Weekly Newsletter

Freedom Calls: 10/11/25, "Tony Blair talks diplomacy and crypto comes of age"

by

November 10, 2025

.png)

Freedom Calls: 10/11/25, "Tony Blair talks diplomacy and crypto comes of age"

From the team at Freedom Asset Management

Freedom does not come for free

Yesterday, in London was Remembrance Sunday – our annual reminder, just in case we might need it, that “Freedom does not come for free”. The freedoms we enjoy today cost many millions of lives across Europe’s borders and well beyond, across two World Wars and many other conflicts. A bumpy week in the markets looks very insignificant against those sacrifices. A reminder that tomorrow, on Tuesday 11th November at 1100, Europe grinds to a halt to reflect for 2 minutes' silence, the exact time in 1918 which marked the end of hostilities in WWI.

Pictured: the War Memorial to the Tank Regiment, Whitehall, Nov 2025

SALT London 2025 Conference highlights

I am grateful to the team at SALT for a last-minute invitation to their London conference. The SALT conference, which is basically the American alternatives scene spreading their gospel to the rest of the word, was big on crypto, fintech and private credit. I happened to be in London, so it all slotted into place. I like to dip into investment conferences on our travels just to make sure we are keeping abreast of the latest investment thinking - even if we are not big believers in all of them. This week, I am doing the same thing in Beijing, so brace yourself for that note next week.

Crypto comes of age…

Freedom started looking at crypto, and BitCoin ("BTC") in particular, in 2017. BTC was about $3,000 at the time. We could see the "digital gold" case, and we could see where people were going with the debasement of fiat currencies case, but we just could not get comfortable with the institutional custody arrangements at the time - or should I say the risk that a large gentleman, (with friends), would show up at your house and threaten to shoot your children unless you handed over the encryption keys to the fund's "highly secure" BTC account… So in the end, we did not set up the fund.

I would probably be writing this from my own lonely Caribbean island with high security fences if we had pulled that off. And that is slightly the problem with crypto: when you tell the story today with BTC at c.$100k, you look like a financial genius if you had invested all your money in BTC back then. But at the time it was a reckless and dangerous gamble with client money - and only for fund managers with no surviving family members, (or pets) they wanted to see again.

But time heals. And BTC is still here - albeit 99,000 other cryptos have scammed retail investors and died along the way.

So roll forward to the SALT stage last week and Anthony Scarmucci is interviewing crypto's great and good to ask them "what is the investment case today for BitCoin?". There were only 2 answers: "digital gold" and the "dollar debasement trade". And that is it…. 10+ years of financial innovation from some of the smartest people on the planet and it is still the same story. I remind crypto fanatics that,10 years on, there is still nothing (legal) that I cannot buy with my Barclays VISA debit card...

Pictured: a squirrel in London's autumnal Green Park going through his morning paces, no doubt like me also pondering the possible use cases of BitCoin.

But BTC’s survival and ubiquity means it is relevant and therefore has a value to those who believe – even if it is not the saviour of the financial system.

… the rise and rise of stable coins

One of the conversations that really surprised me, but shouldn’t have, is that stable coins are very much here to stay and are actively being used and supported by US government entities to facilitate payments where the traditional banking system has struggled due to excessive compliance and regulation. This partly explains Trump’s Genius Act, which legalizes stable coins and ensures that they are backed 100% by US Government paper.

Tony Blair talks diplomacy – “the problem with politics is politics”

Tony Blair (UK prime minister from 1997-2007) spoke at the SALT conference, surprisingly candidly, on a range of subjects from modern diplomacy to the ceasefire agreement in Gaza. He told a slightly incredible story about how the Gaza peace deal actually unfolded, but because of Chatham House rules, I will have to save that nugget for the next time we have lunch.

He made several important points about the Middle East today and Gaza’s future:

- The leading economies of the Middle East (the UAE and Saudi) are much more confident and significant on the global stage and want to see peace and a resolution of the Palestinian question;

The people of Gaza have had enough of Hamas; Hamas’ strategy of trying to achieve diplomatic isolationism against Israel has not worked, to catastrophic effect;

- The “people of” – and not necessarily “the government of” - Israel want peace with their neighbour – and have learned you cannot bomb your way to Gaza’s submission – no matter what you throw at it;

Israel sees great economic value in extending the Abraham Accords to Saudi Arabia.

Blair likened the current situation, in some elements, to the 1998 Good Friday agreement in Northern Ireland, where the IRA eventually worked out they were not going to bomb the British out of Northern Ireland, and the British needed a political solution to years of instability, senseless killing and violence.

Blair was key to delivering that peace agreement, which came with many difficult decisions regarding the treatment of past terrorist actions, but we can now look back on almost 30 years of peace in Northern Ireland, and an incredible period of economic growth for Ireland. By most people’s measures that is the definition of success.

He praised Trump’s negotiating style as “unconventional and direct”, something that the Biden team, with all its best intentions just could never pull off; Biden's team surrounded themselves in rounds of internal committees and protocols, whereas Trump just sends in Witkoff and Kuschner and next week there is meeting of the leaders to discuss, (and sometimes agree) peace. That approach will be re-writing textbooks on International Relations for many years to come.

He did not hold back on AI. Blair's view is “AI is like the Industrial Revolution – only more so”.

Performance – last week quite bumpy in AI stocks

There were two key stories in the markets last week – Powell saying not to expect another rate cut as being baked in, (see Justin's piece below), and famous short investor Michael Burry going “all-in” against Palantir and Nvidia with a $1bn short bet. Because of the interrelated nature of stock indices, this sent the defence and tech stocks down, and with them the S&P500. So in consequence, all the public market funds were off last week to varying degrees - see below:

(For detail, please refer to disclaimer section below)

As we have always said, in USVIP we don’t go chasing all the shiny stuff out there when it comes to AI and tech investing, so although last week was bumpy, it was far from making Michael Burry a rich(er) man. Note, ever since “The Big Short”, the film about Michael Burry’s huge bet against the US mortgage market in 2007/08, he has been unspectacularly unsuccessful at almost all his other big calls. My read here is that unless he covers these shorts very quickly, this will end up costing him a lot of money.

But every cloud has a silver lining, and in our case this means that our USVIP fund for a short time can now be bought at a c.8% discount to its recent peak, so for investors who have been on the sidelines, or waiting to top up – now is your chance…. I certainly will be. The thing to remember about this strategy is that it does not need a vibrant US economy for the investment strategy to be succesful – this technology is changing the world in front of our eyes at a rapid pace – just read Cody’s piece below on Tesla; a half-point move in rates does not change that trajectory, nor does even New York voting for a thinly veiled communist.

Our articles this week are:

- Justin Oliver (OGG) asks if it is “Time to hit the pause button on rate cuts?”

- Cody Willard (USVIP) writes, “Why we are cyber bulls on Tesla’s long term potential”

Please scroll down to read the articles.

This week I shall be in Hong Kong and Beijing, before a week of client meetings with our very own tech and AI expert Cody Willard in London and Guernsey - quite timely I think!

Wherever you are, let me wish you a wonderful and peaceful week ahead,

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

“Time to hit the pause button on rate cuts?”, 10/11/25

By Canaccord’s Justin Oliver – Adviser to the Opus Global Growth Fund

Jerome Powell’s term as Fed chair terminates on May 15, 2026. He has four more FOMC meetings to chair. At his latest post-FOMC press conference, Powell said that he and his colleagues continue to work in the best interests of the American public.

They haven’t always succeeded in doing so since Powell assumed the role of Fed chair on February 5, 2018. Many challenges have faced the Fed since the pandemic, including a two-month lockdown recession in early 2020, mounting federal deficits, an inflation shock in 2021 and 2022, the mini-banking crisis of March 2023, and political pressure to lower the federal funds rate during Trump 1.0 and 2.0. Nevertheless, we think Powell has done a very good job under the circumstances.

The Fed’s latest challenge is the federal government shutdown, which began in early October. Fed officials frequently state that their decisions are “data dependent.” Yet they decided to lower the federal funds rate (FFR) last week without much of the government compiled data on which they depend.

In his press conference, Powell said that the Fed is relying on data provided by the private sector: “It doesn’t replace the government data, but it gives us a picture. Again, I think if something material were happening ... I think we would pick that up. I don’t think we’ll be able to have a very granular understanding of the economy ... while this data is not available.”

He also said: “This is a temporary state of affairs. And we’re going to do our jobs, we’re going to collect every scrap of data we can find, evaluate it, and think carefully about it. And that’s our jobs, that’s what we’re going to do. If you ask me, ‘Could it affect the December meeting?’ I’m not saying it’s going to, but ... what do you do if you’re driving in the fog? You slow down. ... the data may come back. But there’s a possibility that it would make sense to be more cautious about moving. … I’m not committing to that. I’m just saying it’s certainly a possibility that [we] would say, ‘We really can’t see, so let’s slow down.’”

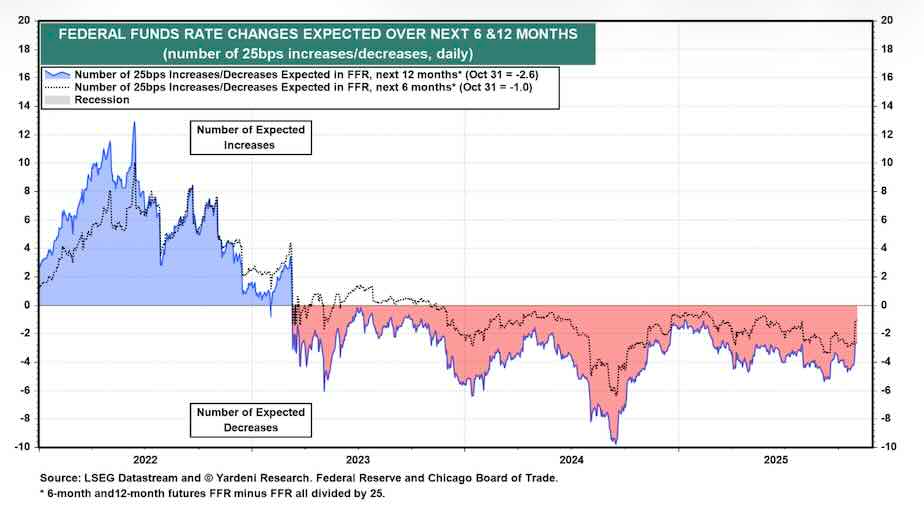

The basic message from Powell’s was that the Fed might be back in pause mode after cutting the FFR by 25bps at the September FOMC meeting and again at the end of October. The Fed’s latest easing cycle began at the September 2024 meeting, when the FFR was cut by 50bps and continued with 25bps cuts at the October and December 2024 meetings. Powell observed that the 150bps cut in the FFR has brought it down to 3.75%, i.e., within the 3.00%-4.00% range, which seems to be the consensus view of where “many estimates of the neutral rate live.”

He acknowledged that the FOMC median estimate of the neutral rate—i.e., the FFR that is neither restrictive nor stimulative—is 3.00%. That’s according to the committee’s September Summary of Economic Projections (SEP). But the latest SEP Dot Plot showed that the range of neutral FFR rate estimates is wide: from 2.50% to 3.75%. In addition, it showed that nine of the FOMC’s 19 participants estimated that the “long-run” FFR is higher than 3.00%, six estimated a lower neutral rate, and only four were at the median. Powell acknowledged the diversity of viewpoints in his prepared remarks: “In the Committee’s discussions at this meeting, there were strongly differing views about how to proceed in December. A further reduction in the policy rate at the December meeting is not a foregone conclusion—far from it. Policy is not on a preset course.” Notwithstanding their “strongly differing views,” only two of the voting members at last week’s FOMC meeting dissented from the 25bps cut decision. Trump loyalist Stephen Miran preferred to lower the target range for the FFR by 50bps, and Jeffrey Schmid wanted no change to the target range.

Trump loyalist or not, the next Fed chair will need to work with the other 11 voting members of the FOMC to make monetary policy decisions. In the past, Fed chairs have succeeded in persuading the majority of their voting colleagues on the committee to support their policy positions. Rarely have there been any dissenters; and when there were dissenters, they were few in number (one or two). A Trump loyalist as Fed chair might face more dissenters or even more than enough of them to vote for a policy stance contrary to the one the chair supports.

Such internal conflict within the Fed would seriously weaken its credibility and power. In addition, if Trump’s loyal Fed chair replacement manages to deliver rate cuts when incoming data don't justify them, the Bond Vigilantes might do what they did in late 2023, i.e., push bond yields higher. The Treasury might be forced to continue issuing more Treasury bills in the hopes that a reduced supply of Treasury bonds would bring their yields down. That's what happened in 2023. But the Bond Vigilantes might push back, recognizing that lower bond yields would cause the Treasury to rapidly increase the supply of bonds.

For now, the bottom line is: rather than continuing to ease at the next committee meeting, in December, the FOMC may press the pause button. That realisation after October’s meeting gave financial market participants pause: how many rate cuts to expect over the next six months was suddenly halved from two to one.

Justin Oliver

“Why we are cyber bulls on Tesla’s long term potential”, 10/11/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

It’s hard to compare what Elon and Tesla do to just about any other CEO or company (perhaps SpaceX is the only thing that comes close). Tesla just wrapped up its 2025 Annual Shareholder Meeting (ASM) and it was another powerful demonstration of how this company is set to truly change the world in the coming years. From robots and robotaxis to batteries and chips, everything at the ASM was centered around Elon’s plan for an autonomous future to achieve Tesla’s goal of “Sustainable Abundance.”

Pictured: Elon With The Promised “Cyber Bull” - Image Made With Grok

There were three things that stood out to us at this year’s ASM: (1) the coming inflection in scale; (2) Elon’s chip plans; and (3) Tesla’s full-stack approach.

First and foremost, it's obvious that Tesla believes they have solved autonomy for cars. Elon was explicit on this point:

“Now that we believe we have full self-driving, that we have autonomy solved -- or are at least within a few months of having unsupervised autonomy solved at a reliability level significantly better than humans -- that means it's time to ramp up production.”

Of course Elon has said similar things before, but we’ve seen first-hand how FSD has improved exponentially the last couple years -- since the switch to end-to-end neural networks -- and we feel confident that urban autonomy is basically solved at this point.

At the ASM, Elon spent most of his time explaining what Tesla is doing to ramp up manufacturing and wasn’t too focused on the remaining tech hurdles to achieve autonomy as he has been in the past. He explained that they are working to grow vehicle production by 50% next year, to about 2.6 million vehicles, and then growing that number to 4 million by the end of 2027 and 5 million the year after that. He made clear that these are aspirational goals, but it was also clear that in his mind scaling this fast will be limited by the slowest part in the supply chain, not demand. The reason being that the value proposition of the car is entirely different when it is fully autonomous. Within a few months, he expects you will be able to “text and drive” or “sleep and drive” in your Tesla, which he described as the “killer app” for autonomous vehicles. We agree with Elon, and think demand will be off the charts for fully autonomous vehicles.

Besides cars, Tesla is also laser focused on scaling semis and robots. The company is set to start producing commercial semis at its plant in Nevada, with the production rate starting at around 50k units per year. This will be a huge market in years to come, given the huge efficiency gains over diesel trucks (not to mention the value of autonomy for trucking), even if this doesn’t exactly move the needle for the company’s financials in 2026. But more importantly, the time has finally come for Tesla to begin scaling robots, starting with its Optimus Robot platform.

Tesla is “ramping up Optimus production faster than anything has ever been ramped up before in history.” -- Elon Musk

Tesla claims it has dramatically improved the design of Optimus with its V3 robot, and it is building a 1 million unit production line at its factory in Freemont, California, followed by a 10 million unit line in Austin, Texas. We think we will see thousands of Optimi working in Tesla factories next year, with commercial sales beginning in 2027. Moreover, we think Tesla will also start to expand into other robot form factors which will specialize at certain tasks (manufacturing, defense, education, entertainment, etc.). At the request of a shareholder, Elon even agreed to make a Cyber Bull robot which will roam around the Austin location!Second, we think Elon announced a major strategic priority for the company when he announced plans for Tesla to eventually start manufacturing its own chips at what Elon called a “Terafab,” a chip fab with a capacity of 1 million wafer starts per month (for context, TSMC’s current capacity is about 1.5 million WSPM). He said that he thinks chip production will quickly become the limiting factor to scaling robots and robotaxis, and therefore Tesla will need to further vertically integrate to meet demand. “I’m super hardcore on chips right now as you may be able to tell. I got chips on the brain. I dream about chips, literally.” -- Elon MuskOnce again, we think Elon is skating to where the puck is going with his move into chip production. If there is one thing we should have learned from The AI Revolution, it’s that the biggest chunk of value in the market (especially in the early days) accrues to those that control the chips (in AI, it was mostly NVDA and TSMC). We are now at the very early innings of physical AI, and Elon rightly recognizes that even Tesla’s formidable software stack and data trove are not what will matter long term if he can’t produce enough chips. It will be Tesla’s control of the design and manufacturing of the AI chips for the physical world that allow it to become a $30 trillion company as we’ve predicted. This is obviously a longer-term priority, but if there is one company on Earth that has the capability to replicate TSMC, it’s Tesla. To be clear, this is one if not the hardest manufacturing challenges on Earth, and we’ve seen how Intel essentially failed to do it despite immense capital expenditures and government backing. Nevertheless, this is a highly worthwhile endeavor given the immense payoff. As Tesla takes AI to the physical world, it must build the massive production capacity needed to meet the limitless demand we expect for its products. Third, we think Elon’s move to begin chip manufacturing is just further evidence of the value of Tesla’s full-stack approach to physical AI. In our view, Tesla is the only full-stack physical AI company, sort of how Google is the only full-stack digital AI company. Tesla, like Google, designs its own chips, builds its own AI models, owns its own unrivaled distribution channels, and builds its own applications. Google has demonstrated the power of the full-stack approach in the digital world, and now Tesla is doing the same thing in the physical world. What’s exciting for Tesla is that it is still so early in this game and it is basically the only megacap company in the world that has focused solely on AI for the physical world. While we are excited and encouraged by the many other companies that have recognized the value of robotics (including most of the big tech companies), Tesla is years ahead of these other companies and is the only one with the manufacturing capacity to scale these products to millions, if not billions of units. Tesla will start with robotaxis and humanoids, but the possibilities for the company are endless given its ownership of the chips, software, factories, and distribution channels. There will be no limit to the usage of AI in the physical world, from factories to spaceships to laundromats and aircraft carriers, and Tesla is the best positioned company to produce products to serve every application of physical AI. “This is not just a new chapter for Tesla, it’s a new book.” -- Elon MuskIn conclusion, we think Tesla provided a clear roadmap for the future of scaling autonomy to the physical world at the ASM. And importantly, Elon is now fully incentivized to achieve this future with the passage of his almost $1 trillion pay package by an affirmative vote of over 75% of shareholders. While the road ahead won’t be easy, the valuation is already high based on near-term metrics, and there are plenty of other risks, we continue to see massive upside potential for Tesla and we are excited to see the company execute on this roadmap in the years to come. Yes, the scaling plan is aggressive. Yes, building a TSMC-scale fab is insanely hard. And yes, Optimus deployment will start clunky before it compounds. But Elon has already proven he can take on industries that were considered untouchable—autos, space, industrial-scale batteries, etc.—and beat entrenched incumbents on manufacturing efficiency and speed. The playbook is the same: iterate fast, vertically integrate, and scale until you’re the cost curve. Cody Willard————————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated. Source: * Estimates Freedom Asset Management as at 8/11/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25. ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** Morningstar as at 8/11/25, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Rm 97 5/Fl United Centre, 95 Queensway, Admiralty, Hong Kong.

© 2025 Freedom Asset Management Limited.