Weekly Newsletter

Freedom Calls: 1/9/25, “Saying good bye to the summer… well almost”

by

Freedom Asset Team

September 1, 2025

7 Minutes

Freedom Calls: 1/9/25, “Saying good bye to the summer… well almost”

From the team at Freedom Asset Management

As luckily as the warm weather graced us for a bank holiday weekend, inevitability, the onset of cooler air and heavy showers in the days that followed signalled the end of summer. It has been a lovely summer, but this week it is properly “back to school” for everyone… with the small exception of (1) Labor Day today in the US, and (2) on Friday our Abu Dhabi office will be closed on the occasion of the Prophet’s birthday.

Pictured: Saying good bye to the summer, sunset at Cobo Bay, Guernsey, August 2025

September is a month charged with expectation. In my days working for larger corporates, when everyone came back from their summer holidays, we realised there were only 4 months left to execute on our respective budgets, sales, or performance targets…. needless to say, nobody was ahead of their targets, holidays were quickly forgotten, and September was always stressful!

At Freedom, we have tried to take a different view – of course the funds have performance targets, but our primary objective is to serve our clients - on their timeline, not ours. I have come to learn that this builds a better business and more enduring relationships. After all, in the private client business, we are in this for next 20 years, not 4 months.

This week’s articles:

- Fed independence is big topic in the markets and media – Ramon Eyck has written an excellent article for us this week, which reminds us that there is reason why Central Banks should be independent, but also notes some of the faux outrage from the media is a bit selective of history;

- Markets are questioning whether the benefits of AI are real, or overstated – Nvidia’s results last week were incredible, by any measure, with Nvidia guiding to “$3-4tr of AI infrastructure spending by 2030” – the market is struggling to price that story, but we think the AI story is sound (in the right stocks) – Cody Willard has written a piece for us this week talking about not chasing every meme stock… this is the difference between following random Reddit posts and having your “brokerage account money” (as I call it) managed professionally;

Please scroll down to read the articles.

Meanwhile in Ukraine

It is quite interesting that Trump signed off $300m of arms purchases for Ukraine over the weekend, which sends a clear message to Putin that the US, although wanting peace, is still prepared to underwrite the current conflict. I am beginning to think that the West’s plan now is to keep Russia distracted and bogged down in this conflict, so they don’t start another one with a NATO state somewhere else in Europe. Meanwhile peace seems a long way off.

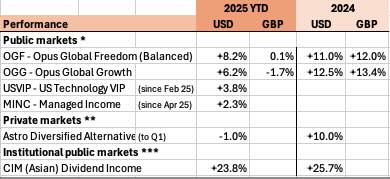

Performance – onwards and upwards

Markets brushed off all the noise around Trump and the Fed. OGG had another particularly good week. We saw the 2Q’25 price come in for Astro so that should price very soon and bring that fund very gently positive with a strong outlook for the second half.

Source: * Estimates Freedom Asset Management as at 30/8/25. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and also launch date of USVIP 10/2/25, ** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, *** FT Markets as at 30/8/25, I shares.

As a reminder we have Cody Willard and Bryce Smith in London and Guernsey next week. There are not many slots left, but please reach out if you would like to meet them.

I am in Guernsey and London this week. Wherever you are please let me wish you a wonderful and peaceful start to September.

With summer over, there are now only 121 days until Christmas - there is a thought to cheer us all up!

Adrian

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111* // M: +971 585 050 111 // M: +852 5205 5855* (*also WhatsApp)

--------------------------------

“How worried should we be about Fed Independence?”, 1/9/25

By Ramon Eyck – Investment Committee Member for Opus Global Freedom (“OGF”) and Managed Income Fund (“MINC”)

The independence of the Fed has been under pressure for much of 2025, with President Trump repeatedly labelling Fed chair Jay Powell a “numbskull” over his refusal to cut interest rates and the sacking of Fed governor Lisa Cook this week ratcheting these fears even higher.

Trump, like all politicians, would rather interest rates were lower, not least because this would substantially cut the cost of servicing the US government’s debt and reinvigorate the US housing market. Warnings coming from Fed insiders have been particularly stark, with former Fed Chair Janet Yellen stating in the FT this week that “this action threatens to end the independence of the Federal Reserve — and with it, the credibility of the US’s monetary policy both at home and abroad”.

What is the history of Fed independence?

During WW II, the US government needed to finance massive war spending and to keep borrowing costs low, the Fed agreed to peg interest rates on long term government debt at 2.5%, which meant the Fed essentially lost control of monetary policy. After the war, the US faced rising inflation (peaking at over 14% in 1947) and the Fed became increasingly alarmed that continued rate pegging would worsen inflation. Removal of the peg was resisted by the Treasury but after intense negotiations, Fed independence was established in what has become known as the “1951 Accord”.

So why is central bank independence considered so important?

Central bank independence is considered a key pillar of modern monetary policy, helping countries to control inflation, maintain credibility and confidence in their markets and support long term economic stability. Politicians often have short-term incentives (e.g. to stimulate the economy before elections), and independent central banks are seen as better able to focus on long-term price stability, even if their policies are unpopular. Turkey, Argentina and Zimbabwe provide stark examples of how the erosion of central bank independence can lead to surging inflation, a collapsing currency and capital outflows.

The pressure currently being exerted on the Fed has arguably increased the risk premia we should be applying to US assets. But to date, long bonds have only sold off modestly, the yield curve is only marginally steeper and the US dollar, while it has sold off significantly YTD, is down just 4% over the last 12 months.

Central Bank independence is clearly a sensible concept, so why has the market reaction been relatively subdued?

It’s quite possible markets are under-estimating the significance of this shift, but in reality there are a range of other factors that also need to be considered:

- Challenges to Fed independence are nothing new. Fed chairman have been repeatedly subjected to verbal assault, political manipulation and on at least one occasion physical threats, with Lyndon B Johnson reportedly having shoved Fed governor McChesney Martin against the wall of his Texas ranch.

- Independence doesn’t guarantee central banks are going to get the policy mix right, with many caught behind the curve over the years. This includes Powell, who raised rates 100bps in 2018 into a slowing economy then kept rates at zero for two years after Covid lock downs ended.

- Central banks have often been complicit in surrendering their independence. This has typically been in response to a crisis (such as the GFC or the LDI meltdown in the UK) but demonstrates that coordination between governments and central banks can be helpful.

- The US is not Turkey, Argentina or Zimbabwe! The US is the world’s most important economy and US Treasuries remain the lowest risk investment available. Fed Independence is enshrined in law and we would expect it to be protected by the Supreme Court (with Lisa Cook about to test this premise). And even if Trump does manage to stack the Fed board, the governors have reputations to uphold and are unlikely to bend entirely to his political will.

Fed independence is clearly important and while monetary policy has not been perfect under this regime, the existence of this independence has helped support US economic stability and underpinned confidence in the US economy and markets.

Trump is not the first politician to exert pressure on the Fed and he is unlikely to be the last but this does not mean confidence in US assets is about to collapse. Over time the risk premia associated with holding US assets may well rise but the Fed remains a strong, well-managed institution protected under the law so we believe markets are right to make a measured response to this latest confrontation.

Ramon Eyck

---------------------------------------

“The first rule of investment is don’t lose money…”, 1/9/25

By 10,000 Days’ Cody Willard, Adviser to the US Technology VIP Fund

"There are times to make money. There are times not to lose money. And if you don't know the difference, you're going to get killed." – Oft attributed to Stanley Druckenmiller

"The first rule of an investment is don't lose money. And the second rule of an investment is don’t forget the first rule." – Warren Buffett

One of our biggest differentiators in our Revolution Investing framework compared to other so-called innovation investors is that we actually do pay attention to valuations. We don't blindly look at P/E (price to earnings) or P/S ratios (price to sales) with no context, as we build 5-, 10- and 15-year financial models for each company we analyze. But we also certainly get context from historic P/E ratios vs today's market, which can help explain how we have been able to avoid major drawdowns in our strategies recently even as many formerly highflying theme stocks have been crashing 30%, 50% or more in recent weeks.

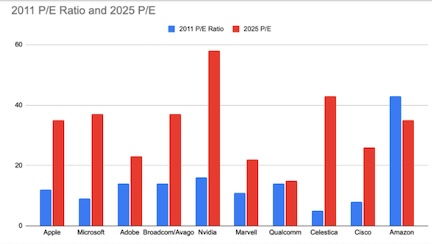

As I was cleaning out some old files in my office, I came across a book that I'd written in 2011 called “50 Stocks for the App Revolution”. In it, I repeated my prediction that billions of people would eventually be interacting with their smartphones (and tablets) trillions of times collectively every day and that investing in the best platforms and applications of The App Revolution would be the most lucrative investment approach.

Among the fundamental analysis I did for each of the 50 stocks in the book were the P/E ratios that they were trading at in 2011. When I saw the P/E ratios they were trading at back then, I almost fell out of my chair. Here are some examples of just how low tech stock P/E ratios were back in 2011 vs today :

You can see how much higher the P/E ratio for each tech stock is today compared to back in 2011 as every company except for Amazon has a higher ratio today. To give a little more context to these numbers, let's show consensus revenue growth for each of these tech stocks back in 2011 vs today too:

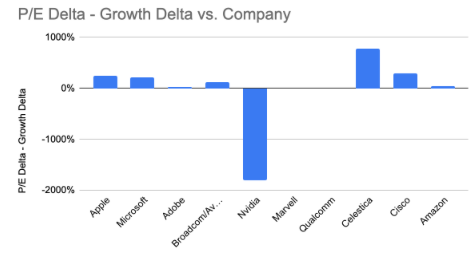

You can also see that most of the companies in this sample (6 out of 10, to be exact) are growing faster today than they were back in 2011, but for every company except for Nvidia, their revenue is not exactly exploding relative to the increase in their P/E ratios. We can subtract the growth in the P/E from the growth in the revenue to see this outsized discrepancy:

Again, every company but Nvidia has seen large gains in its P/E compared to the change in their revenue growth rates.

While these valuations certainly are high by historical standards, that doesn't mean we're necessarily running for the hills either. Many of the tech-naysayers and Luddites and short sellers have for years complained about high valuations, and for years these stocks have kept working.

One of the main reasons that these higher valuations are justified is that these large tech companies are larger, more profitable, and more monopolistic than any set of companies that have ever existed on planet Earth. Sure, Apple isn't growing as fast as it was in 2011, but the Apple Ecosystem is orders of magnitude larger and its platform now processes about $1.3 trillion in revenue through the App Store. Such durable, recurring, high-margin revenue is something the world has never seen. The company is almost untouchable (key word: almost), and thus it probably deserves a higher valuation than it did back in 2011 when it was still hard at work trying to grow that ecosystem.