taught fixed income investors anything, it is that “quality carry” is scarce and contested.

And on that note, there is one candidate that is drawing fresh attention: the GCC hard-currency sovereigns. The evolution of GCC sovereign bonds into a semi-core fixed income asset class reflects both improved domestic policy frameworks and the global search for yield in a low-spread world. From a strategic perspective, GCC sovereign bonds offer a unique balance between yield and quality. The complex is now predominately investment grade and crucially benefits from hard peg to the US dollar that transmits U.S. rate moves while limiting currency volatility.

So, what does the investable universe look like? Think US dollar denominated sovereign (and quasi sovereign) notes from Saudi Arabia, the UAE, Qatar, Kuwait, Bahrain, and Oman; all of which is benchmarked and well covered by global indices and increasingly held by institutions. The UAE, Qatar, and Kuwait retain strong investment-grade profiles supported by substantial cash reserves and low leverage (debt).

These bond yields typically sit above U.S. government debt, reflecting a liquidity premium and oil-linked fiscal cyclicality, and yet remain far tighter than higher risk emerging market sovereigns. A crude way to phrase this would be that they have enough oil money to eat their mistakes. This dynamic has encouraged investors to view GCC bonds as a “middle-income safe haven” of sorts that offers incremental yield without the instability of higher risk emerging markets.

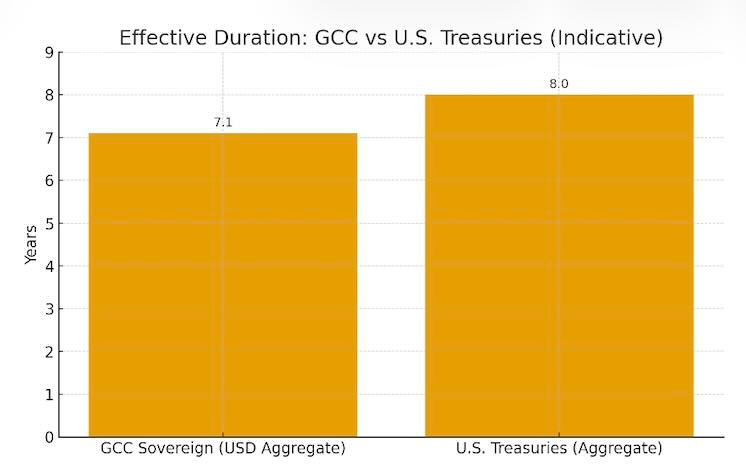

Duration is why the segment stayed on our radar through the Federal Reserve’s tightening cycle and with the Fed now in an easing phase, we remain in tune to it as a primary risk.

Curve dynamics, term-premium noise, and supply technicals can overwhelm the clean “cuts = duration rally” narrative.

Harvesting quality carry over taking outright rates beta is preferable in our view. GCC aggregates typically sit in the high 6-to-7-year effective duration range; useful context, but longer than we would choose to lean into at this point.

In practical terms, that could mean treating GCC sovereigns as semi-core exposure and sizing them to a portfolio’s duration budget rather than using them as the primary method to duration expression.

Despite progress, liquidity constraints persist; GCC sovereigns are not yet perfect substitutes for US Treasuries. These bonds are good, stable investments, but they are riskier and harder to sell quickly than US Treasuries, especially when the market is struggling. They can therefore be treated as a structural supplement, not a complete replacement.

Additionally, it is important to look at each individual issuer’s risk. Bahrain’s high public debt and thin cash reserves means they need sustainably higher oil prices to keep their bond yields low. Saudi Arabia’s vast infrastructure and state spending have the potential to deteriorate the wider fiscal position and warrant close monitoring. These risks don’t undo the case; they set the terms. Portfolio construction here is therefore about sizing and balance: it makes sense to overweight the core credits, and go smaller in the peripherals, and let index caps do some work.

The world has changed a lot since 2007, but it is always helpful to look at how an asset class has performed in the past (see below). US Treasuries did come to your rescue in the GFC (the blue line), whereas GCC sovereigns whilst secure, did not help with meaningful positive returns (the orange line), see below:

Where did we land this week?

We did the interesting hypothetical exercise of putting together a portfolio of GCC bonds. We did the legwork, looking at index composition and duration, oil-fiscal sensitivity, liquidity premia, issuer mix, and practical access via benchmark-linked UCITS structure.

To be clear, we aren’t putting GCC fixed income into our funds right now, but as this region becomes ever fiscally stronger, and more regional credits added, there will come the point where an allocation to this asset class makes sense in our global portfolios.

Derek Akkiprik

-------------------------------------------

“Reasons to stay bullish”, 27/10/25

By Canaccord’s Justin Oliver

The major stock market indexes rocketed to new record highs on Friday. It is perfectly conceivable that the S&P 500 stock price index rises to 7000 by the end of this year and 7700 by the end of next year. Those targets would be exceeded sooner if animal spirits take hold, although that would increase the odds of bearish outcomes — i.e., a correction, a bear market, or a meltdown.

September's cooler-than-expected CPI report on Friday morning increased the odds of two more Fed rate cuts before the end of this year. The CME FedWatch Tool reflects a 90% probability of two 25bps cuts before year-end, bringing the federal funds rate (FFR) down to 3.50%. It's a sure bet.

The 2-year US Treasury yield had already declined from 3.60% at the beginning of October to 3.48% on Friday. However, the 10-year yield remained stuck around 4.00%. The Fed may be making the same mistake as it did last year, when a 100bps cut in the FFR prompted a 100bps rise in the 10-year yield (along with mortgage rates).

The S&P 500 is now up 15.5% ytd. On average over the past 10 years, the index has increased by a total of four percentage points in November and December combined. If it does so again this year, the index would rise to 7063 from Friday's close.

After a brief correction earlier this year, momentum stocks have continued to lead the bull market higher, as they have since late 2023.

The widespread concern about the sustainability of the bull market is that S&P 500 valuation multiples are elevated. We don't think this poses a problem unless we are wrong about the resilience of the economy and a recession scenario becomes more likely. Meanwhile, our bullishness has significant tailwinds coming from earnings. S&P 500 forward earnings per share rose to another record high of $298.52 last week. At Friday's close, the forward P/E was 22.8. Forward earnings is converging toward the analysts' 2026 consensus earnings estimate, which edged up last week to $305.03 per share, see below:

Both the S&P 400 MidCaps and the S&P 600 SmallCaps have yet to exceed their record highs hit at the end of last year.

That's because their forward earnings have been stuck in the mud since mid-2022. Their recent recoveries have been lacklustre. Investors Intelligence Bull/Bear Ratio (BBR) probably rose above 4.00 this week. The result will be reported on Wednesday. Readings above 3.00 can be contrary indicators, suggesting that there are too many bulls and that a pullback is imminent. In our experience, the BBR measure works better as a buy signal when below 1.00 than as a sell signal when above 3.00. The bull market run has many reasons to continue.

Justin Oliver

-----------------------------------

“The Overlooked Robotics Supply Chain Is At An Inflection Point”, 27/10/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

Two weeks ago -- while watching Figure AI’s demo video of its latest model, Figure 3 -- I suddenly felt vindicated in all the vision I’ve been talking about endlessly for years now: the robotics market is going to be much bigger than even I have been saying.

Figure 3 throws a ball for a white lab. Source: YouTube.

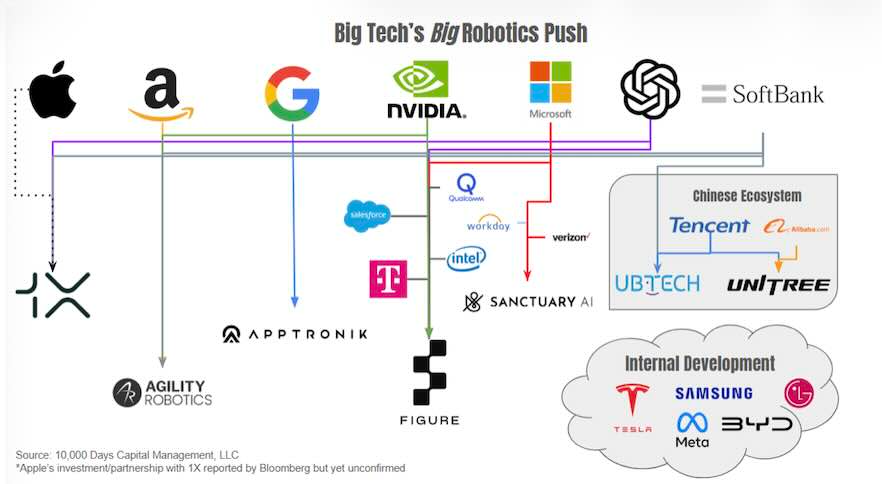

Tesla has been our largest position since we launched the US Technology VIP Fund in large part because we recognize the massive potential for the Optimus Robot.

But watching the Figure video, I saw that The Humanoid Robotics Revolution would be much bigger than just Tesla — and the Robotics Revolution will be much bigger than just humanoids. There will certainly be millions (or billions!) of cheap, mass produced robots (like Optimus), but there will also be millions of high-end premium robots, speciality robots, working robots, luxury robots, etc.

This Revolution is gaining steam because AI has made robots smart. For the first time, machines can learn tasks by observing them—just as humans do—instead of requiring every motion and decision to be hand-coded. Second, there is a flood of money going into the humanoid-robot ecosystem right now. As we show below, the major humanoid-robot startups have raised north of $5 billion in funding and accumulated over $60 billion in market cap:

So, how do we invest in this Revolution? First, we have and will continue to own an outsized position in Tesla. But we also think that the best non-Tesla way to invest in The Robotics Revolution at this moment is to invest in the robotics supply chain.

We’ve identified companies in this supply chain that are sitting at the cusp of a major inflection point in revenue and are basically not priced for any growth above trend (these are all trading at very reasonable present valuations and are dirt cheap using our proprietary model (shown below)). And almost nobody is looking at these industrial companies for plays on The Humanoid Robotics Revolution.

We analyzed about fifty companies that might supply materials to the humanoid (and other form factors) robotics builders and in this article we’ll discuss the three best plays right now which we’ve bought for the US Technology VIP Portfolio.

- Novanta, Inc. (NOVT)

Novanta is a pure play on robotics, across the humanoid, industrial, and medical industries. The company has been a key supplier in the minimally invasive surgery robotics market (selling to companies like Intuitive Surgical (ISRG)) and is now moving heavily into the industrial and humanoid markets. In their second-quarter earnings call, they disclosed a three-year, $50 million deal with a “leading e-commerce and warehouse robotics company,” (sounds like Amazon to me) and they expect that opportunity to grow rapidly. Overall, Novanta’s management is shooting to capture $1 billion in incremental revenue from "physical AI” over the next 5 years, which would more than double the company’s current revenue. The CEO also stated that they are already working with over 10 leading humanoid companies, and expect to announce major design wins in the near future.

- Vishay Precision Group (VPG)

Vishay makes specialty sensors and subcomponents that go within tactile sensors, called strain gauges. These are tiny strips that are embedded within other devices (like a humanoid robot hand) that detect microscopic movements in force and convert that into an electrical signal. These sensors are critical for robots to detect and control the application force, so that they can perform actions -- like picking up an egg, dealing cards, petting a dog, etc. -- safely in the real world.

Source: Tesla.

The company first disclosed that it had secured a design win with a humanoid robot maker (likely Tesla) in November 2023. Since then, Vishay’s management has disclosed that the company continues to receive more orders from humanoid robot $4.5 million in total bookings from humanoid manufacturers in the last 12 months or so.

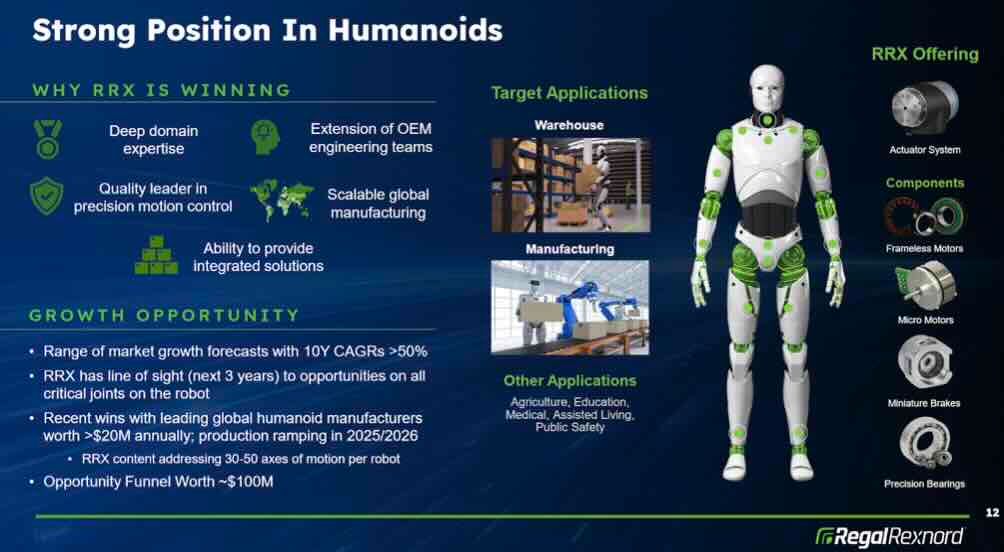

- Regal Rexnord (RRX)

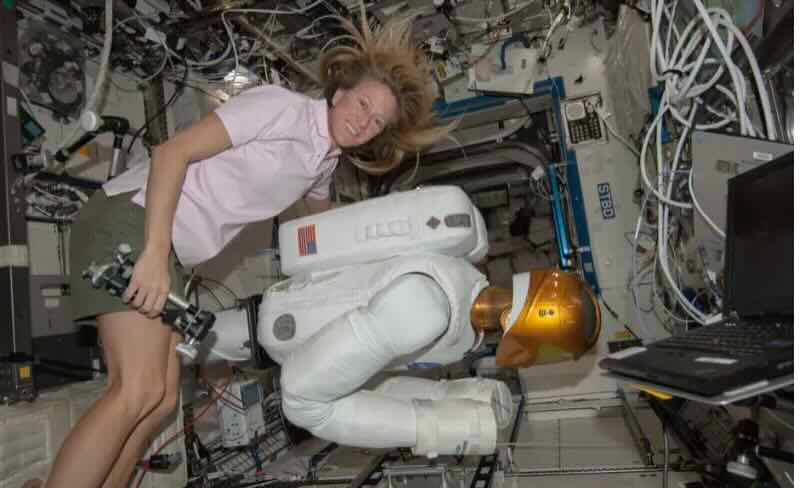

Regal Rexnord actually has a long history of building parts for specific humanoid robots, such as those used in Robonaut 2, the first humanoid robot used in space by NASA.

NASA’s “Robonaut 2”, the first humanoid robot in space, working on the ISS. Source: NASA.

RRX is keenly focused on the humanoid opportunity, and recently disclosed that it had secured several design wins worth over $20 million in annual sales. The CEO stated that these design wins cover “between 30 and 50 axes of motion per robot and include both Regal Rexnord components and integrated solutions.” The current sales funnel for humanoids is approaching $100 million.

Risks

There are two primary risks involved with these investments: (1) vertical integration by the OEMs; and (2) competition from low-cost Asian manufacturers. However, we think those are largely mitigated by the relatively low valuations of these companies. Moreover, we think there are a lot of humanoid developers that don’t have the capital nor know-how to vertically integrate to the same extent as Tesla. Further, a humanoid robot is extremely complex (1-2 orders of magnitude more parts than a car), and it is highly unlikely that all of these various parts are vertically integrated by all of the OEMs. With respect to China, we think there will likely be a premium on the highest quality American parts. Moreover, we think most American and European companies will want to build their humanoids using parts made in the West, given the huge implications for national defense, and the fact that these things will be living with and working in people’s homes.

Conclusion

As you can tell, we are very excited about the potential for our basket of robotics supply-chain stocks. We think these stocks are all trading at reasonable valuations and are about to see a big inflection in growth rates that the market isn’t pricing in at all.

Cody Willard

Disclaimers

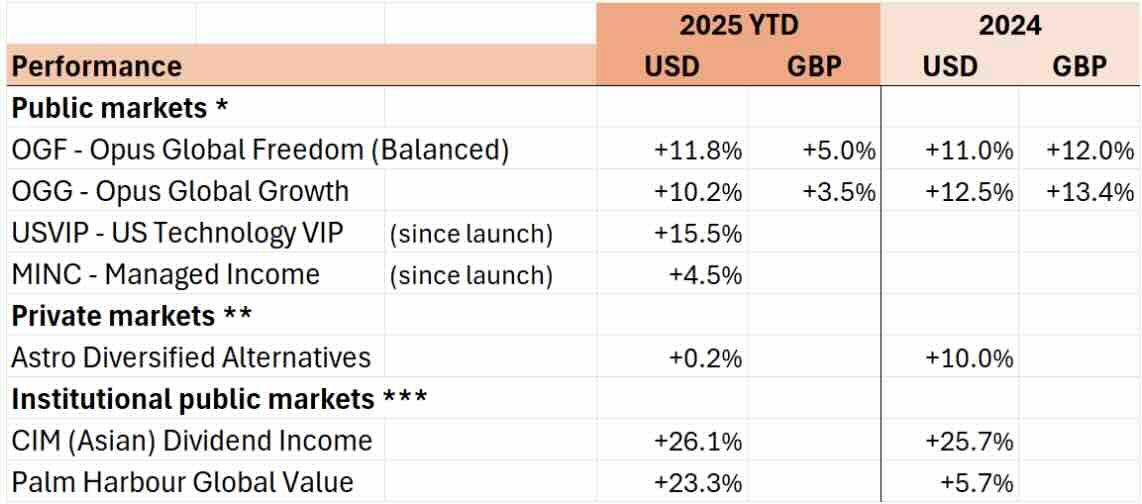

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 25/10/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 25/10/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.