Weekly Newsletter

Freedom Calls: 20/10/25, “Gold keeps shining ... and big tech earnings are out soon”

by

From the team at Freedom Asset Management

October 20, 2025

7 Minutes

Freedom Calls: 20/10/25, “Gold keeps shining ... and big tech earnings are out soon”

From the team at Freedom Asset Management

Trump does “bait and switch” on Zelensky in Washington

Last week, Trump and Putin surprised us all with a phone call and an agreement to meet sometime in the future in Budapest, at the invitation of the great democratic statesman Mr Orban. This happens to be whilst Orban is holding the largely ceremonial title of the Presidency of the Council of the EU. The rest of the EU are aghast. As readers will know by now, Orban is the most pro-Putin of EU leaders and Hungary has started the process of removing itself from the International Criminal Court (ICC), which would otherwise require Hungary to arrest Putin on arrival. So all the gloves fit for why the meeting is to be held in Budapest.

Pictured: the parliament building in Budapest, picture credit: elte.hu

For the discerning, Budapest offers some lovely sight-seeing - and the Eger region, not far from Budapest is well worth a visit for its excellent red wine. The presidential dinner will then I am sure be finished off with a bottle of legendary Tokay, apparently described by France’s King Louis XIV as the “wine of kings, king of wine” – quite some praise indeed from the French. All of this will be lost on teetotaller Mr Trump, but I suspect Mr Putin may partake.

I was in London last week, getting one of my regular updates on the state of Russia from an informed source - note: this was before the Trump/Putin phone call. I asked for “the tea”:

“It’s terrible… Putin has completely lost the upper hand in these negotiations, he handled [the Trump meeting in] Alaska really badly… he could have got a good deal there. And if Putin had been really smart he would have made some bold promises (subject to further protracted negotiations) and he could have dragged out a ‘peace process’ for months whilst still attacking Ukraine.”

The deal on the table in Alaska in August, was (1) Russia gets to keep Crimea, (2) a ceasefire is declared, (3) negotiations continue, in return for (4) some immediate US sanctions relief. Putin demanded effectively the capitulation of Ukrainian forces and agreement on the 4 territories it now largely controls. Trump stormed off and cancelled lunch.

Back to our source in London. I asked about Tomahawks and whether that changes the dynamic:

“Not really… send as many as you like, you are not going to do much damage to Russian infrastructure. The point is that if you look at a Russian oil refinery they were built to withstand multiple attacks… it’s not like a European refinery where everything is tightly packed into one place so one Tomahawk would do substantial damage …. a Russian refinery can extend to over 6km long and they are spread all over Russia. You need a lot of Tomahawks to take all those out – and the Americans just don’t have that many [spare].”

So, did Trump do a “bait and switch” on Zelensky inviting him to Washington to talk about Tomahawks and then throwing maps around the table and being reticent on the Tomahawks? Maybe, maybe not.

Remember Trump’s objective here is to get Putin to the table for a deal, not to level Moscow and St Petersburg. There is no chance that peace-loving Trump would endorse a civilian target for the Tomahawks – and if you believe our source above, it is much better to threaten the Tomahawks, than actually to send them.

There was obviously something to that Putin/Trump phone call which changed the dynamic (again).

Let’s see where this goes. Our expectations are pretty low. Whilst Putin would like to show some progress, he is in no hurry for peace. He perceives he is winning and this effort can show his home audience that Russia is being taken seriously on the world stage. Expect protracted disappointing talks.

But I would love to be proved wrong here.

Performance – Gold rocks!

Gold had a great week as people are piling into the precious metal. We hold gold in both the balanced and growth funds – and the growth fund holds about 8kg to be more precise (c.$1.1m worth), so that helped in a week which was otherwise unremarkable. USVIP was back up on the week, as was the allocation to Japan, even if core S&P500 was more subdued. Defence stocks have had a couple of unhelpful weeks, but this is after a remarkable run of 70%+ YTD. We don’t think defence is done yet.

There is a lot of talk about a turning point in private credit markets. We don’t hold any private credit exposure in the public market funds. There is no question that a lot of money has been poured into private credit attracted by the potential for high returns for investors and the high fees for managers. The spotlight last week was on the private credit losses at the US regional banks, which feature in the US small cap indices. We are keeping an eye on it – we have very little exposure to US small cap. We did a deep dive on the US regional bank stocks in the last month and concluded we did not like their exposure to regional commercial office lending, so the private credit exposure is the cherry on the cake.

This week, as you may remember, we have the CCP plenary session in Beijing, as well as tech earnings around the corner, so expect continued choppy waters for a few weeks. We believe coming through the chop we will see stronger markets.

(For detail, please refer to disclaimer section below)

Our articles this week:

- Justin Oliver, Adviser to the Opus Global Growth Fund (OGG), writes for us about gold in “Gold keeps shining”.

- Cody Willard, Adviser to US Technology VIP Fund, explores upcoming important tech results in “Why The Markets Are Waiting With Bated Breath On Big Tech Earnings”.

Please scroll down to read the articles.

I start this week in the Guernsey office with colleagues Alan Walker, Bill Francis and Ramon Eyck, where I may tempt them to an early morning swim(!)…. before I head off for the rest of the week in Abu Dhabi. I will be in Abu Dhabi and Dubai with Justin Oliver for the week of 27th October, so please reach out if you would like to catch up.

Wherever you are, please let me wish you a wonderful and peaceful week ahead.

All the best,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

——————————————

“Gold keeps its shine”, 20/10/25

By Canaccord’s Justin Oliver

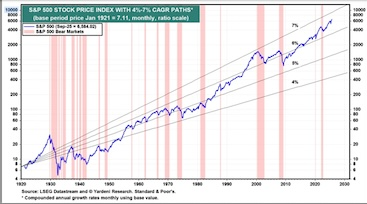

Both the S&P 500 and the price of gold have been roaring ahead to new record highs this year and while it might appear frivolously optimistic, we wouldn't be surprised if both hit 10,000 by the end of this decade.

The stock price index and the gold price have exhibited an inverse cyclical correlation, but their long-term upward trends have been remarkably similar. The ratio of the two has fluctuated around 1.7. They seem to converge and be equal every 10-20 years, though the data are limited because the price of gold was fixed until President Richard Nixon stopped pegging this price in 1971.

We believe that the S&P 500 can reach 10,000 by the end of the decade, driven by strong earnings growth—assuming that there’s no recession in the interim. And the no recession scenario remains our base case in light of the economy's remarkable resilience since the start of the decade.

The economy did experience a recession, lasting just two months, during the pandemic lockdowns in early 2020. But its short duration amid extreme pressures attest to the economy’s underlying resilience: when the lockdown restrictions were lifted, ongoing social distancing restrictions didn't stop the recovery. Nor did global supply-chain disruptions, which triggered a spike in inflation, forcing the Fed to tighten monetary policy significantly in 2022 and 2023. Similarly, the economy continued to grow this year despite the stress engineered by Trump’s tariffs, the recent government shutdown, and labour shortages.

For the S&P 500 to get to 10,000 by the end of 2029 with a 22.0x forward P/E—our best working assumption—would require that forward earnings per share rise to $455 by the end of that year. We think that is a realistic outlook. More questionable is the 22x valuation multiple assumption. However, it is reasonable to expect plenty of lift from the Magnificent-7. They currently account for a record 32% of the S&P 500's market capitalization and sport a forward P/E ratio of 29.3x. We assume they’ll remain magnificent and continue to earn an outsized valuation.

The S&P 500's valuation multiple can remain historically high as long as the market consensus is that a recession is unlikely. A recession scenario would be bearish, with both earnings and the valuation multiple taking hits.

Gold and bitcoin don't have valuation multiples because they don't have earnings. They both have their fans, who can claim any upside targets they fancy (e.g., $1 million), knowing they can't be challenged by traditional valuation analysis. All we can try to do to project where they’re headed is to extrapolate the trends seen in charts.

What could end the remarkable rally in gold? The easing of geopolitical crises might do so. There might be some willingness by governments to rein in their fiscal deficits. Good luck with both of those! What if the Trump administration decides to sell the gold held at Fort Knox to pay off some of the US government's debt? The US Mint claims that its gold reserves total 248 million ounces. At $4,000 per ounce, it would be valued at $992 billion. That's a drop in the bucket of the $37 trillion in US public debt. It's also small relative to above-ground world gold stocks. The World Gold Council estimates that the above-ground gold in the world totalled 6.95 billion ounces at the end of 2024. That would be worth approximately $28 trillion at the current gold price. Central banks around the world have proven to be price agnostic buyers and we see few reasons why this won’t continue.

10,000 for the S&P and gold in just over 4 years? It’s not as outlandish as it might first appear.

Justin Oliver

-------------------------------------------

“Why The Markets Are Waiting With Bated Breath On Big Tech Earnings”, 20/10/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

Like it or not, if you are invested in the markets, you are invested in AI. Valuations, and in many cases the fundamentals, of companies across sectors are driven by what happens in The AI Revolution.

With The AI Revolution seemingly accelerating every day and the markets hovering close to all-time highs, it might surprise you to find out that investors and traders have built a substantial wall of worry. Over the last month, the S&P 500 is basically flat (up 93 basis points) while the VIX is up a whopping 40% (Reminder: the largest nine tech companies make up 40% of the S&P):

That’s an uncommon phenomenon. It’s especially uncommon when the markets are hovering around all-time highs. It’s also shocking to see the “Fear & Greed Index” sitting in the Extreme Fear category, again with the markets at all time highs.

So it appears that a lot of investors are preparing for the worst, and they’re willing to pay up for put protection even with the markets fairly steady and the fundamentals of the economy looking pretty much okay. And the source of this fear? It goes back to what we wrote last week: it is the fear that AI is in a bubble and is about to pop.

Which brings us to earnings season, the topic of this article. We’re at the very beginning of earnings season, and we’ve already got some important numbers in tech land from the likes of TSMC and ASML (both of which were very good). But the market was more or less indifferent to those prints. Instead, it is waiting around with bated breath on the numbers from the big AI chip buyers: Microsoft, Google, Amazon, and Meta. It’s fascinating to think that the entire market depends on the statements of these four companies, but that’s really, at least a large part of, the truth.

These four companies matter immensely—they’ll account for roughly 75% of global AI infrastructure spend this year. And despite a flood of pundits casting doubt on the return profile of AI, the hyperscalers’ ROI math is the only one that matters.

The market is worried about ROI and the sustainability of AI capex spending for a couple reasons. First, the circular nature of recent deals for AI investments and chips between companies like Nvidia, OpenAI, Oracle, and AMD is reminiscent of the dot com days. Second, more fundamentally, people cannot wrap their minds around $400 billion plus in annual capital spending.

However, we expect that big tech will quell most of the fears surrounding the AI capex buildout. All indications are that the cloud businesses continue to grow as rapidly as they can bring supply online. Moreover, as the first instances of Nvidia’s cutting edge Blackwell architecture come online, we expect to see another step change in model performance. As AI models become more capable, usage goes up, driving further investment in cloud resources. Further, we’re already seeing big ROI for the internal application of AI at these companies in addition to early signs of monetization in standalone “AI Revenue” in the form of Microsoft Copilot, Google Gemini, etc.

Accordingly, we don’t expect AI capex to slow down any time soon. The rapid growth in AI usage, both in terms of the number of users and the number of tokens generated per user -- driven by things like advanced reasoning models and video generation tools -- continues to drive demand for more compute power. We wouldn’t be surprised if the hyperscalers issue 2026 capex guidance that is higher than expected given the continued acceleration of AI adoption and usage.

If the hyperscalers deliver on revenue and earnings growth, and show continued confidence in their ability to generate returns on their AI capex, we think there could be upward pressure on stock prices given the big wall of worry the market has built over the last month or so. On the other hand, if even one of the hyperscalers expresses concern about capex levels, that could lead the markets lower. But as long as demand for AI services continues to exceed compute supply as it has consistently for the last three years, the hyperscalers will almost certainly continue to grow their investments in AI infrastructure.

Feet to fire, we think that all indicators point to the hyperscalers seeing further acceleration in revenue growth at their cloud businesses, which will lead to more capex spend, not less. Of course, we’re not gaming the next quarter or two; we’re betting on these trends for the long term. We continue to think we are in the early days of The AI Revolution and we’ll look back and see how irrelevant most of the present fears and worries turned out to be.

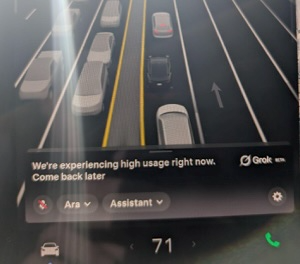

And a personal anecdote to put a bow on this piece. As I was driving home for work after writing this article, I attempted to talk to Grok in my Tesla and received the below notification that it was unavailable because of high usage. I’ve received similar notices from both Google Gemini and ChatGPT in the last month or so at various times. I’d say there is not enough compute out there…

Cody Willard

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 18/10/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 18/10/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.