Weekly Newsletter

Freedom Calls, 15/9/25, “The bulls are running… and someone opened the IPO window"

by

Freedom Asset Team

September 15, 2025

7 Minutes

Freedom Calls, 15/9/25, “The bulls are running… and someone opened the IPO window"

From the team at Freedom Asset Management

It was a good week in the markets and all of our strategies, see the performance section below. London was also buzzing last week, with Europe’s largest arms fair in town… and of course our very own Cody Willard and Bryce Smith talking about investing in US revolutionary technology.

Pictured: (L-R) Cody Willard and Bryce Smith huddled under an umbrella, with the Royal Air Force’s ensign and the Union Jack adorning London’s Mall, Sept 2025.

US interest rate cut in September

It seems like a racing certainty that the US Federal Reserve will push for a 25bps rate cut on Wednesday this week. On the one hand it seems odd that a cut is needed at all with stock markets reaching all time highs, but there are signs that the US labour market is weakening and probably the cut should have come earlier. Anyway a 25bps cut is so baked in that anything else would be the surprise. Cannacord’s Justin Oliver gives us his view in the articles below.

A chill wind blows through the UK, but maybe the defence industry comes to the rescue

The bright light in the UK economy is the defence industry. Everything else is pretty gloomy. Almost everyone we sat down with in London last week is expecting the upcoming UK budget to mean higher taxes - the only questions are: "which taxes?" and "how much?”

Nobody is ready to invest in their UK businesses whilst this uncertainty prevails. I think even the Labour Party have now worked out that ending the nom dom regime has been a mistake for the UK economy.

But the bright note is definitely the UK defence industry as Charles’ note last week pointed out, there are substantial defence deals being done in Europe and the UK is the clear winner. I wonder whether this could point to a broader realignment of Europe and an economic turning point for the UK. We have come to learn that the US is not interested in being the defence backstop to Europe, and so Europe needs to step up. A wishy-washy "coalition of the willing” means nothing in defence terms; one country will need to lead, and militarily that can only be either the UK, or France - and I just don't see the Scandinavians getting behind France. If Europe is organized around the UK, there is much more of a chance (in the current geopolitical climate) that the US will respond to a phone call from London…. than from Paris, Berlin or Rome.

And is it possible that the defence deals being done in Sterling are responsible for Sterling’s stubborn strength against the US dollar? Maybe, but for our US visitors, London was an expensive city last week. I still think Sterling depreciation is on the cards and maybe it will take the UK budget announcements for that to become clearer. Let’s see.

Someone opened the US IPO window

We were delighted to see that Klarna made its much awaited IPO last week in the US. Klarna is an investment in our Luxembourg VC fund. Although we still have a 6-month lock up on that position, at the current rate that will be in excess of a c.2x exit on that investment. We thank our friends at Mubadala Capital for bringing this allocation to us in 2022. Importantly, now that the IPO window is open again, this is good news for US tech stocks in particular. We have not seen these levels of US IPO activity since 2021. Fingers crossed it lasts!

Performance - let the bulls keep running...

OGF is within a whisker of 10% YTD in US dollars; OGG has pulled back ground quickly at 7.7% YTD; USVIP had a good week up 5%, and MINC continues its steady low vol grind upwards.

In USVIP last week we made an investment into the only liquid proxy for SpaceX, following Echostar’s deal for spectrum that SpaceX so badly needs. The resultant deal means c.50% of the market cap of Echostar is their SpaceX equity. We have always liked SpaceX and this is the best liquid way to have exposure to the asset.

For our institutional investors, the CIM Dividend Income fund (+27% YTD) has been benefiting from mainland Chinese insurers searching for yield as domestic interest rates have fallen in response to a difficult economic outlook for mainland China. High yielding Hong Kong ‘H’ shares, via the Southbound Connect, have been the beneficiaries of this flow, proving that you do not need a vibrant economy for an investment strategy to prosper, sometimes you just need to own the things that people want to buy.

Capital at risk. Source: * Estimates Freedom Asset Management as at 13/9/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch date of USVIP 10/2/25, ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** FT Markets as at 13/9/25, I shares.

Our articles this week:

- Cody Willard writes about “Navigating the hype in tech stocks"

- Justin Oliver writes about the upcoming Fed rate cut in “Time to cut"

- Charles Harris talks through his research into an uncorrelated way to invest in fixed income, in “Catastrophe bonds: The bond with 9 lives”

This coming week I am in Abu Dhabi and Dubai, next week in Hong Kong - all with Cody Willard and Bryce Smith. A big thank you to all our clients and friends of the firm that made us feel so welcome in London and Guernsey last week.

All the best,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111* // M: +971 585 050 111 // M: +852 5205 5855* (*also WhatsApp)

--------------------------------------

“Navigating The Hype and Panic Cycles in Tech Stocks”, 15/9/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

It was only a few weeks ago that tech stocks were trading down amid the underwhelming release of OpenAI's GPT-5 and an MIT report claiming "95% of enterprise AI applications fail to deliver on their promises". While that kind of headline noise is irrelevant to our long-term Revolution Investing approach, many industry contacts and market commentators were concerned a bubble was popping. Accordingly, numerous tech stocks sold off sharply.

Fast forward to today. Oracle delivered a blowout quarter last week, propelling many of those same tech stocks to new all-time highs. This rally came after Oracle projected its cloud revenue would grow to $144 billion over the next 4 years, up from $18 billion this fiscal year.

The lesson here is that short-term volatility does not alter our long-term views on AI development or our strategy for investing in Revolutionary Technology. Oracle's fantastic quarter only reaffirmed our thesis that there is a massive shortage of available compute to serve AI demand. As a result, our pure-play investments in this theme, such as CoreWeave, rallied strongly on the news.

And despite the pessimism echoed in the MIT report, we see clear evidence that AI is already having a material impact on productivity across the U.S. economy. This productivity growth is a powerful tailwind for the markets, and the companies in our USVIP portfolio are the primary drivers of those gains. Furthermore, when we consider that the hyperscalers are spending more on AI capex than the United States spent, in real terms, on building the railroads, the electric grid, or the interstate highway system, it is clear that significant room for growth remains. This potential extends beyond AI to the Robotics and Space Revolutions, which are still in their nascent stages.

Going forward, we expect the market to continue to wax and wane between AI hype and AI hate. However, we anticipate the market will maintain its long-term upward course, driven by the revenue and earnings growth stemming from these tech-driven productivity gains.

This is the most likely path over the next several years and it is one the reasons we are not anticipating a 2000-era dot-com crash. In essence, our strategy is to capitalize on opportunistic buying when the market sells off on short-term noise and to trim positions into periods of speculative hysteria. Indeed, the very fact that so many investors remember, lived through, and are seemingly preparing for a repeat of the dot-com crash probably means it won't happen exactly the same way again. There could definitely be some pullbacks along the way, but we think the Revolutionary tech trends we're investing in are likely to continue to power the markets higher over the medium to long term.

For the next few years, AI FUD (fear, uncertainty, and doubt) and AI hype will inevitably work their ways back into the markets from time to time; especially as this technology is still so new and we are still in the very early innings of these tech Revolution. But we are not afraid of this potential volatility, and that's also why we are constantly studying the market and these technologies so that we are prepared to take advantage of the opportunities when they present themselves (like we have several times just this year).

In conclusion, our job is to stay disciplined in navigating the mini hype and fear cycles we expect to play out over the coming years. That means not chasing the high flyers of the moment, or the shiniest new object in the room, while also slowly but surely scaling into our favorite Revolutionary names when they present attractive buying opportunities.

As we often say, our goal is to find the most Revolutionary companies changing the world so that we can grow our capital as safely as possible over time.

Cody Willard

-------------------------------------

"Time to cut”, 15/9/25

By Canaccord’s Justin Oliver, adviser to the Opus Global Growth Fund

Following last week’s cooler-than-expected PPI and as-expected CPI, expectations are that the FOMC will cut the federal funds rate by 25 basis points on September 17, with no dissenters to that decision among voting members.

Following the recent jump in initial unemployment claims, meeting participants might consider a 50-basis-point cut, but we doubt that they will opt for that, as the majority would likely dissent. Instead, the committee might signal the likelihood of more rate cuts ahead in its Summary of Economic Projections.

Consequently, we are raising our year-end S&P 500 target from 6,600 to 6,800. That’s our base-case scenario with a subjective probability of 55%. We currently assign a 25% subjective probability to a melt-up that lifts the S&P 500 to 7,000 by year-end 2025 and 20% odds to a correction in the index by the end of this year. If the Fed lowers the federal funds rate on September 17 and signals more rate cuts ahead, we will increase our odds of a melt-up and decrease our odds of a correction.

We are still not convinced that the economy needs to be stimulated by the Fed. Inflation remains closer to 3.0% y/y than to the Fed's 2.0% target. Real GDP is growing solidly despite the recent downward revisions in payroll employment. The unemployment rate remains between 4.0% and 4.3%. All this implies that either real GDP will weaken significantly and the jobless rate soon will rise sharply, or that productivity growth is making a strong comeback. We believe it is the latter.

Consider the following:

(1) GDP. Despite August's weaker-than-expected employment report, the Atlanta Fed's GDPNow model estimated that real GDP rose 3.1% (saar) during Q2, up from 3.0% on September 4. Capital spending on equipment and exports are robust. Consumer spending is solid at 2.3%. Real GDP was up 3.3% during Q2.

(2) Labour market. Initial unemployment claims jumped 27,000 to 263,000 (seasonally adjusted), the highest reading so far this year. This number could persuade a few FOMC participants to press for a 50-basis-point rate cut. So far, it is only a one-week spike, which has occurred occasionally in the past. In addition, 15,000 of the increase (not seasonally adjusted) occurred in Texas. That seems like a one-time aberration, unless a large number of oil field workers were let go a couple of weeks ago.

(3) Productivity. Strong GDP growth, coupled with a seemingly weak labor market, suggests that productivity growth must be robust. Over the past 12 quarters, productivity growth has averaged 2.1%, precisely the same as its average over time. If our forecasts are correct, we expect growth to approach 3.0% over the remainder of the decade.

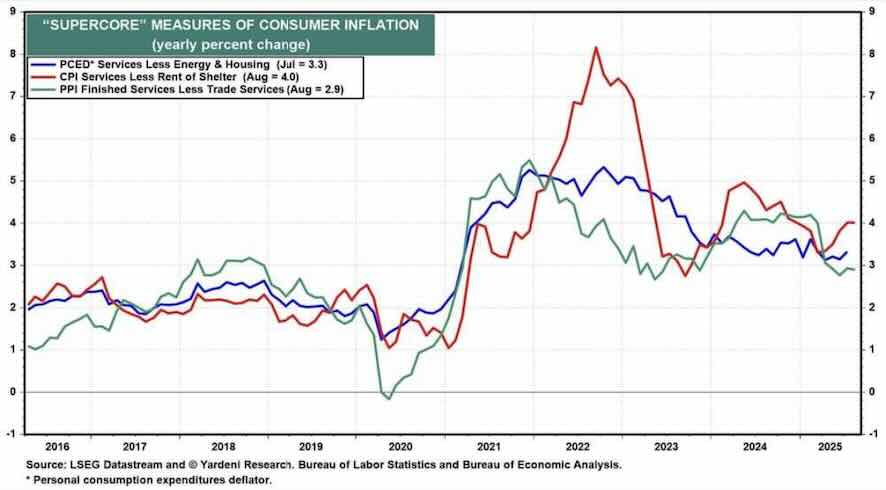

(4) Inflation. Meanwhile, the core CPI, core PCED, and core PPI for consumption—all excluding shelter—are closer to 3.0% than to 2.0%, as noted above.

Trump's tariffs have caused a slight increase in durable goods inflation. That is likely to be a transitory problem. A stickier problem is that measures of the "super-core" inflation rate remain sticky between 2.9% and 4.0% (see below):

Ultimately, a robust economy augers well for corporate profits which, ultimately, are the strongest driver of stockmarkets over the long term. The investment outlook remains supportive.

Justin Oliver

-----------------------------------

“Catastrophe bonds - The bond with 9 lives”, 15/9/25

By Charles Harris

With the Atlantic hurricane season in full swing and recent news of Hurricane Erin testing the resilience of coastal communities in the south-easten US, the complex world of insurance and risk management is once again in the spotlight. In this high-stakes environment, a unique financial instrument has been quietly gaining prominence: the catastrophe bond (aka “cat" bonds). More than just a niche product, these cat bonds represent a fascinating intersection of insurance, natural disasters, and capital markets, offering a compelling solution for both risk protection and investment diversification.

Cat bonds are a specialized class of debt instrument and a subset of the broader Insurance-Linked Securities (ILS) market. Their primary function is to transfer a specific, well-defined set of catastrophic risks from a sponsor - typically an insurance company or a reinsurance firm, but increasingly also corporations and government entities - to investors in the capital markets. These bonds can cover any peril risk ranging from earthquakes or wildfires in California to tsunamis in Japan, but most commonly cover hurricane damage in the south-eastern US.

Cat bonds first emerged in the mid-1990s after a series of major disasters (Hurricane Andrew in 1992 & Northridge earthquake in 1994) strained the traditional reinsurance market and exposed limits in their ability to cover claims.

Today the asset class exceeds $56bn and has, since inception, generally delivered strong risk adjusted returns - the only major drawdown in the last decade linked to Hurricane Ian in 2022. Since then, the market has rebounded strongly, returning just shy of +20% in 2023 and +18% in 2024. Since inception in 2003 to 2024 the SwissRe Cat Bond Index has an annualised return of +7.7% vs the S&P Short Term US T-Bill Indexes +1.8% (Source: Morningstar, Schroders, FT).

The investment case

The cat bond market has surged in popularity in recent years, growing from a niche alternative investment to what is now a $56bn market. Largely driven by recent demand from hedge funds, but also the persistent demand for peril protection as catastrophic events progressively inflict more damage. These events are not only occurring more frequently, but as development occurs over time so does the insurance market as a result.

The main investment appeal is diversification. As the return of a cat bond is linked to the occurrence of a predefined catastrophe and not financial market fluctuations, they provide a unique tool to reduce portfolio volatility.

The floating rate structure provides a hedge against interest rate exposure; the low duration of the cat bonds themselves (average 3 years) and their underlying assets also limit interest rate volatility and risk.

Since cat bonds are fully collateralised, investors are also shielded from the sponsors credit risk adding another layer of protection.

Furthermore, cat bonds offer attractive and consistent returns, since inception the SwissRe Cat Bond Index has only had one negative year, with an annualized return of +7.7% (as of EoY 2024).

The unique coalescence of low correlation to financial markets, high yield returns and mitigated credit risk make cat bonds a popular tool amongst portfolio managers seeking attractive and stable returns.

What are the headwinds for the sector?

Beyond seasonal risk, attention is also turning to market regulation, with the European Securities and Markets Authority (ESMA) considering restrictions on retail access. Such proposals pose a potential headwind, with reduced demand likely to weigh on liquidity and pricing.

At the same time, the growing presence of hedge funds and private investors - highlighted recently by Munich Re in the Financial Times - is reshaping the market. They warn that whilst this influx of capital has deepened liquidity, these newer market entrants may lack the expertise and long-term commitment of traditional reinsurers, potentially amplifying risks when extreme events do occur.

As we come to learn from investing, sometimes the bear case actually becomes the bull case.

That said, greater regulatory oversight could strengthen long-term confidence by reducing systemic risk. Should prices fall in the months ahead as a result - whether from seasonal volatility or regulatory pressure - the period following hurricane season could offer an attractive entry point. For those seeking diversification and uncorrelated market yield, cat bonds' strong recent performance merit a place on investors’ radars - with the potential to shine bright once the storm of hurricane season has blown over.

This is an asset class that we shall be following over the coming months for a possible small allocation in our fixed income exposure if an attractive entry point presents itself.

Charles Harris

----------------------------------------------

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.