Weekly Newsletter

Freedom Calls: 13/10/25, “And the winner is …. Peace!"

by

From the team at Freedom Asset Management

October 13, 2025

7 Minutes

Freedom Calls: 13/10/25, “And the winner is …. Peace!"

From the team at Freedom Asset Management

"Nil points les Etats-Unis"

Much like the deciding votes in the Eurovision Song Contest have so little to do with the quality of the singing or songwriting, so it seems that the Nobel Peace Prize has so little to do with “peace”.

Pictured: Ukraine’s Ruslana, digging deep for a Eurovision winning performance in 2004, Picture credit: AP

The Eurovision Song Contest has been Europe’s most high-profile singing event since 1956. The UK which has brought so much to the international music scene has won the event only 5 times, which matches that hotbed of musical talent… errr Luxembourg! The last real commercial song to win the contest was Abba’s “Waterloo” in 1972. But who can forget such classics of our time like: “Rise like a Phoenix” by Austria’s Conchita Wuerst (2014), “Diva” by Israel’s Dana International (1998), or “Wild Dances” by the leather clad Ruslana (and friends) representing Ukraine in 2004 (pictured above). It felt too early on a Monday morning for a picture of Conchita Wuerst. The competition has descended into, an albeit very entertaining, fest of virtue signalling, and over the top performances from a wide variety of never-to-be-seen-again performers (largely for good reason).

But before we deride the Nobel Peace Prize committee as being little more than the equivalent of the Eurovision Song Contest, they have done something useful: everybody knows what Trump is achieving for peace right now in the Middle East - even the FT has been forced to admit he has done good work there; but perhaps we were less aware of struggle for democracy in Venezuela being fought by 2025’s Nobel peace prize recipient Maria Corina Machado. Many of the previous winners are also less well known peaceful protesters for democracy. And interestingly, the first thing that Ms Corina Machado did upon learning of her win was to praise Mr Trump and to ask for his help. Maybe he will get over it…. maybe he won’t. No, I don’t think he will either.

The good news is we seem to have a peace deal in Gaza, and sometimes we should just take the wins.

And perhaps Mr Trump should take comfort from the fact that not even Winston Churchill was awarded the Nobel Peace Prize… Mr Churchill had to make do with the 1953 Nobel Prize for Literature…. Churchill was also upset about it. So maybe herein likes the solution: that erstwhile epic, Trump's 1987 number one best seller "The Art of the Deal” gets Trump the 2026 Nobel Prize for Literature?! Stranger things have happened…

The UAE prepares for its first casino

It was a fascinating weekend in Ras Al Kaimah, where amongst other things we saw the development work on the first casino to launch in the UAE. 5 years ago it would have been unthinkable that a casino would be granted permission in this country, but roll the clock forward to today and the imposing Wynn hotel and casino with 1,500 rooms, is due to open in 2027 on the newly created offshore island of Al Marjan.

Pictured: the sun setting on the construction site that is Al Marjan island and its 1,500 room hotel, taken from the Al Hamba beach resort, Oct 2025

Be prepared for some choppy markets over the next couple weeks or so

Friday was fairly bumpy in the markets, as Trump launched his latest salvo in the tariffs wars against China. In fairness, it was China that made the first move restricting rare earth metal exports earlier in the week. On Trump's comments, US markets promptly dropped between 2-5%.

If you remember from a recent note we have the upcoming Chinese Communist Party plenary session 20-23 October (in 10 days’s time) so the timing of China’s move on rare earths appears not entirely coincidental. Xi will want to go into this meeting showing strength.

The only sensible outcome in all of this is a deal, which both sides want and need. China’s fragile economy desperately needs to retain export access to the US - there is simply no other market that can replace the US. And the US needs those rare earths. China is also keen to boost consumption and encourage entrepreneurship, having learned that common prosperity does not work.

But we should be prepared for some choppy markets whilst the deals get done. The main point here is that we have seen this show before, and we should expect wiser heads to prevail.

Performance - a bumpy week

Bumpy weeks are always good opportunities for top-ups. I will be looking to do that over the next couple of weeks, so please reach out to the team if you are thinking the same thing. Top-ups are usually quick from a compliance perspective, and help dollar cost averaging.

(For detail, please refer to disclaimer section below)

Our articles this week:

Justin Oliver, Adviser to the Opus Global Growth Fund (OGG), “Japan’s next prime minister makes Margaret Thatcher look like a moderate”.

Cody Willard, Adviser to US Technology VIP Fund, explores the “Top 5 reasons we are probably not in a bubble”. This is a 'must read' for all tech investors.

Please scroll down to read the articles.

This week I will be back in London and Guernsey for some cooler weather and lovely clients. Wherever you are, please let me wish you a wonderful and peaceful week ahead.

All the best,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

——————————————

“Japan’s next prime minister makes Margaret Thatcher look like a moderate”, 13/10/25

By Canaccord’s Justin Oliver

In picking Sanae Takaichi as Japan’s next prime minister, the Liberal Democratic Party (LDP) made as right-leaning a choice as it could have. The conservative firebrand makes her two political heroes - Japan’s Shinzo Abe, prime minister from 2012 to 2020, and the UK’s Margaret Thatcher - seem almost moderate!

With nicknames ranging from “Iron Lady” to “Taliban Takaichi,” Japan’s first female leader - assuming that she can build a governing coalition by October 15, a likely prospect - will be anything but boring. Yet the real excitement is likely to be what the bond markets make of her pro-stimulus worldview.

There are a couple of reasons why Takaichi’s policies might unnerve the financial markets:

(1) Nationalist fervor. Even the LDP’s longtime coalition partner Komeito is unnerved by Takaichi’s nationalism, anti-immigration rhetoric, and reputation for having some of Tokyo’s sharpest elbows. The yen’s slide past 150 level to the dollar could continue. Like Abe, Takaichi is concerned less with structural disruption than she is with monetary and fiscal pump priming. The “Takaichi trade” recently sent Nikkei 255 stocks to an all-time high, with the market rising over 5% last week.

(2) Stimulus over reform. The late Abe did more during his reign to exacerbate Japan’s addiction to free money and runaway debt, than to revive its animal spirits. “Abenomics” was a three-part plan. The monetary and fiscal arrows were deployed immediately. But Abe failed to fire the third and most vital arrow: cutting bureaucracy, modernising labour markets, and catalysing a start-up boom. Only by firing up these reforms can Japan compete in the artificial intelligence age. Yet Takaichi prioritizes policy measures over more substantive reforms - with a bias toward monetary easing that puts her at odds with the Bank of Japan (BOJ) and with fiscal stimulus plans.

The BOJ will have an even harder time pursuing its tightening agenda under Takaichi and last year, she called BOJ rate hikes “stupid.” The price for winning opposition support to stay in power is likely to be tax cuts. Takaichi knows that lasting more than 12 months in power - a rarity in Japan - requires lightning-fast wins. There is the potential for her to trigger a ‘Liz Truss’ moment at a time when 20-year Japanese yields are already near 1999 highs. Meanwhile, Takaichi scored a surprise win in the election by talking tough on China and hinting at a renegotiation of the US-Japan tariff deal. It’s not clear what will annoy Donald Trump more: a sharply weaker yen or Tokyo’s refusing to pay his $500 billion “signing bonus.”

Where Japan goes from here - and where that takes the globe – it definitely won’t be boring.

Justin Oliver

--------------------------------------

“The Top 5 Reasons We’re Probably Not In A Bubble”, 13/10/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

Even before Trump’s fresh reignition of the trade war with China on Friday, you could tell that tension was building in the markets all week. This was evident in the fact that the VIX continued its slow and steady rise higher throughout the week while the markets ground higher as well (a quite unique phenomenon). Even though the markets didn’t show it, there was plenty of built up nervousness that was ready to translate into selling pressure at the first sign of weakness, and the catalyst finally came on Friday when Xi and Trump both ratcheted up the rhetoric in the trade war.

But the real source of the tension isn’t really the trade war (that’s old news), it's the possibility of a bubble. It didn’t matter where you looked this last few weeks, everyone was debating the possibility of a bubble in the U.S., and in tech stocks in particular:

- “I think that there will be a lot of capital that’s deployed that will turn out to not deliver returns…” -- David Solomon, CEO of Goldman Sachs (October 3, 2025)

- “We’re getting in bubble stuff here . . . highest stock prices ever, highest gold ever, highest crypto ever.” -- Jamie Dimon, CEO of JPMorgan Chase (September 23, 2025)

- Valuations for AI companies are "ridiculously high.” -- Leon Cooperman, legendary hedge fund manager (October 1, 2025)

“The risk that there will be a bubble in private credit is pretty high.” -- Professor Elisabeth de Fontenay, Duke Law School (September 30, 2025)

The private credit sector is exhibiting “bubble-like” attributes. -- Fitch Ratings (September 30, 2025).

There is so much bubble talk that it almost feels like there is a bubble in calling for bubbles!

So the contrarian take at this moment seems to be that AI, and the markets more broadly, actually are not in a bubble. But contrarianism is not a reason, in and of itself, to be long right now. When we look at the fundamentals, it is clear to us that we are not in a bubble. So let’s break down the top 5 reasons that U.S. tech stocks are not in a bubble, and why these are still good investments for years to come.

Reason #1: Valuations Aren’t Crazy

Let’s start with the easiest way to show that we are not in a bubble: valuations. Put simply, the valuations of the largest tech companies on the planet are pretty darn reasonable when we consider the earnings growth rate. As you can see in the table below, the nine most valuable tech companies on the planet actually show a median 2025 PEG ratio of less than one, which is very reasonable.

Further, in absolute terms, a median forward P/E of 28 is nowhere near the insane levels we saw in the dot com bubble, when the forward P/E of the Nasdaq 100 was almost 80. Cisco and Microsoft traded at about 200 and 70 times earnings, respectively. So even if you think current valuations are a little overstretched, it’s hard to say that valuations are truly in bubble territory.

Reason #2: We’re (Mostly) Not Spending OPM (Other People’s Money)

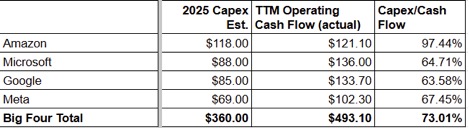

This is perhaps the biggest reason we are confident that the AI infrastructure buildout itself is not in a bubble. The hyperscalers -- which account for about 75% of all AI capex -- are funding basically all of this spend with their own operating cash flow. That’s a big departure from the dot com days, where the companies building out the massive fiber networks were mostly spending OPM. A 2001 McKinsey report found that the average capex-to-operating-cash-flow ratio in the telecom sector exceeded 200% in the late 1990s — i.e., they were spending 2x or more of their cash flow on capex, with the gap filled by external financing.

Today, the Big 4 Hyperscalers are only spending about 73% of their trailing twelve month cash flow (FY2025 operating cash flow estimates were not readily available). That’s a far cry from the 200%+ spent on fiber during the dot com boom.

This shows that the hyperscalers still have lots of room to grow capex spending if they so choose. Of course, some smaller companies are starting to tap debt and equity markets to build data centers, but the ones that make up the vast majority of the total spending are spending their own money. Moreover, as we explain below, those companies are already generating real ROI with that spending, which means they’ll spend even more until the ROI starts to drop off (if ever?).

Reason #3: AI Is Generating Real ROI Right Now

Despite this historically high level of spending in absolute terms, these AI infrastructure investments are already generating real ROI for the big spenders. The cloud businesses (renting chips to third-party customers) have seen a re-inflection in growth and profitability in the AI age. But what’s more telling is that companies like Meta -- which uses all of its AI infrastructure for internal use cases -- are seeing a big uptick in growth and profitability.

By the end of 2025, Meta will have purchased about 1.3 million Nvidia GPUs, purchases totaling around $39 billion (assuming $30k per chip). That would mean Meta is attributable for at least 12% of Nvidia’s revenue in 2024 and 2025.

But how do we calculate Meta’s ROI on its Nvidia purchases if it is not generating standalone “AI Revenue” from these chips? The best way to do this is to look at the change in Meta’s profitability excluding the growth in users (although it's likely that improvements made to Meta’s tech via GPUs is also responsible for some user growth).

In 2023 (before Meta started binging on GPUs), the company’s Average Annual Revenue Per Person (ARPP) was $43.15. Over the last four quarters, that number was $52.55, representing 21.8% ARPP growth in about eighteen months ($9.4 additional ARPP). If we assume that all of the growth in ARPP in the last eighteen months was attributable to GPU-enabled improvements in the ranking systems, and we multiply that by Meta’s current users (3.48 billion Daily Active People (DAP)), that’s $32.9 billion in additional revenue coming from GPUs. Using Meta’s operating margin ex-Reality Labs of 52% in the most recent quarter, that’s about $17 billion in incremental annual operating profit from GPUs. Meta’s total capex over the last eighteen months was $65 billion, so Meta’s ROI given the $17bb in incremental profit utilizing these new data centers was 26%.

And we actually think this ROI is conservative, because much of the servers installed over the last eighteen months are likely not fully contributing to Meta’s recommendation algos. There is a lag between when a data center is built and when those additional resources translate into additional revenue for the company. Meta uses these chips to train new recommendation algorithms which improve content delivery, ad targeting, and ultimately ROI for its advertisers. But all of that doesn’t happen overnight. However, even assuming that the capex spend of the last eighteen months was directly tied to the improvement in ARPP over that time frame, we still get a 26% ROI, which is quite good.

Amazon, Google, Microsoft, and Meta are all using a sizable portion of their capex to improve internal workloads. So if we use the total capex spend and compare that to the known pure “AI Revenues” (like the Street is doing), that dramatically understates the ROI. The earnings of the big tech firms themselves have grown tremendously over the last two years as they’ve used GPUs to improve their services. But the incremental earnings these companies have generated are not being attributed by the Street to their GPU purchases.

Reason #4: We’re In The Dial-Up Internet Stage Of The AI Revolution

So we have already shown that AI is already generating big returns for the biggest consumers of AI chips, and yet the underlying technology itself is still in its nascent stages. We like to say that we are in the “Dial-Up-Internet-Stage of The AI Revolution.” In five years or so, we’ll look back at the current chatbot age as extremely primitive. Companies are just now starting to integrate AI into their enterprise workflows. As agents continue to become more productive, we expect enterprise usage of AI to skyrocket. Further, the video age of AI is just beginning, with Sora (from OpenAI) and Veo (from Google) only able to generate 8 to 15 second videos. One day, we’ll use AI to generate incredibly captivating feature-length movies.

One thing we know for sure is that we’re not smart enough to predict the plethora of ways in which AI will be applied in the future. It seems like every week we are surprised with the new creative ways that people are using AI. This will only accelerate as the underlying models get better.

And that’s certainly going to happen. The big spending on AI infrastructure in the last 12 months or so will translate into step changes in model performance once that compute capacity is fully online. Elon predicted that we will see a roughly 10x increase in training compute in the beginning of 2026, and that will result in at least a doubling in LLM performance. The current LLMs are already incredibly useful and entertaining, and it will be incredible to see what future iterations will be capable of doing.

Reason #5: Everyone Is Looking For A Bubble And A Crash

Finally, the mere fact that everyone is sitting around looking for and calling for a bubble probably means there isn’t one. Almost everyone that is alive and investing today lived through the dot com bubble, and almost all of them have PTSD from that era. And there are certainly plenty of analogies to be made between the dot com boom and the current AI boom, i.e. the platform shift, massive infrastructure buildout, new business models, etc. So it’s not surprising that many investors point at these similarities as support for their bubble theses.

While there are similarities in the tech environment from the late 1990s and now, there are important distinctions to be made like those we’ve outlined above. But sitting here in 2025, with the internet bubble only 25 years in the rear view mirror, people are still a little scared of this tech-based rally. Not to mention, the Great Financial Crisis was only about 17 years ago (eight years after the dot com crash). So that’s two of the most significant economic collapses in American history in the span of a single decade.

So we can’t blame people for being cautious or skeptical in the current moment. But that institutionalized hesitation to invest in technology when stocks are hot is probably a good reason why tech stocks are going to continue to outperform. Simply put, there is a lot of cash on the sidelines, and that money will reluctantly be put to work in the major tech stocks as they continue to show improvement in the fundamentals. Remember how everyone was so quick to doubt the AI boom when DeepSeek hit earlier this year? And then every single major tech company raised their capex guidance after DeepSeek? People who panicked out of tech stocks back in February, March, and April are surely regretting those decisions today.

Conclusion

In the medium to long term, we think that US tech stocks will continue to outperform as they have for several years now. We are clearly in a tech-driven bull market, but as we’ve demonstrated there are good reasons to believe that this bull market has room to run. That’s not to say there won’t be volatility, or that there won’t be tests of the underlying trends along the way. However, we think looking at the underlying tech itself, and the fundamentals of the tech companies, it’s clear that The AI Revolution is going to create a lot of wealth for investors in the years to come.

Cody Willard

———————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 12/10/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 12/10/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.